As most of you know, I have formed an investment fund to acquire auction properties and flip them for profit. I have been very busy since mid-September when I turned my attention from raising money to actually doing the work. I have been intentionally mum on the blog about this endeavor; although, I will feature properties I acquire there from time to time in the future. Quite honestly, I don't want to attract too much attention to this opportunity for fear of competitors entering the market and driving down the margins. Due to that concern, this post will only appear on the IHB today, and tomorrow morning, it will be taken down. I want to inform my regular readers, who are most of my investors, without giving opportunity for potential competitors to review days later.

I would also like to start by saying the two properties I am featuring today are not typical. These were both outstanding deals for different reasons. The typical margins I am obtaining are about half as large. That being said, both of these properties are in escrow, so I have good reason to believe the margins presented are real. There is still a chance that either or both will fall out of escrow, but Alexander Hills is scheduled to close on November 18. When it does close, I will no longer be able to accept new investors into the fund.

Clean, beautiful 2-story home situated in the gated community of Lamplight Cottages. Desirable floor plan with 3 bedrooms, 2-1/2 baths. Open kitchen with a built-in island, granite countertops, built-in microwave, custom cabinetry, and tile floors. Living Room and stairs have dark chocolate hardwood floors and dramatic vaulted ceilings. Great Community with Pool, Clubhouse and lush green park. This home is owned by equity seller and available for quick close.

Bullish on Las Vegas's low end properties

Everyone is worried that Las Vegas prices will never bottom. In my opinion, properties in this price range are already there. The higher price ranges, like the second property I am going to show you, still has air to deflate, but the properties under $150,000 are not going to go much lower if at all.

I say that for one simple reason: prices are very affordable. Look at the income requirement on this house. With current interest rates this detached single-family house is affordable to someone making $25,725. That is a full-time single breadwinner making $12.86 per hour, or two breadwinners making that combined. That is affordability.

Further, the cost of ownership is much lower than comparable rents:

10483 CAROLINE ROSE ST

1,095

10439 MORNING SORROW ST

1,095

7570 GRASSY BANK ST

1,195

6191 BROKEN SLATE WY

1,100

8432 RAVENCREST ST

1,300

8225 GOLDEN FLOWERS ST

1,200

This property should rent for about $1,200 per month, making it a good cashflow rental property even at full retail cost (these properties have tremendous cashflow value at auction prices).

The combination of excellent affordability and the huge savings on the cost of ownership versus rental is prompting every renter with good credit to buy. The large positive cashflow is causing many cashflow investors to buy these properties both at auction and on the MLS. Between the local owner occupants and the outside cashflow investors, there is real demand at these price points.

I know I plan to buy several just like this one.

Selling to the tenant

The second property I have in escrow is a good deal that became a great deal because I sold it to the tenant.

Whenever I bid on an auction property, I always include a renovaton budget, and if the property is occupied, I budget cash-for-keys to pay the occupants to leave without trashing the house. In cases like this one where I was able to sell the property to the renter that lived there, I avoid both of those costs, and the savings falls to the bottom line.

This is a non-MLS sale, so there is no property description nor is there a link to

I think properties at this price point in Las Vegas still have some air in them. Of the properties I have purchased for the fund, the ones in this price range offer the greatest potential margins because so few auction buyers have the cash to trade these. Higher margins means it is easier for a flipper to lower price to move the property if necessary. That in turn means that prices for these will likely head lower. Further, the price-to-rent ratio is not good at these higher price points:

7871 SPINDRIFT COVE ST

1,850

7831 ABALONE BAY ST

1,850

Cashflow investors will not be attracted to these properties, so it is up to owner-occupants to clean up this mess. There is much more supply than there are buyers ready, willing, and able to absorb it. Prices in this range will fall.

But that is the risk of being a flipper. Catching falling knives offers great margins to those with the dexterity to juggle. Also, the margins provide more room for error or later price reductions.

Investor site up soon

I want to thank all the investors for their patience while I prepare the website to report on all the fund's properties. My attention has been on acquiring and processing these properties so far, but developing the investor website for reporting is now my priority. I have developed the report which will serve as a template, and I have the accounting system in place to track the details of the individual properties. You will be receiving an email from me soon with details on how to access the member's site. If you want to see the PDF reports on these properties, I have those available for your review. Email me and I will send them to you. The website will have all the same information when it is ready to go.

Milllions of loan owners struggle to stay afloat. Many persist like a shipwreck suvivor clings to a makeshift raft hoping and praying they will reach the beach.

The payments absorb billions of dollars that might be used for other forms of consumer spending, creating a drag on the overall economy.

By Don Lee, Los Angeles Times

November 1, 2010

For almost two years, home foreclosures have swept the nation, spreading misery among once-buoyant families, spattering lenders with red ink and undermining efforts to restart the economy.

But a bigger problem may turn out to be the millions of Americans who are still faithfully paying their mortgages, but on houses worth far less than before the bubble burst. It's not that these homeowners will stop making their payments. It's just the opposite — that they will keep doing it.

How could that be a source of future trouble? Because, with home prices stagnant in much of the country, payments on mortgages that are underwater could absorb billions of dollars that might be used for other forms of consumer spending — a drag on family finances, the housing market and the overall economy.

"Examine the graphic above. The first column shows a graphical breakdown of the income of a typical homeowner. Total home related debt (including taxes, insurance, HOA and other monthly expenses) is limited to 28% of gross income. Consumer debt including all other debt service payments is limited to 8%. Taxes take up about 24% (depending on income and tax bracket), and the remaining 40% is disposable income to cover the other expenses of daily life.

The second column shows what happens as people start to stretch to buy a home in a financial mania (charts are below). The increasing home debt reduces the tax burden a little, but the increased consumer spending and home debt takes a big chunk out of disposable income. The recession of the early 90s lingered for so long here in California because the people who bought in the frenzy of the late 1980s found themselves with crushing debts and greatly reduced disposable income. Prior to the increase in housing debt, this disposable income would have been spent in the local economy; instead, this money was sent out of state to the creditor who made the loan.

The big financial innovation–if you want to call it that–of the Great Housing Bubble was the nearly unrestricted use of cash-out refinancing and HELOCs to tap into home price appreciation. The third column shows the impact this new source of credit had on personal income statements. HELOC money allowed people to pay off their consumer debt while only modestly increasing their home debt. Since this income was untaxed (borrowed money is not truly income), the extracted money was entirely converted to disposable income. This incredible influx of disposable income caused our economy to explode.

Unfortunately, as is documented in the post Our HELOC Economy, the loss of this HELOC income is having devastating effects on local tax revenues and our economy. When you examine the personal income statements of borrowers in column four, you see that home debt and consumer debt have now become so burdensome that there is no longer enough disposable income to cover life's basic needs; borrowers are insolvent.

The only solution to the problem of borrower insolvency is a monumental restructuring of both home and consumer debt. Realistically, the only way this is going to occur is through foreclosure and bankruptcy. We are not going to re-inflate this Ponzi Scheme because when sustainable loan terms are applied to real incomes, people cannot raise bids to sustain or inflate home prices–even with 4.5% interest rates. Without home price appreciation and subsequent HELOC borrowing, the Ponzi Scheme does not work.

The implications of this are clear; we are going to experience an extended recession bordering on depression here in California that is going to linger for many, many years. During this extended crisis, a significant percentage of California homeowners are going to face foreclosure and personal bankruptcy.

The collapse of a Ponzi Scheme is never pleasant, and that is what we are facing. According to Arthur Miller, “An era can be said to end when its basic illusions are exhausted.” The unsustainable lifestyles and illusions of wealth created during The Great Housing Bubble are exhausted; the era has ended."

Back to the LA Times article:

And the drag could persist for years.

Of the estimated 15 million homeowners underwater, about 7.8 million owed at least 25% more than their properties were worth in the first quarter of this year, according to Moody's Analytics' calculations of Equifax credit records and government data.

More than 4 million borrowers, including 672,000 in California, 424,000 in Florida and 121,000 in Illinois — three of the biggest real estate markets — were underwater more than 50%. Their average negative equity: a whopping $107,000.

Many of these homeowners are paying much higher interest rates than the latest national average of 4.25%. They still have jobs and can afford to make the payments.

But they can't refinance because they owe too much. That home equity line of credit isn't going to happen. Even ordinary loans may be impossible to get. And selling the home at a huge loss is out of the question.

Nor can most underwater borrowers take advantage of the Treasury Department's loan-modification program, which generally requires a job loss or another kind of hardship.

In other words, they're stuck.

The individual loan owners are stuck, and the California economy is stuck because The California Economy Is Dependent Upon Ponzi Borrowers. With the various Ponzi loans being withdrawn from the market, California houses are no longer a viable source of spending money. We may maintain a significant amount of air in the housing bubble here because the Desire for Mortgage Equity Withdrawal Inflated the Housing Bubble, and this same desire will work to sustain it. Most loan owners in California view home price appreciation as an entitlement they can spend at will.

Heather Hines and her husband reflect this new reality. They owe $415,000 on a Santa Rosa, Calif., town house they bought in 2004 for $430,000. When the county appraised the three-bedroom home a few weeks ago, it was worth $246,000 — even less than a year earlier.

The couple had planned to move to a larger home after their two grade-school children became teenagers, but now that looks impossible. Their house needs a new roof, but they've put off replacing it for more than a year.

They did not budget for later home improvements because they expected the house to pay for itself. The appreciation was supposed to appear by market magic, and they would then borrow the money — at ever decreasing interest rates — to fix that roof. The best laid plans of mice and men often go astray.

"It's hard to think of making that investment when you're hundreds of thousands underwater," said Hines, 37, a city planner who like her husband is employed and has an advanced university degree. "It just feels hopeless. What are we supposed to do? It feels like we're never going to see any equity in our home."

They should feel that hopeless. Unless the Fed can print enough money to put everyone back to work and stimulate some major wage inflation, house prices are not going to regain their former peaks any time soon.

Theoretically, the Hineses could walk away — stop making the mortgage payments that consume a big part of their income. But defaulting would ruin their credit and have other negative consequences. So, she said, they'll keep paying and hoping for the best.

Hope is not a plan.

Unhappily for the rest of the country, that's not the end of the problem: The Hineses' financial bind will ripple throughout their community and the larger economy.

The real estate market depends on such homeowners being able to sell and move up; without them the trade-up market can't grow.

This is an under-appreciated feature of the housing market. When the government manipulations put in a temporary bottom at an elevated price point, they delayed the bottoming of the market. If the market had been allowed to crash and bottom in 2011, move-up buyers would have started becoming active by 2013, and the rate of sales would increase with the new influx of equity from appreciation. With all the government manipulation, we have elevated the bottoming price, but delayed the bottom for two or three years. The impact of that will be apparent over the next several years as the market drags along the bottom and few obtain any equity to simulate a move-up market.

Meantime, the Hineses will keep delaying that new roof, depriving a local roofer of business. They're unlikely to redecorate or upgrade the kitchen either, as millions of families were doing before the recession — more potential losses for local businesses, not to mention the car dealers, clothing and consumer electronics stores and manufacturers of the products that the Hineses won't buy.

Weighed down by the huge debt on their house, they also will be a lot more cautious about how they use credit cards. Big family getaways in the summer? Forget it, Hines said.

Multiply such sentiments by millions across the country and that translates into lackluster private spending, which accounts for 70% of the American economy.

"Families have not yet boosted their spending above the levels preceding the severe cuts they made during the recession," William Dudley, president of the Federal Reserve Bank of New York, said in a speech last month.

"This frugality stands in stark contrast to the first year of recovery from previous deep recessions," Dudley said.

This frugality will be long lasting. With the debt orgy we just witnessed, many are shunning debt in favor of a lifestyle of prudence and saving. Contrary to popular belief among economists, frugality and savings are good for the economy as people can invest in productive activities and assets instead of mindlessly consume.

In prior downturns, the housing industry and consumer spending powered the economy back to strength. Home building not only created construction and finance jobs but also fueled manufacturing of glass and lumber, furniture and appliances, and a host of other goods and services.

In normal times, the U.S. should be putting up about 1.7 million new houses annually, but this year it's running at about 600,000, economist David Crowe of the National Home Builders Assn. said. He thinks it will be three years before home building returns to its potential.

From what I am observing with the building industry here in California, we are coming out of the double dip, and activity is beginning to pick up again. Developers and builders are out working on land projects again preparing for the next cycle. Of course, this new activity is minor compared to the activity in 2005, but it feels like a boom compared to 2008 and 2009.

Rather than going out on their own or starting families, young Americans are doubling up with friends and relatives, saving more and paying down debts. Older Americans are staying in their jobs longer, hoping that the single biggest asset for most of them, their homes, will recover in value.

But nobody is expecting a return of rapid real estate appreciation any time soon.

Except here in California where everyone thinks the bottom is formed and the new party is about to begin.

If home prices were to rise at an annual rate of 3%, not an unlikely scenario, it would take the Hineses about 11 years to get to a point where their mortgage balance was even with their property value.

Refinancing the Hineses' 6.5% interest loan could be a big help, saving them almost $600 a month. But lenders won't even consider them.

And unless borrowers fall behind on their mortgage payments or face a high risk of defaulting, there's little chance that lenders, even with federal incentives, would reduce their principal or lower their interest rates.

"They feel completely left out," said Fred Arnold, past president of the California Assn. of Mortgage Professionals, referring to many underwater borrowers.

"If you stop payments, you have a much better chance of getting a modification," Arnold said.

Given these truths, is it surprising that some many mortgage loans are delinquent?

He contends that the federal government should set aside funds to help more borrowers refinance: "It would put immediate money into the economy." But that's not in the cards, especially with budget deficits weighing on Washington and the American public.

Eventually, economists suggested, a lack of options will push more underwater borrowers to walk away from their mortgages. But in the meantime, the stress on families, the housing market and the whole economy will continue.

Mike Saint-Just, 62, doesn't see a lot of room to maneuver. In 2007, he put down $125,000 on a $230,000 one-bedroom condominium near Palm Springs. County tax authorities say it is now worth $87,000.

After tapping a home equity line of credit, Saint-Just owes $143,000 — about two-thirds more than the value of his home.

Saint-Just draws a federal pension, enough to stay current on his loan but not much more. When he asked his lender about getting a new loan with lower rates, he said he was told he was too far underwater.

The loan officer "did say I could go into foreclosure and hope, maybe, they might do something. And they might not, in which case my credit would be ruined and I'd be out the door of the unit," he said.

So Saint-Just keeps making his monthly payments and cutting back on nearly everything else.

"It means dropping grocery stores and going to Wal-Mart, the 99 Cents store for food and generic items," he said.

With the winter coming, he's preparing to dress warmly and wrap himself in a large afghan to save on heating. That may get Saint-Just through the cold weather, but it may leave the overall economy to shiver.

don.lee@latimes.com

Those that continue to pay bloated mortgages damage the economy, and those that stop making payments stimulate the economy: Strategic Default: The $10,000,000,000 Monthly Economic Stimulus. So what do we make of that? Would a widespread loan owner revolt be a good thing for the economy?

They borrowed too much

Some people may have been able to afford their properties when they bought them, but then they simply over-borrowed and now they face losing their homes from excessive debt.

Today's featured property was purchased on 7/20/1998 for $237,500. The owners used a $190,000 first mortgage and a $47,500 down payment.

On 1/19/2001 they refinanced with a $305,000 first mortgage.

On 10/20/2004 they refinanced with a $388,500 first mortgage.

Total mortgage equity withdrawal is $198,500 including their down payment.

Foreclosure Record

Recording Date: 10/04/2010

Document Type: Notice of Rescission

Foreclosure Record

Recording Date: 09/29/2010

Document Type: Notice of Default

Foreclosure Record

Recording Date: 08/13/2010

Document Type: Notice of Default

Their recent notice of rescission suggests they just got a loan modification. The reality of their debts has prompted them to sell to get out from under the mortgage they can't afford. They already spent their profits on the deal, and now they are hoping they can escape without becoming another short sale. Their asking price gives them some room to maneuver, but not much.

Do you think they will get out without becoming a short sale?

According to the listing agent, this listing may be a pre-foreclosure or short sale.

HUGE $50,000 PRICE REDUCTION!!! One of the most desireable neighborhoods in Irvine. The Terrace has it all. Expansive lighted greenbelts, tot lots, two pools, a clubhouse, walkways and its close to everything; shopping (walking distance to a Ralphs market), freeways, entertainment centers like The Spectrum and The District and so much more. This three bedroom home is a wonderful spacious floor plan with a large kitchen, dining area and a cozy living room with a fireplace. Good sized, fenced and private rear patio. The single story home is situated on a small cul de sac and has an oversized driveway. Its in Move-In condition, in a great location and ready for you and your furniture. Great starter home or an investment property. No Mello Roos and low HOA dues. Wonderful community. This short sale should go fast.

desireable?

This short sale should go fast? When in the history of mankind has a short sale gone fast?

I bet they were surprised when they made their "HUGE $50,000 PRICE REDUCTION!!!" and no offers came in. The price has been reduced another $25,000 since then.

Date

Event

Price

Oct 22, 2010

Price Changed

$425,000

Oct 13, 2010

Price Changed

$450,000

Sep 21, 2010

Price Changed

$499,000

Aug 13, 2010

Listed

$549,900

Jul 20, 1998

Sold (Public Records)

$237,500

Jun 22, 1995

Sold (Public Records)

$180,000

Great starter home or an investment property. Starter home, maybe; investment property, not unless you are a fool.

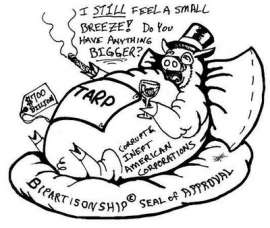

The story of the TARP program has been about winners and losers. Contrary to the much touted goal of preventing foreclosures, the TARP program is primarily designed to prop up our ailing banks. In this regard, it has succeeded. As for helping loan owners stay in their homes, not so much. Of course, the loan owners have benefited from amend-extend-pretend because they have been allowed to squat, but people don't want to squat, they want to own their homes with a reasonable payment. Unfortunately, they paid so much that owning with reasonable payments is not going to happen.

Office of the Special Inspector General for the Troubled Asset Relief Program

General Telephone: 202.622.1419 Hotline: 877.SIG.2009

SIGTARP@do.treas.gov

www.SIGTARP.gov

October 2010

More than two years have passed since the Emergency Economic Stabilization Act of 2008 (“EESA”) authorized the creation of the Troubled Asset Relief Program (“TARP”). On October 3, 2010, Treasury’s authority to initiate new TARP invest- ments expired, marking a significant milestone in TARP’s history but also leading to the widespread, but mistaken, belief that TARP is at or near its end. As of October 3, $178.4 billion in TARP funds were still outstanding, and although no new TARP obligations can be made, money already obligated to existing programs may still be expended. Indeed, with more than $80 billion still obligated and available for spending, it is likely that far more TARP funds will be expended after October 3, 2010, than in the year since last October when U.S. Treasury Secretary Timothy Geithner (“Treasury Secretary”) extended TARP’s authority by one year. In short, it is still far too early to write TARP’s obituary.

At the same time, TARP’s two-year anniversary is a fitting time for an interim assessment. To what extent has TARP met the goals set for it by the U.S. Department of the Treasury (“Treasury”) in announcing TARP programs and by Congress in providing Treasury authorization to expend TARP funds — avoiding financial collapse, “increas[ing] lending,” “maximiz[ing] overall returns to the taxpayers,” “provid[ing] public accountability,” “preserv[ing] homeownership,” and “promot[ing] jobs and economic growth” — and at what cost? In answering these questions, it is instructive to compare TARP’s impact on Wall Street with its impact on Main Street. By fulfilling the goal of avoiding a financial collapse, there is no question that the dramatic steps taken by Treasury and other Federal agencies through TARP and related programs were a success for Wall Street. Those actions have helped garner a swift and striking turnaround, accompanied by a return to profitability and seemingly ever-increasing executive bonuses. For large Wall Street banks, credit is cheap and plentiful and the stock market has made a tremendous rebound. Main Street, too, has reaped a significant benefit from the prevention of a complete collapse of the financial industry and domestic automobile manufacturers, the ripple effects such collapses would have caused, and increased stock market prices. Main Street has largely suffered alone, however, in those areas in which TARP has fallen short of its other goals.

As these quarterly reports to Congress have well chronicled and as Treasury itself recently conceded in its acknowledgment that “banks continue to report falling loan balances,” TARP has failed to “increase lending,” with small businesses in particular unable to secure badly needed credit.

As an aside, I note that I was contacted by my bank and asked if I wanted a credit line for my new business. When I said, no, I run a cash business trading in hard assets, the loan officer told me they are getting pressure to extend these credit lines, and if I change my mind, they want to loan money.

Indeed, even now, overall lending continues to contract, despite the hundreds of billions of TARP dollars provided to banks with the express purpose to increase lending. As to the goal of “promot[ing] jobs and economic growth,” while job losses may have been far worse without TARP support, unemployment continues to hold at roughly 9.6%, 3% higher than at the start of the program. While large bonuses are returning to Wall Street, the nation’s poverty rate increased from 13.2% in 2008 to 14.3% in 2009, and for far too many, the recession has ended in name only. Finally, the most specific of TARP’s Main Street goals, “preserving homeownership,” has so far fallen woefully short, with TARP’s portion of the Administration’s mortgage modification program yielding only approximately 207,000 (out of a total of 467,000) ongoing permanent modifications since TARP’s inception, a number that stands in stark contrast to the 5.5 million homes receiving foreclosure filings and more than 1.7 million homes that have been lost to foreclosure since January 2009.

I find the blunt truthfulness of this report refreshing. I am amazed this came from our own government.

On the cost side of the ledger, the results have been mixed as well. It is undoubtedly good news that recent loss estimates continue to suggest that the financial costs of TARP may be far lower than earlier anticipated, with the most recent estimates placing the dollar loss at between $51 billion and $66 billion. But costs can involve far more than just dollars and cents. Any fair assessment of TARP must account for other costs that, while more difficult to measure, may be even more significant. For example, as SIGTARP has noted in past quarterly reports, increased moral hazard and concentration in the financial industry continue to be a TARP legacy. The biggest banks are bigger than ever, fueled by Government support and taxpayer-assisted mergers and acquisitions. And the repeated statements that the Government would stand by these banks during the financial crisis has given a significant advantage to the larger “too big to fail” banks, as reflected in their enhanced credit ratings borne from a market perception that the Government will still not let these institutions fail, although the impact of this cost may be blunted by recently enacted regulatory reform.

Indeed our big banks are in a race to see who can get too big to fail. Once there, they no longer have to worry about maintaining good financial ratios, making good loans that will get repaid, or sacrificing short-term gains for long-term growth.

Another even more fundamental non-financial cost, as SIGTARP warned in October 2009, is the potential harm to the Government’s credibility that has attended this program. Despite the recent surge in reporting on TARP’s successes, many Americans to continue to view TARP with anger, cynicism, and mistrust. While some of that hostility may be misplaced, much of it is based on entirely legitimate concerns about the lack of transparency, program mismanagement, and flawed decision-making processes that continue to plague the program. When Treasury refuses for more than a year to require TARP recipients to account for the use of TARP funds, or claims that Capital Purchase Program participants were “healthy, viable” institutions knowing full well that some are not, or when it provides hundreds of billions of dollars in TARP assistance to institutions, and then relies on those same institutions to self-report any violations of their obligations to TARP, it damages the public’s trust to a degree that is difficult to repair. Similarly, when the Government promotes programs without meaningful goals or metrics for success, such as its mortgage modification programs, or when it makes critical and far-reaching decisions without taking an even modestly broad view of their impact, such as pushing for dramatically accelerated car dealership closings without considering the potential for devastating job losses, or when it fails to negotiate robustly on behalf of the taxpayer, as it did when agreeing to compensate American International Group, Inc.’s (“AIG”) counterparties 100 cents on the dollar for securities worth less than half that amount, the Government invites public anger, hostility, and mistrust. And by doing so, it dangerously undermines its ability to respond effectively to the next crisis.

Interesting that this report documents exactly how the government corporatocracy is screwing us.

While TARP is arguably moving to a new phase, recent actions this past quarter unfortunately suggest that the risks it poses to the public’s trust in Government will continue. Indeed, two areas of the greatest anticipated spending going forward — the Home Affordable Modification Program (“HAMP”) and the AIG recapitalization plan — highlight those risks.

This rather scathing report has generated some uncomfortable questions at the Congressional Oversight Panel.

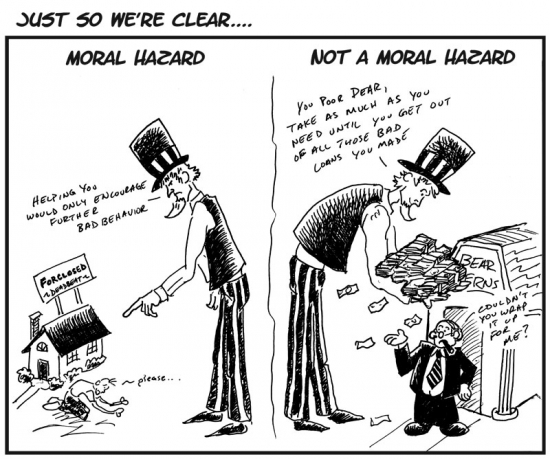

The government's much-criticized Home Affordable Modification Program helped set the stage for a successful private loan modification effort that likely wouldn't have gotten off the ground without it, said Faith Schwartz, former executive director of Hope Now.

If that is true, I wish this program had never started. Loan modifications do nothing but provide false hope to loan owners and extend this crisis.

Schwartz testified Wednesday before the Congressional Oversight Panel on the Troubled Asset Relief Program, in a hearing about TARP foreclosure mitigation programs.

"The HAMP roadmap set the stage for servicers to better apply solutions for distressed borrowers who failed to meet the HAMP requirements," Schwartz said in written testimony submitted to the panel.

"The Home Affordable Modification Program (HAMP) has received criticism, in part, because it did not immediately produce certain projected numbers of permanent loan modifications," she wrote.

The program has also been criticized by people like me who think it should not exist at all.

"This criticism is not entirely accurate," according to Schwartz. "HAMP has played an important role by helping to organize the participants and process in the loan modification effort and instituted a loan modification protocol that would have been difficult to mandate in any other way. Hope Now and government agencies attempted this in 2008 through the streamlined modification program, but it did not reflect all investors and primarily focused on GSE-owned loans. That was a start, but the HAMP program expanded and formalized those initial standards for loan modifications."

The Hope Now Alliance was formed in 2007 to expand and better coordinate the private sector and nonprofit counseling community to reach borrowers at risk.

"Early on, the goal of the Alliance was simple: reach at-risk borrowers that had no contact with their servicer," Schwartz said. "Research showed that over 50% of all foreclosures involved homeowners who were not in contact with their servicer."

Have you noticed rumors of principal forgiveness crop up whenever lenders want to get people to contact them? I think they use that as a bait-and-switch enticement to get people to contact their lender.

The alliance established a hotline, organized community outreach events, sent letters to delinquent borrowers and launched a website.

It also established HOPE LoanPort, aWeb-based system that enables for uniform intake of an application for a modification, allows stakeholders to see the same information in a secure manner, and delivers a completed loan package to the servicer that is actionable. The pilot program includes 14 large mortgage servicers, representing a majority share of the market.

Everyone knows how slow and inneficient government programs are. As soon as the government got involved, it should have been apparent to everyone that by the time they got their programs working, the majority of loan owners would already be foreclosed on.

"HAMP modifications offer a well-defined safety net for borrowers as a first line of defense," Schwartz said. "As evidenced by Hope Now data, servicers are implementing significant modifications after reviewing for HAMP eligibility by offering alternative modifications in lieu of foreclosure. Servicers report proprietary non-HAMP solutions run almost three times greater than HAMP modifications due to eligibility challenges."

"These are modifications that do not require taxpayer dollars and they are meant to benefit the homeowner and investor in lieu of foreclosure," she said.

HAMP should not exist. It has largely been a failure; and in that, I think it was a success.

Get as much as possible as quickly as possible

One of the lessons the Ponzis learned from the housing bubble is that they need to refinance as soon as a new comp gives them some equity, and they need to keep borrowing to the full extend of their borrowing power. Besides the immediacy of the spending money, it gives them downside protection. When the market inevitably crashes, they have already sold the property to the bank for peak pricing. Then they get to walk away, and while the air comes out of the bubble, they can repair their credit to get ready for the next cycle.

The owner of today's featured property paid $170,000 on 10/3/2000. He used a $163,150 first mortgage and a $6,850 down payment.

On 8/20/2002 he refinanced with a $189,000 first mortgage.

On 7/30/2003 he refinanced with a $189,200 first mortgage.

On 8/29/2003 he refinanced with a $201,000 first mortgage.

On 10/23/2003 he obtained a 21,500 stand-alone second.

On 3/25/2005 he refinanced with a $251,000 Option ARM with a 1% teaser rate.

On 1/10/2006 he refinanced with a $328,000 Option ARM with a 2% teaser rate. and obtained a $90,000 HELOC.

Total property debt is $418,000 plus negative amortization and almost two years of missed payments.

Total squatting time is about 20 months so far.

Foreclosure Record

Recording Date: 08/16/2010

Document Type: Notice of Default

Foreclosure Record

Recording Date: 11/19/2009

Document Type: Notice of Rescission

Foreclosure Record

Recording Date: 06/18/2009

Document Type: Notice of Default

Do you ever wonder when I will run out of these? Irvine is supposed to be an upscale neighborhood where everyone makes hundreds of thousands of dollars a year. Why do we have so much HELOC abuse? Why are so many losing their homes due to their excessive borrowing? Could it be that Irvine is a facade? How much of Irvine is populated by posers trying to impress other posers?

According to the listing agent, this listing may be a pre-foreclosure or short sale.

Price Reduction!!! CLEAN UPSTAIRS 2 BEDROOM, 2 BATH CONDO. BEAUTIFUL VIEW OF PARK/GREEN BELT. GREAT FOR FIRST TIME BUYERS/INVESTORS AND WONDERFUL FAMILY COMMUNITY. WOODEN BLINDS THROUGHOUT. NEWER CARPET AND PAINT. SEPARATE DINING ROOM.

Good for investors? Sure, I want to pay $289,000 to obtain $1,700 a month in rent, and give $490 a month to the HOA. Only a kool aid intoxicated fool would consider this a good investment.

I've been feeling energized lately. Everything is going very well personally and professionaly, and i am very excited about the new venture. After two or three years of the red-ink recession, I am back in the black. It's not just financial, its feeling useful, needed, and productive again. Long periods of professional inactivity dulls the mind and the senses. That's a hidden toll the recession exacts on people, even those who don't experience the full brunt of unemployment.

I have been reluctant to write much about the new venture. There are some business secrets I have an obligation to keep. I have been obtaining very good margins, but I don't want to broadcast it too loudly and bring in competitors. The blog has a loud voice at times.

I will start writing some posts about these Las Vegas properties, but I need to think through what I should and should not reveal as my greater duty is to the interests of my investors. If i spent a week documenting the details of each of the seven properties I have purchased, I would likely see a number of new competitors show up at the auction site. There is a balance, and I will find it.

Las Vegas

Las Vegas is an interesting town to travel to for business. Since I am there when the tourists are not, the rooms are much cheaper, and all the activities are less expensive and less crowded.

I have my own barometer of the financial health of Las Vegas. I am still driving to Las Vegas each week. As I go through Victorville and reach the edge of civilization before heading across the high desert, there is a Motel 6. Lately, the rate has been $44.95 per night on Sunday when I drive past. I have been staying at the Sahara for $30 per night. There are often rooms available for less than $20 per night in Las Vegas. When the Motel 6 on the fringe charges more than a big casino hotel on Las Vegas Boulevard, times are tough in Las Vegas. Maybe I am wrong, and perhaps fringe motel rooms always carry a premiium, but the Las Vegas casino hotel is a billion times more fun and interesting.

When I go out in Las Vegas (I like to throw dice), it still feels alive and vibrant. Fremont street is often packed with people, and the strip casinos have a lot of activity. The problem with Las Vegas isn't a decline in the traffic of people (there has been some of that too). The problem is that visitors are not losing or spending as much money as they used to. And while about 50% of the construction industry remains unemployed, those idle workers are not earning money and contributing to the economy. The lack of a viable housing market and its associated labor market is what makes this recession go on and on.

I have always liked Las Vegas for a variety of reasons. And going there every week is a responsibility I enjoy.

If you manage to time the real estate cycle in California, the return on investment can be enormous. All the speculators who used 100% financing and either HELOCed or sold at the peak obtained an infinite return because their investment was zero. But even the FHA buyers who put 3% down obtained returns on their investment that in many cases is measured in triple digits. The owner of today's featured property invested $4,500 when he purchased, and when he refinanced at the peak, he sold it to the bank (in a nefarious way) and made $169,500. That is approximately 38 times what he invested. The bank is left holding a $262,500 mortgage on a tiny old condo worth about $200,000 in today's still-inflated market.

According to the listing agent, this listing may be a pre-foreclosure or short sale.

Looking for Investor or solid owner occupant transaction to stay the course with the short sale process.

Good luck with that.

I find that the cumbersome nature of the short sale process makes is easier for flippers to sell houses. Buyers don't have the patience to wait forever for a short sale. There are many buyers who have offers on several short sales, and they sit and wait for one of them to pop. When a filpper puts a property on the market, it gets attention because a prospective buyer does not have to wait for a bank to make up its mind. Both short sales and REO are bank decisions. Third party trustee flips pair serious sellers and impatient buyers. If the property is priced right, it quickens the pace of sales significantly.

Right now, I don't want to see mortgage interest rates go higher. I plan to borrow heavily to buy as many cashflow-positive properties as I can get, and as long as interest rates are low, I hope to take advantage of them. However, the best thing for the housing market is not sustained low mortgage rates because those rates only benefit the few who qualify. We need lower prices, higher interest rates, and more people to qualify for mortgages.

often hear people wonder aloud why banks won't loosen underwriting standards on home mortgages. I'm beginning to wonder the same thing. That's because I think it is time for lenders to start issuing mortgages to non-prime borrowers again, though not on the same shaky terms that triggered the housing crisis of 2008, of course.

I wondered why we don't relax lending standards for investors in Should Government Mortgage Subsidies Be Offered to Cashflow Investors? There are many good borrowers being denied credit right now because lenders are so afraid of certain loan products that even the small number of borrowers who can properly utilize certain loan products are being denied. However, the main reason banks won't loosen underwriting standards is because they really don't know which ones they can loosen and still get their loans repaid.

First, the reason why lenders are hesitant to relax loan requirements: The heart of the matter is: Mortgage rates and their profitability margins are so low, it just isn't worth the risk to lend to anyone who is anything but a AAA+ credit-worthy consumer.

Furthermore, it takes an implicit guarantee from Fannie Mae or Freddie Mac, on top of that sterling rating, to make mortgage lending even semi-palatable for a bank or investor.

The real problem with mortgage lending is super low interest rates made possible by government loan guarantees. It started when the Federal Reserve began buying down interest rates through purchase of GSE insured loans. When the program terminated in early 2009, there was great concern that interest rates would rise. After the Fed quit purchasing GSE MBS, purchase applications and home sales plummeted. As purchase applications fell, so did interest rates as the supply of money available for home mortgages exceeded demand.

Mortgage interest rates are at historic lows for those with good credit who are borrowing less than the conforming limit; however, for those outside of these parameters, either the interest rate is significantly higher, or credit is simply not available. The market would ordinarily react by pushing interest rates higher. If the yield does not match the risk — and the risk is much higher for non-insured loans — the yield must go up to attract capital. Higher yields mean higher interest rates.

For better or worse, the housing market is fueled by Wall Street's appetite for mortgage-backed securities. As mortgage rates continue to set historical lows, so do their profitability margins — as well as the profitability margins of the securities they reside in (that investors typically buy, sell and otherwise trade on).

Being that investors have no appetite for high-risk, low-yield investments, there's simply no money in mortgages right now. As a result there is very limited credit available in the marketplace, especially to non-prime borrowers.

This is not a problem limited to subprime borrowers. Anyone looking for a jumbo loan can expect to pay a much higher interest rate and be subject to very high qualification standards. Even then, these loans don't make much sense given the likelihood of declines at the high end.

This is in stark contrast to what was a high-risk, high-yield, credit free-for-all environment that was in place from 2002 until the housing market crash in late 2008.

So, it's been two years since the crash and the prevailing thought has become that: Interest rates must be kept low to keep consumers "incentivized" and "transacting." Unsustainable consumer incentives have run their course. A tax credit has been tried and proved expensively ineffective while interest rates have been kept artificially low for too long. These are strategies that treat the illness but do little toward finding a cure.

Current mortgage rates for the most qualified consumers and properties are hovering around 3.99 percent for a 30-year-fixed and as low as 2.875 percent for the 5-year-fixed variety. Yet while mortgage rates are jaw-droppingly low, the housing market is no closer to snapping out of the protracted downward spiral it's been in for a couple years now. You can drop rates to .399 percent, but if only a tiny consumer pool qualifies for such, there isn't enough benefit to impact the market in a meaningful way.

Money needs to be thoughtfully brought back to non-agency mortgage-backed securities, which would require higher interest rates and the yields they offer investors. Huh? Yes, increasing interest rates and the yields that accompany them are required if we want to see credit flow back into the non-agency — that includes portfolio, jumbo, Alt-A and subprime loans — mortgage-bond markets. We need more liquidity and credit in the non-prime, non-agency mortgage pools if we want to pull out of the housing quagmire, because there's a huge pool of non-prime borrowers who can afford mortgages.

If prices were allowed to fall, and if mortgage interest rates were allowed to find a natural equilibrium, credit would be made available to more people. The problem right now is not interest rates, it is the number of qualified borrowers who can take advantage of them. The market manipulation has made mortgage debt inexpensive and affordable, but only for a small number of people.

It isn't a matter of simply lowering qualification standards and allowing more people to borrow at low interest rates. We must find a natural market where risk is tied to yield, then we will have credit being made available to a larger number of people albeit at much higher rates.

Something that gets lost when discussing borrower defaults and foreclosures is that people who were prime borrowers are defaulting just as readily as non-prime borrowers. At the same time, there is an abundance of non-prime borrowers making their mortgage payments in a timely fashion.

I've had the opportunity to personally review residential mortgage-backed securities and can attest that FICO scores and loan-to-value ratios are not the leading factors behind mortgage defaults. That's why I think it's time to bring back the non-prime borrower into the mortgage market.

So, how high do rates need to be? Likely 300 to 400 basis points (3 percent to 4 percent) higher than they are today.

Therein lies the reason why this doesn't happen. If interest rates were 300 to 400 basis points higher, affordability would decline about 50%, and prices would crumble. A natural rate of interest after a catastrophe like the housing bubble would be much higher than it is today. The housing bubble was caused by a mispricing of risk, and we are still doing it. Before it was questionable credit default swaps that allowed the market to misprice risk, now it is the backing of the US government that is doing the same. AIG went under because of the credit default swaps they issued. The US taxpayer will likely absorb huge losses because we are currently underwriting the entire housing market.

Interest rates of 6 percent to 7 percent on a fixed-rate mortgage are still cheap money, and there is a very large pool of consumers who could afford mortgages with rates in this range but who qualify for nothing under today's agency-backed underwriting guidelines. Get back to mitigating risk with price, but in a more responsible way.

Non-prime borrowers will call for different underwriting standards. I'm not talking about going back to the days of no income, no asset, no job requirements; I suggest going back to more logical and flexible underwriting criteria. A heavy emphasis must still be kept on the substantive components of mortgage qualification: Credit, income and assets.

These suggestions will ultimately come to pass, but it will be years before we have anything resembling a natural market for interest rates or home prices. For now, propping up prices with artificial interest rates created by government backing is the official policy, and as long as our banks teeter on the edge of insolvency, this policy will continue.

Despite the robo-signing paperwork mess, there will continue to be abundance of foreclosed inventory flowing into the market — that desperately needs buyers who desperately need credit — or the property will continue to rot a hole into the housing market and U.S. economy for many years to come.

We learned a lot from the housing boom and subsequent bust. No one is suggesting that we go back to the period of 2003 to 2007. Increased awareness and transparency on many levels likely will prevent that.

Actually, many have suggested that we return to the bubble ways. Many of our efforts to prop up the market are similar to what we did in the bubble. For example, loan modification programs are essentially Option ARMs. No amount of awareness and transparency is going to prevent a housing bubble.

I recommend that lenders increase rates and yields to match the risk of the underlying borrower and security. A bold move like that will get investor liquidity and credit flowing back into a market that is choking itself out.

I agree that we need to match yield to risk to better serve the housing market, but it isn't going to happen any time soon because in order to do what he suggests, house prices would need to fall another 30% while interest rates doubled. The bank losses and chaos that would create make it unpalatable to policy makers and, of course, the banks — if you can actually tell the difference between the two.

What passes for responsible mortgage management in Irvine

Most loan owners I profile in Irvine have more than doubled their mortgage. Almost all borrowers I see looking through the property records have added to their mortgage. It is a very rare case to find a homeowner who paid it down. What should be the norm — paying down a mortgage on a 30-year amortization schedule — is a rarity.

I hate to give borrowers in this category a "passing" grade, but this is the reality for most Americans. Growing credit card or mortgage debt slowly generally can be compensated for through home price appreciation, and although I consider this a bad idea, I can't really call it HELOC abuse, just foolish HELOC use. Is there a distinction there? I will let you decide.

Financial planners will tell you that most people fail to budget properly for unexpected expenses (they don't save), so when they fall behind a little each month, they put the balance on a credit card and hope they can pay it back with a tax return — or during the bubble with a visit to the housing ATM.

People are still going to manage their bills this way going forward, and there will be pressures to "liberate" this equity to pay for these expenses. The money changers will continue to peddle this nonsense as sophisticated financial management. It is a stupid way to manage debt, and I give it a C.

The owners of today's featured property paid $192,000 on 6/17/1988. I don't have their original mortgage data, but they likely put 20% down.

On 4/6/1998 they refinanced with a $191,000 first mortgage. Ten years after buying this property, the mortgage nearly equaled their purchase price.

On 7/17/2000 they obtained a $37,000 HELOC.

On 12/10/2003 they got a $50,000 HELOC.

On 10/21/2004 they refinanced with a $215,000 first mortgage.

On 5/31/2007 they opened a $150,000 HELOC.

On 8/31/2009 they refinanced again with a $264,500 first mortgage.

After owning the house for 22 years, they should have it nearly paid off, but instead, they extracted $100,000 in equity and they have enlarged their mortgage considerably. They will still sell this home and make a significant profit — thanks to the housing bubble.

So what do you think? Is this a reasonable way for people to manage their mortgage debt? Are these people acting wisely and responsibly?

This is a custom home with light large open spaces. Custom wood work and hardwood flooring give the home a warm, friendly feeling. The windows are large and include operable skylights. This creates excellent cross ventilation. The home is located within walking distance to all schools. Irvine High School, Heritage Park, and Irvine public library are very close by. The home has three bedrooms downstairs and two upstairs, along with a large bonus room. The bonus room has a built-in Murphy bed. The three full bathrooms have been remodelled, and the master bathroom features a Jacuzzi tub. The upstairs bathroom is a Jack and Jill, opening to both bedrooms. There are two fireplaces. One is used brick in the living room. The other is in the master bedroom. Mature trees and landscaping make the exterior of the home lovely and relaxing. The home includes a gazebo in the backyard, which is included in the sale.

remodelled?

I hope you have enjoyed this week, and thank you for reading the Irvine Housing Blog: astutely observing the Irvine home market and combating California Kool-Aid since 2006.

.jpg)

.jpg)

.jpg)

.jpg)

{kind=link}