Houses are taking a long time to sell in Irvine today. It's rare to see this kind of weakness in Irvine. Usually, the constricted supply keeps prices elevated and makes the pace of sales relatively brisk. That is not today's market.

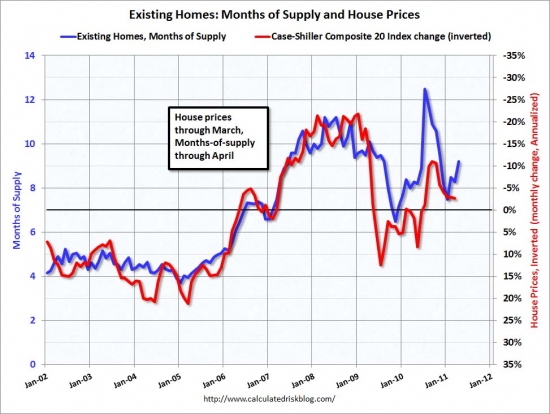

Months of supply is a good indicator of macro trends impacting the US housing market. The chart below from Calculated Risk shows the strong correlation between months of supply and the change in price.

Months of supply is my least favorite indicator of market action on a local level. It's too volatile, and it says little about the forces underlying the market. The smaller the area, the more volatile it becomes because there are so few data points. Of course, that doesn't mean realtors don't try to use it. Since it is volatile, it's relatively easy to make note of recent changes and blow them out of proportion to create false urgency.

One analysis of real estate for sale in Irvine shows the market speedier in its last tabulation.

Every two weeks, Orange County broker Steve Thomas publishes a report on the supply of local homes for sale. Here's what the latest report — as of Sept. 29 — has to say about Irvine …

769 residences listed in brokers' MLS system with 196 new deals opening in the past 30 days.

By Thomas's math, this community has a “market time” (months in would take to sell all inventory at current pace of new escrows) of 3.92 months vs. 4.00 months found two weeks earlier vs. 4.77 months seen a year earlier. Countywide, latest market time was 3.61 months vs. 4.28 months a year ago.

So, homes in this community sell — in theory — in 9% more time than the countywide pace.

Of the homes listed for sale in this community, 203 were either foreclosures being resold or short sales, where sellers owe more than the home's value. So distressed properties were 26.4% of supply of homes for sale vs. 34.7% countywide.

Homes for sale in Irvine represent 7.4% of Orange County inventory — and 5.7% of all the distressed homes listed for sale in Orange County. New escrows here are 6.8% of all Orange County's new pending sales.

Compare these trends to countywide patterns:

Cities with highest level of distressed properties among their listings? Lake Forest was tops — 59.0% — followed by Santa Ana at 58.5% of listings and Anaheim at 58.3% of listings.

Fewest? Seal Beach was tops — 4.1% — followed by Corona Del Mar at 5.0% of listings and Newport Coast at 6.7% of listings.

I have a problem with Steve Thomas's math. Rather than use the accepted method of calculation — inventory divided by closed sales — Thomas uses opened escrows, a number always larger than closed sales because many properties fall out of escrow. By making the denominator of this fraction larger, he consistently understates the actual months of supply. Closed sales is an easy number to obtain from the MLS data, so there is no reason to use opened escrows over closed sales other than the desire to make the months of supply look smaller. A smaller month of supply number makes the market look better than it really is, and appears to be intended to create false urgency in buyers.

Below are the actual calculations of months of supply done properly for Irvine over the last two months by zip code. The volatility of the numbers is apparent. The increase in months of supply from 4.3 to 5.0 is nearly a 20% increase from August to September.

Zip codes that were disasters in August were healthy in September and visa versa. The usefulness of this information is suspect. How should someone use this data? Should buyers accelerate their plans or put them off? What about sellers? I doubt many people base their decisions on this data, nor should they.

From the post yesterday, 92603 (Turtle Rock, Turtle Ridge and Quail Hill) are the villages showing the most recent weakness, and the months of supply does reinforce that idea. Aggregate numbers are somewhat more accurate because they are less susceptible to small changes in inventory or sales. The aggregate numbers for Irvine also show the increased months of supply caused by hefty inventories and slow sales. However, months of supply is generally going to increase in September and October because sales drop off faster than inventory is removed from the market. It's November when sellers typically give up and hibernate for the winter. The sellers active from mid-November through February are the most motivated.

Horrible realtor ad of the day

Home ownership is under attack… or is it that loan owners are not being responsible with their payments? From the video below, you would assume responsible people are being forced out of their homes. The reality is irresponsible people are being forced out of the bank's home.

25%-30% off the high end

The owners of today's featured property paid $1,200,000 in the summer of 2005 using a $959,900 first mortgage and a $100,000 HELOC. The house appreciated for a year, and they increased their mortgage to a $1,000,000 first mortgage and a $96,500 HELOC. It appears they have been dutifully paying the mortgage ever since.

However, most people who attempt a short sale aren't paying their mortgage, so they could be delinquent and in shadow inventory (delinquent on the mortgage and no notices filed). In any case, their asking price is 25% less than they paid, and if it sells, they will lose their down payment, and the lender will be out a nice chunk as well. This is the kind of short sale that will take forever to get approved as the lenders will not want to absorb the loss and the borrower will not want to pay the difference.

Spectacular luxury gem neslted in highly sought-after gated neighborhood on quiet cul de sac. Loaded with opulent finishes and offering ample natural light – this gem will be the pride of any homeowner. Great features include: beautiful hardwood and/or travertine flooring. Great yard ideal for entertaining. WOW!

——————————————————————————————————————————————-

Proprietary IHB commentary and analysis

Resale Home Price …… $899,999

House Purchase Price … $1,200,000

House Purchase Date …. 6/22/2005

Net Gain (Loss) ………. ($354,001)

Percent Change ………. -29.5%

Annual Appreciation … -4.4%

Cost of Home Ownership

————————————————-

$899,999 ………. Asking Price

$180,000 ………. 20% Down Conventional

4.20% …………… Mortgage Interest Rate

$719,999 ………. 30-Year Mortgage

$179,552 ………. Income Requirement

$3,521 ………. Monthly Mortgage Payment

$780 ………. Property Tax (@1.04%)

$0 ………. Special Taxes and Levies (Mello Roos)

$187 ………. Homeowners Insurance (@ 0.25%)

$0 ………. Private Mortgage Insurance

$150 ………. Homeowners Association Fees

============================================

$4,638 ………. Monthly Cash Outlays

-$825 ………. Tax Savings (% of Interest and Property Tax)

-$1001 ………. Equity Hidden in Payment (Amortization)

$270 ………. Lost Income to Down Payment (net of taxes)

In August, prices dipped below rental parity for the first time in over a decade. In September, prices fell further below rental parity than any time in the 00s.

There have been few rays of sunshine for the local housing market over the last five years. Prices are down about 30% from the peak, and hopes of a bottom were crushed when a double dip ended the false rally of 2009 and 2010. The bad news can't go on forever. Prices won't fall to zero. Eventually, prices get low enough that people get a reason to buy other than dreams of capturing appreciation. Once prices fall below rental parity, people can buy to save money versus renting.

Payment affordability

When we talk about affordability, everything is relative. Incomes are a good measure, and using a 31% DTI applied to local incomes provides a useful measure of affordability. Another measure is local rents. Since rents and incomes are closely tethered (people don't typically borrow their rent), local rents are a good proxy for local incomes.

Since most house purchases are financed, the affordability of monthly payments is important. Since rents are paid on a monthly basis as well, the comparison of the monthly cost of ownership to rent is a very useful measure of affordability. Basically, if people can afford their rent, they could afford a payment equivalent to rent. Thus rental parity is a good measure of payment affordability.

Financing terms are important

When examining the cost of ownership, the financing terms become very important. The folly of the housing bubble was to abandon amortizing mortgages in favor of interest-only and negative amortization loan products. People used these Ponzi loan programs to lower their monthly payments and ostensibly lower their cost of ownership. While they did lower their payments for a time, the terms of these loans were not stable. At some point, they needed to recast to fully amortizing loans which would be paid off. The “payment shock” of this recast was a timebomb waiting to blow up a family's balance sheet. Most of these loans have already blown up, and the borrowers are waiting in shadow inventory for lenders to clear them out.

People sought ways to defuse the recast bomb by a process known as “serial refinancing.” Right before the bomb was due to go off, people assumed they would be able to refinance into a new loan and reset the clock. Most borrowers believed these financing terms would always be available, so they had little risk of being around for the explosion. As we all know now, these borrowers were all wrong.

When considering the cost of ownership for calculations of payment affordability, the cost of an amortizing mortgage must be considered. Interest-only and negative amortization loans artificially lower the cost of ownership, but these methods are not sustainable.

ARMs are dangerous too

Amortizing adjustable-rate mortgages are also a dangerous product. People select them because they carry a lower interest rate, and the payments are marginally more affordable. These loans work great when interest rates are falling, but when interest rates rise, loan payments go up, and the savings from early payments is more than made up for by increasing costs later on.

The real danger with an ARM loan is embedded into obscure terms of the promissory note. The loan is written with a contract interest rate that changes periodically. There is a contractual limit as to how high the interest rate can go. Unfortunately, affordability is only measured against the contract interest rate. If interest rates rise, the payments could very easily become unaffordable, and the borrowers could face the same problems with default and foreclosure many are dealing with today.

The worst part about ARMs is that the additional risk is not necessary. Fixed-rate mortgages also allow for refinancing when interest rates drop. Borrowers simply refinance into a new loan. There is no need to use ARMs to capture the benefit of falling interest rates.

Of course, despite the problems with ARMs, many people will still use them and assume the government will bail them out if the going gets tough. It's hard to argue with a borrower who believes that. So far, the government has shown every sign of bailing out even the most foolish of borrower behavior.

Interest rates and principal balance

Interest rate and purchase price matters little when the loan is held to term. If a borrower makes 360 (30 x 12) equal payments, the composition of principal and interest is irrelevant. However, very few borrowers hold a loan to term as many sell or refinance.

Whether interest rates are high or low benefits certain parties and hurts others.

Low interest rates hurt cash buyers or those who utilize large down payments. A cash buyer would prefer to pay a very low price. Unfortunately, low interest rates inflate prices, so cash buyers are adversely impacted by low rates. Conversely, borrowers with little down benefit the most from low interest rates. Price to them is mostly about monthly payment since they are financing most of the transaction. Further, low interest rates followed by high inflation (conditions likely in our future) works strongly in favor of those with who put little down and borrowed heavily as the dollars they are repaying are worth less than the dollars they borrowed.

High interest rates strongly favor cash buyers. High interest rates make for low principal balances and low prices. High interest rates hurt borrowers who put little down because most of their payment goes toward interest. High interest rates followed by declining interest rates favors those who can refinance into a lower rate to reduce the interest burden.

It's very difficult to predict what will happen with interest rates and inflation. We are at the bottom of the interest rate cycle now, and higher rates and higher inflation are a possible, perhaps even likely, scenario. In any case, locking in a cost of ownership lower than the cost of a comparable rental is usually a good idea. The danger being a rise in interest rates that causes further weakening of prices which makes it impossible to sell without taking a loss. Landlording becomes the logical alternative, but that isn't for everyone.

Irvine prices are finally below rental parity

The low interest rates and falling prices have finally pushed Irvine below rental parity. Not every house in every neighborhood, but a broad spectrum of housing options are now trading at or below rental parity. It still takes effort to find these properties, but they are common enough to warrant searching in Irvine if you are looking to buy now.

The chart above was part of the OC Housing Market Presentation from last Wednesday. When I first prepared this chart last month, I was quite surprised to see Irvine trading below rental parity. The reading for September was the lowest in the last 11 years. Much of this improvement is due to low interest rates engineered by the federal reserve, but with their commitment to keeping rates low for the foreseeable future, waiting for the next interest rate peak to buy may take a while.

I remember early astute observers on the blog who quipped, “Irvine has never traded at rental parity.” Well, actually it has. In fact, it traded well below rental parity during the late 90s, and it will likely dip below rental parity again for at least the next few years.

I calculate the rental parity formula by taking 90% of the comparable rent and computing a loan balance. From there, I tack on a 20% down payment. I use 90% of the comparable rent to allow for taxes, insurance, HOA, and adjust for tax savings. Since there is no private mortgage insurance (PMI), most of the rent goes toward the payment.

FHA buyers face different conditions, so rental parity for them is calculated differently. I only use 75% of the comparable rent, and I add on a 3.5% down payment. Based on that standard, Irvine is still out of reach.

FHA buyers only make up a small percentage of Irvine resales, mostly concentrated in condos which is why we have seen so many of those sporting low prices.

The table below shows the degree of price inflation relative to rental parity by zip code.

The most inflated zip code remains 92603 — Turtle Rock, Turtle Ridge and Quail Hill. This zip code is deflating fast as relative price inflation has declined 40% over the last two months. Falling prices and falling interest rates will do that.

Northwood (92620) is also inflated, but prices are coming down.

Oak Creek, Orangetree and Portola Springs are the anomaly. Prices have been rising there for the last three months and are currently above rental parity. Rents are also rising in that zip code. We speculate this is due to restricted supply, but for whatever reason, it is the only zip code showing strength in Irvine.

Most of the remainder of Irvine is showing falling prices and firming rents. When combined with falling interest rates, the result is improving affordability as prices fall below rental parity. We anticipate this trend will continue and reach its zenith for this year's cycle in January. Prices over the next 6 months will generally be affordable by rental parity standards. With the uptick in foreclosure filings, there is no guarantee of a spring rally to pull the market out of the doldrums.

The buying window is open

I have consistently maintained on this blog that buying when prices are below rental parity is a good idea. I still believe that to be true. Rising prices are not a requirement for being bullish. Long-term owners who want to lock in a cost of ownership lower than comparable rents have options bubble buyers do not. The below rental parity buyer will be saving money each month, and if they have to move while prices are below their purchase price, they will be able to rent the property and avoid making a sale.

Prices are generally sticky on the way down, but they become much stickier when underwater owners don't need to sell to patch a hole in their family's balance sheet. Once prices reach rental parity, unless there is a huge influx of supply (which is still possible), prices generally don't go much lower. Of course, rising interest rates could easily lower the value of rental parity, and eventually this will happen, but the federal reserve seems committed to preventing higher interest rates in the medium term.

Owner-occupant who bought a Ponzi's house at auction

One of the topics Shevy will cover tonight at the REO and Short Sale Workshop is buying at the auction. It is one method owner occupants have for obtaining real estate below current market costs. The current owner of today's featured property bought it at auction about three years ago on 10/30/2008. His $547,000 purchase price represented a significant discount at the time. Even with the ongoing weakness in pricing, he will still be able to sell without losing money.

The previous owner was a full-blown Ponzi:

The house was purchased on 7/2/2002 for $481,000. The owner used a $384,800 first mortgage, a $96,200 second mortgage, and a $0 down payment.

On 8/12/2003 he refinanced with a $487,000 ARM with a 4% rate, probably a 1/1 ARM.

On 9/17/2003 he obtained a $97,500 HELOC. After only one year of ownership, he was able to pull out over $100,000.

On 4/14/2004, about seven months later, he refinanced again with a $560,00 ARM with a 3.87% interest rate and obtained a $70,000 HELOC.

On 11/16/2004, about sevens months later, he obtained a $150,000 HELOC.

On 8/31/2005 he refinanced with a $612,500 Option ARM with a 1% teaser rate and obtained a $175,000 HELOC. I wonder if this guy was a mortgage broker?

On 4/24/2006 he traded in his HELOC for a $250,00 stand-alone second mortgage.

In three and one half years, after putting no money down, this Ponzi cashed out $381,500. That's an average of $109,000 per year!

He defaulted shortly thereafter and squatted for about 15 months.

Foreclosure Record

Recording Date: 02/22/2008

Document Type: Notice of Sale

Foreclosure Record

Recording Date: 09/17/2007

Document Type: Notice of Default

Since most of the worst HELOC abusers have already been flushed from the system, I haven't profiled many really bad cases lately. This guy was a real blast from the past. He's a good reminder of the problems of the housing bubble.

When I first saw this property, I felt it was one of the nicer properties we have seen trading below rental parity — unless you believe you can find a rental this nice for less than $2,500 per month. It's deal like this one on nicer properties that are becoming more prevalent, and the reinforce what I am seeing in the data. Much of Irvine is now at or below rental parity.

Welcome to the wonderful Northwood community in Irvine. This home features a remodeled kitchen with dual ovens, 6 burner cooktop and a Subzero fridge. The master suite features a balcony for you to relax on. The property also has jacuzzi and pool to enjoy those warm summer days. There are many other upgrades done to this home for you to come view.

——————————————————————————————————————————————-

Proprietary IHB commentary and analysis

Resale Home Price …… $649,000

House Purchase Price … $547,000

House Purchase Date …. 10/30/2008

Net Gain (Loss) ………. $63,060

Percent Change ………. 11.5%

Annual Appreciation … 5.7%

Cost of Home Ownership

————————————————-

$649,000 ………. Asking Price

$129,800 ………. 20% Down Conventional

4.20% …………… Mortgage Interest Rate

$519,200 ………. 30-Year Mortgage

$125,290 ………. Income Requirement

$2,539 ………. Monthly Mortgage Payment

$562 ………. Property Tax (@1.04%)

$0 ………. Special Taxes and Levies (Mello Roos)

$135 ………. Homeowners Insurance (@ 0.25%)

$0 ………. Private Mortgage Insurance

$0 ………. Homeowners Association Fees

============================================

$3,237 ………. Monthly Cash Outlays

-$416 ………. Tax Savings (% of Interest and Property Tax)

-$722 ………. Equity Hidden in Payment (Amortization)

$195 ………. Lost Income to Down Payment (net of taxes)

Whoa,yeah you know I need to be free (that's what I want)

Oh, now give me money money! (that's what I want)

The Beatles — Money

Money won't buy happiness, but it can provide the finest forms of misery. Everyone wants money. If given the chance to do nothing and obtain money, most people would take it. Such was the lure of the housing bubble.

People only had to do two things to obtain copious amounts of cash. First, they needed to buy a house. Then they needed to find a lender who would give them money for signing some paperwork. That's it. No work, no skills, no risk, no sacrifice, nothing. Buy a house, sign some papers, and anyone could obtain hundreds of thousands of dollars. It shouldn't be surprising that kool aid intoxication is so strong. Who wants to give up on that deal?

Unfortunately, as with most things in life that are too good to be true, the housing boom was not real or sustainable. Equity is an illusion, but debt is very real. The debt hangover is still plaguing the country. Our banks are imperiled by the toxic debts polluting their balance sheets, and borrowers are burdened by debt service payments to the ailing banks. This debt service is money that could be circulating in the economy as demand for goods and services. Instead, the money that should be creating aggregate demand is being sucked into the black hole of banking losses and dragging down the entire economy.

Employment Lost in Property Crash Weighs on the Economy's Chance of Recovery

By S. MITRA KALITA — October 5, 2011

HAGERSTOWN, Md.—Joshua Bradley says it was the easiest job he ever had: power-washing windows of new suburban houses. Then, about three years ago, business dried up and he found himself out of work.

“People don't want to get anything done to their houses anymore,” says Mr. Bradley, 28 years old. “They do it themselves to save money.”

His experience wasn't unusual.

Over the past decade, the housing market has been a powerful engine: It helped the U.S. economy out of a recession and created jobs as construction firms took on workers and new homeowners hired contractors to decorate rooms and maintain the lawns, or purchased new furniture for indoors and outdoors.

But today, as the sector endures a prolonged slump, many of the jobs it created are gone, and housing has now become part of what many economists see as a vicious circle that has left the wider economy struggling to gain altitude.

Americans aren't spending because their home values are declining and employment prospects are dimming, and housing and employment is struggling because Americans won't spend.

“People are losing their jobs and never getting equivalent jobs,” says Yale University economist Robert Shiller. “That fear is spooking everyone, so people aren't in a mood to expand.”

It isn't that people won't spend, they can't spend. Borrowers everywhere have too much debt, and they aren't being given more Ponzi loans to make payments and buy more stuff. It's the natural result of a massive credit binge. Take a look at the size of the green area representing disposable income in the chart below.

In the past 10 years, housing and related sectors grew to represent an outsize portion of the economy, accounting for 16.8% of GDP in 2005, according to Capital Economics. That fell to 13% in the second quarter of this year, the lowest share since 1982.

“The whole U.S. economy in this last decade was built on housing and the services that come with it: mortgages, moving, furniture,” says Steve Blitz, director and senior economist at ITG Investment Research in New York.

That is evident in such boom-to-bust markets as Hagerstown. Like Mr. Bradley, many now-unemployed workers in the city, which lies 75 miles from Washington, D.C., had a direct or indirect connection to housing. Some worked in the construction jobs supported by the surge in development; others worked in nearby distribution centers for retailers such as PetSmart and Staples, where new homeowners shopped. Some created small businesses catering to new residents, often tapping into home equity to do so.

Does anyone else think this is a bad idea? Is it wise to risk the family home on a business start up?

But then the housing bust arrived. The number of building permits for new construction in Hagerstown fell nearly 75% between 2006 and 2010, from 212 to 55, according to Sage Policy Group Inc., a Maryland economic-consulting firm. In July, the median price of a home in Washington County was $130,450, down nearly 45% from its $235,000 peak reached in June 2007.

Unemployment in the city has been particularly stubborn, climbing to 11.3% in June from 10.7% a year earlier. The national rate fell from 10.5% to 9.8% over the same period.

During the boom years, Hagerstown ranked among the highest for positive mortgage equity withdrawal—meaning people pulling cash out of their houses. Now, it ranks among the most negative, meaning families are defaulting or paying down debt, according to Moody's Analytics.

Hagerstown was taken over by Ponzis. The few who didn't participate get to pay the price in government bailouts and lowered property values.

On a recent afternoon, amid vacant storefronts and “for rent” signs, Karla Auch stood before her downtown gift shop, the Rainbow Connection, opened six years ago with a home-equity loan. “Going out of business,” announces a sign on the front.

“A lot of new businesses came in with all the people. We tried. It never really boomed,” Ms. Auch says.

People such as Charles Wible, a lifelong Hagerstown resident who left school in the 11th grade, see an uncertain future ahead. Mr. Wible, 39 years old, installs garage doors and says he had a nice life during the housing boom.

“Ten years ago, I was making $60,000 a year and working half as hard as I am now,” he says. “Now I'm making $25,000 a year and scrounging for work.“

Everyone who depended on real estate is facing this problem. How many realtors are complaining about the same issue?

The loss of jobs and businesses has led to high foreclosure rates across the U.S.; according to the National Association of Realtors, 31% of transactions in August were distressed sales. Credit, meanwhile, is tight, and banks are loath to lend in areas like Hagerstown, with home prices still falling.

Hagerstown resident Machiel van de Geer says he and his neighbors take turns mowing the lawn of foreclosed properties.

There is no obvious fix to the city's economic quandary—or the country's. “The only solution here is jobs,” says Anirban Basu, chairman and chief executive of Sage Policy Group and an expert on Maryland's economy. “In the absence of a resurgence of employment, a recovery in Hagerstown's housing market is impossible.”

But where the jobs will come from remains elusive. Mr. Bradley, for example, switched industries and found work as a shift supervisor at the Hard Times Café, a local restaurant. But every day brings a slew of people just like him to the restaurant looking for work, he says.

“We've got to invest in software, technology, manufacturing,” says Mr. Blitz, the ITG economist. “It's these industries that will create more jobs and income. We are transitioning from an economy built around the leverage on housing and finance to an economy built on real goods.”

The economy won't recover until some sector other than real estate creates new jobs. Once some other sector creates jobs, new households will form which will in turn create demand for real estate. With fresh demand for real estate, housing employment will start to recover, and the demand will snowball from there. The catalyst will not be housing. It must start in another sector of the economy.

Here, officials point to a business-technology park under construction. It would link Hagerstown Community College with the city's new hospital, in hopes of spurring jobs in biotechnology, health sciences and information technology.

For some it will come too late. Mr. Wible says he didn't expect a turnaround in his lifetime, so he's banking on his four sons.

“They are not building houses like they used to,” he says. “So I try to instill in my boys to stay in school. I don't want my boys out there fighting for work like I have to.”

—Nick Timiraos contributed to this article.

That is capitulation.

HELOC Abuse and Pascal's Wager

During the housing bubble, I can remember having conversations with kool aid intoxicated fools concerning house prices and mortgage debt. They would tell me house prices only go up, so it doesn't matter how much you borrow because the house will always pay for it. When the debt became expensive, you could serial refinance into one teaser rate Option ARM after another.

When I suggested that lenders may not always offer these teaser rates and that cheaper and cheaper credit might not always be made available, most scoffed at me as a fool who didn't understand California real estate finance. When i asked people to tell me what would happen if house prices did not go up, or if interest rates went up, or if credit became tight, they would look at me with a blank stare or tell me I worried about stuff that would never happen.

Whenever I had these conversations, I was always reminded of Pascal's Wager. Pascal's Wager is an idea from philosophy first postulated by Blaise Pascal. He believed a rational person should wager as though God exists, because living life accordingly has everything to gain, and nothing to lose. So it is with HELOC debt.

I was always under the belief system that one should not wager the family home on the necessity for prices to always increase and cheap debt to always be made available. Many California loan owners wagered their family homes for a little spending money… well, actually a lot of spending money. But no matter what benefit people thought they would obtain from borrowing irresponsibly, they should never have wagered their family homes on it. They did make this wager, and they all lost. Given the stupidity of that mistake, it's hard to feel too sorry for them.

Keeping up appearances

Many people fell victim to HELOC abuse due to their own frailties of ego. Far too many were trying to keep up with the Joneses while the Joneses were juicing on a HELOC high. I have no idea what motivated the owners of today's featured property to spend their home, but they bought before the bubble began to inflate, and they are now a short sale. They wouldn't have this problem if they wouldn't have tripled their mortgage debt.

Today's featured property was purchased on 6/8/2000 for $260,000. The owners used a $208,000 first mortgage and a $52,000 down payment.

On 3/17/2003 they obtained a $100,000 HELOC.

On 7/25/2003 they enlarged the HELOC to $133,000.

On 8/27/2004 they opened a $250,000 HELOC.

On 12/12/2005 they refinanced with a $434,000 first mortgage.

On 4/4/2006 they obtained a $200,000 HELOC.

On 5/9/2008 they got a $300,000 HELOC.

On 5/14/2009 they got another loan for $150,000.

On 8/25/2011 they got one last loan for $108,000.

Total property debt is $734,000 based on the $434,000 first and the $300,0000 HELOC.

Total mortgage equity withdrawal is $526,000.

These borrowers withdrew more money in HELOCs and refinances than the house is currently worth!

A great opportunity to own in the heart of Irvine. This nice home is located in a quiet community. Open floor plan with a bright and airy high-vaulted ceiling. This home features 3 spacious bedrooms and 2.5 baths. 2 car direct access garage w/ lots of space for storage. Wood floors all throughout the house. Nice sized backyard, good for relaxation. Homeowner's Association includes pool and spa. Convenient location. Award-winning schools: Culverdale, Westpark, SoLake Middle School and University High.

——————————————————————————————————————————————-

Proprietary IHB commentary and analysis

Resale Home Price …… $449,000

House Purchase Price … $260,000

House Purchase Date …. 6/8/2000

Net Gain (Loss) ………. $162,060

Percent Change ………. 62.3%

Annual Appreciation … 4.8%

Cost of Home Ownership

————————————————-

$449,000 ………. Asking Price

$15,715 ………. 3.5% Down FHA Financing

4.03% …………… Mortgage Interest Rate

$433,285 ………. 30-Year Mortgage

$131,575 ………. Income Requirement

$2,076 ………. Monthly Mortgage Payment

$389 ………. Property Tax (@1.04%)

$50 ………. Special Taxes and Levies (Mello Roos)

$94 ………. Homeowners Insurance (@ 0.25%)

$498 ………. Private Mortgage Insurance

$292 ………. Homeowners Association Fees

============================================

$3,399 ………. Monthly Cash Outlays

-$323 ………. Tax Savings (% of Interest and Property Tax)

-$621 ………. Equity Hidden in Payment (Amortization)

$22 ………. Lost Income to Down Payment (net of taxes)

A Harvard economist has recommended principal forgiveness to address the problem of falling house prices. It is the worst policy option being considered today.

But we've been going through this thang since way back

I told ya when I get the dough I would pay back

But I got problems baby

¦yea, if you only knew

I got bigger problems baby

J. Cole — Problems

Lenders and loan owners have problems. Lenders made loans their borrowers can't repay, and now both parties to the deal are turning to the US taxpayer for a bailout. Somehow, these two groups have convinced themselves they deserve some of my money. I was not a participant in their transaction. I did not sign on to the risks and rewards of the deal they made, yet both groups feel I should be compelled to bail them out. Screw them both. Their problem is not my problem.

There is a problem here: excessive debt. There is also a solution in the system: foreclosure and bankruptcy. Both parties to this private financial transaction want to avoid the consequences of foreclosure and bankruptcy because it will cost banks their money and borrowers their houses and their credit. Moral hazard dictates both parties should endure the consequences of their actions or they will repeat their mistakes.

The most important step in solving any problem is to define the problem correctly. Failure to carefully identify the problem will inevitably lead to solutions which don't have the desired effect. In fact, many solutions implemented to solve a poorly defined problem actually make conditions worse.

Falling house prices is not the problem

Currently across the country, many people have identified falling house prices as a problem.

Bankers believe falling house prices are a problem because it erodes the value of the collateral backing up their loans. If they need to foreclose on a delinquent borrower, they don't obtain their original loan capital. To make matters worse, falling home prices actually motivate their borrowers to stop making loan payments which exacerbates the problem. For bankers, falling house prices are a problem.

Homeowners believe falling house prices are a problem because it erodes their wealth. Historically, houses have been a reservoir of equity and a vessel that retains wealth. For homeowners, falling house prices are a problem to the degree they depended upon the value of their house for savings, retirement or income supplementation.

Economists believe falling house prices are a problem because it inhibits consumer spending. The negative wealth effect causes people to save rather than spend, and the decreasing value of houses shuts off the home ATM machine. For economists who don't seem to care where demand comes from, falling house prices are a problem.

Each of the above groups views the world through their own prism, and each of them has a legitimate reason to believe falling house prices are a problem. However, they are all wrong. For the broader society, falling house prices are not a problem. Falling house prices mean buyers are less indebted when they purchase real estate. Lower debt levels means homeowners have more disposable income. Increased disposable income creates sustainable demand, unlike Ponzi borrowing which only creates demand as long as more credit is being extended to the borrower.

Debt is the problem

The real problem in our economy — the problem incorrectly identified by economists — is excessive debt. And the only way to solve that problem without major side effects of moral hazard is through foreclosure and bankruptcy.

With foreclosure and bankruptcy, both lenders and borrowers endure consequences for their behavior. The lender losses money, and given the loan practices of the housing bubble, they deserve to lose money. The borrower losses their house and endures restricted access to credit for a time — both of which are appropriate consequences for taking on a debt they could not repay. If neither party experiences these consequences, the mistakes of the past will be repeated. That's the essence of moral hazard.

Bankers and loan owners are the two groups who both agree falling house prices are a problem. However, this is only a problem for them. The problems between bankers and loan owners do not impact me as a renter except to the degree they reach into my pocket through government policy for bailout money. If both parties weren't seeking bailouts I am being asked to pay for, falling house prices would be akin to falling stock prices, a loss endured by private parties which might make the news but wouldn't impact my life.

Economists fail to identify the real problem

Some economists get lost in the abstractions of their own theories. They lose site of the impact their proposals have on behavior. For example, many economists believe stimulating demand through mortgage equity withdrawal is a good thing. They call it the “wealth effect.” They completely miss the fact this borrowing quickly degrades into a Ponzi scheme and debt dependency. Mortgage equity withdrawal is not a sustainable form of demand, and stimulating it merely creates the conditions for a larger crash and a more prolonged recession.

To exacerbate their mistake, economists fail to recognize the economic problems of the last four years are a direct result of the Ponzi borrower and wealth effect spending they advocate. Since they don't see the causes of our problems, they devise solutions which call for more Ponzi borrowing and spending. Debt does not create wealth.

Since economists have wrongly identified falling house prices as the root of our problems, they have wasted much brainpower to devising solutions with the wrong goal in mind. Some of these solutions — like lowering interest rates — create economic distortions and mis-allocations of capital. Other solutions — like government mandated loan modifications — are a threat to contract law and the stability of our mortgage lending system. The worst solutions — like today's suggestion that we forgive principal — create more widespread problems by altering borrower incentives and propagating moral hazard.

HOMES are the primary form of wealth for most Americans. Since the housing bubble burst in 2006, the wealth of American homeowners has fallen by some $9 trillion, or nearly 40 percent. In the 12 months ending in June, house values fell by more than $1 trillion, or 8 percent. That sharp fall in wealth means less consumer spending, leading to less business production and fewer jobs.

Fallacy #1: the wealth effect. Lower house prices means the new buyer is less indebted than the old one. This new buyer will have more disposable income and thereby stimulate the economy. Only this time, the demand will be sustainable because it is income based rather than debt based.

But for political reasons, both the Obama administration and Republican leaders in Congress have resisted the only real solution: permanently reducing the mortgage debt hanging over America. The resistance is understandable. Voters don’t want their tax dollars used to help some homeowners who could afford to pay their mortgages but choose not to because they can default instead, and simply walk away. And voters don’t want to provide any more help to the banks that made loans that have gone sour.

He has missed the most obvious reasons voters like myself don't want to see principal reduction.

First, it isn't strategic defaulters I am concerned about. They left the house, and they may have lingering debt issues yet to be resolved. The real problem is the borrowers who took on too much debt but hope to dodge the consequences. This breaks down into two groups: late buyers and HELOC abusers.

The late buyers who overextended themselves made a choice. During the bubble, I chose not to buy more house than I could afford. Many people who made less money than I did chose to over-extend themselves and occupy the house which should have been affordable to me. It's a bit like cutting in line. In the process, they bid up home prices and priced me out of the housing market. Now I am being asked to pay for their imprudence with bailouts — after they have been living in my house for the last several years. I feel like I am being robbed twice.

The HELOC abusers obviously don't deserve principal forgiveness. Anyone who was prudent during those times should not be asked to pay the bills of the fools who spent like drunken sailors, yet that is what we are being asked to do with widespread principal reductions.

But failure to act means that further declines in home prices will continue, preventing the rise in consumer spending needed for recovery.

This contention is just wrong. Falling house prices will stimulate the recovery as it will put more money into the hands of consumers. We don't need another debt-fueled Ponzi scheme to save the economy. If we just let prices fall to their natural bottom and allow borrowers to borrow less, the extra disposable income will create the recovery we want to see.

As costly as it will be to permanently write down mortgages, it will be even costlier to do nothing and run the risk of another recession.

Bullshit.

House prices are falling because millions of homeowners are defaulting on their mortgages, and the sale of their foreclosed properties is driving down the prices of all homes. Nearly 15 million homeowners owe more than their homes are worth; in this group, about half the mortgages exceed the home value by more than 30 percent.

Most residential mortgages are effectively nonrecourse loans, meaning creditors can eventually take the house if the homeowner defaults, but cannot take other assets or earnings. Individuals with substantial excess mortgage debt therefore have a strong incentive to stop paying; they can often stay in their homes for a year or more before the property is foreclosed and they are forced to move.

The overhang of mortgage debt prevents homeowners from moving to areas where there are better job prospects and from using home equity to finance small business start-ups and expansions. And because their current mortgages exceed the value of their homes, they cannot free up cash by refinancing at low interest rates.

I give this man credit for accurately identifying the conditions in the market. What is shocking is how incorrectly he identifies the problem and thereby botches the solution.

The Obama administration has tried a variety of programs to reduce monthly interest payments. Those programs failed because they didn’t address the real problem: the size of the mortgage exceeds the value of the home.

Yes, and the solution — which is already outlined in the mortgage agreement — is for the borrower to vacate the property and the lender to recover what they can of their capital in a foreclosure auction.

The problem with loan modification programs is that they try to keep borrowers in homes they cannot afford. It can't be done fairly or without moral hazard. Would you borrow prudently if you knew the government would bail you out if you got in trouble?

To halt the fall in house prices, the government should reduce mortgage principal when it exceeds 110 percent of the home value. About 11 million of the nearly 15 million homes that are “underwater” are in this category. If everyone eligible participated, the one-time cost would be under $350 billion.

No, no, no! Not $350 billion. Not $350. Not one penny for principal reduction from my tax dollars.

Here’s how such a policy might work:

If the bank or other mortgage holder agrees, the value of the mortgage would be reduced to 110 percent of the home value, with the government absorbing half of the cost of the reduction and the bank absorbing the other half.

The government is going to absorb half the losses from the banks? How isn't that a massive government bailout of the banks? This is a bank bailout disguised as a loan owner bailout, and in my opinion, both should go down in flames.

For the millions of underwater mortgages that are held by Fannie Mae and Freddie Mac, the government would just be paying itself.

I can't believe an economist actually wrote that. [shakes head in disbelief] The government would not be paying itself. It would be paying the investors in mortgage-baacked securities insured by the GSEs, and the bondholders of the GSEs.

And in exchange for this reduction in principal, the borrower would have to accept that the new mortgage had full recourse — in other words, the government could go after the borrower’s other assets if he defaulted on the home. This would all be voluntary.

So every loan owner with no assets will immediately sign up for this program because they had nothing to lose anyway. Plus every borrower in a state like Nevada, where all loans are recourse anyway, would also sign up immediately. And would this agreement supersede state laws to the contrary? In Nevada recourse loans are extinguished after nine months if the lender doesn't try to collect. And does anyone believe the government would actually go after delinquent borrowers, or would they merely forgive the debt themselves in the end?

This plan is fair because both borrowers and creditors would make sacrifices. The bank would accept the cost of the principal write-down because the resulting loan — with its lower loan-to-value ratio and its full recourse feature — would be much less likely to result in default. The borrowers would accept full recourse to get the mortgage reduction.

Those are sacrifices? The bank is getting reimbursed for half its loss, and the borrower is getting to stay in their home. It appears to me as if both parties are escaping all consequences for their foolish behavior. Lenders will be given a green light to underwrite more dodgy loans, and borrwers will be encouraged to take on massive debts with the promise of principal forgiveness. It's the worst possible set of incentives, moral hazard in extreme.

Without a program to stop mortgage defaults, there is no way to know how much further house prices might fall.

Yes, there is. Prices will fall until they are affordable and new buyers come forward to absorb the inventory because owning is cheaper than renting. If the supply is excessive, like it is in Las Vegas, then cashflow investors will step in to supplement the demand when prices get low enough to attract their attention. The market has self-correcting mechanisms if they are allowed to work.

Although house prices in some areas are already very low, potential buyers continue to wait because they anticipate even lower prices in the future.

This effect is over stated. Buyers will react to affordability. If prices are low enough, people will buy to save money versus renting even in a declining market.

Before the housing bubble burst in 2006, the level of house prices had risen nearly 60 percent above the long-term price path. So there is no knowing how far prices may fall below the long-term path before they begin to recover.

I cannot agree with those who say we should just let house prices continue to fall until they stop by themselves. Although some forest fires are allowed to burn out naturally, no one lets those fires continue to burn when they threaten residential neighborhoods.

For years the US Forest Service was dominated by timber production interests. It was a classic example of regulatory capture. The US Forest Service's primary objective, and thereby its land management policies, favored timber production. Forest Fires were seen as an obvious threat to timber production, so policies of fire suppression were absolute: put out all fires as quickly as possible, and do not let anything burn. This was forest service policy for several decades.

To its chagrin, the US Forest Service discovered its policy was flawed. By not allowing small fires to burn, leaf litter and other combustible natural growth accumulated. In unmanaged forests, periodic fires eliminate this source of fire fuel. In managed forests this accumulation of fuel fosters fires that get out of control (think Yellowstone).

To combat the accumulation of fire fuel, the US Forest Service changed its policies. Now, small fires in the understory are permitted to burn. By eliminating the excess fuel, the more dangerous and costly canopy fires are avoided. A few trees may get damaged in the small fires, but the forest survives.

We must allow the fire to wipe out the debts of residential home owners. Only then will the green shoots of the next forest have the sunlight to take root and prosper. So it is with the new homeowners who will be buying in at lower price points.

Back to the conclusion of the op-ed:

The fall in house prices is not just a decline in wealth but a decline that depresses consumer spending, making the economy weaker and the loss of jobs much greater. We all have a stake in preventing that.

Martin S. Feldstein, a professor of economics at Harvard, was the chairman of the Council of Economic Advisers from 1982 to 1984 under President Ronald Reagan.

He repeats his fallacious argument that the wealth effect is necessary to stimulate the economy. It's shocking that a man with such impressive credentials is so completely wrong about what should be done.

Whenever I read this kind of crap from an intelligent writer, the cynic in me wonders if the author is being paid off by powerful interests who endorse this policy. Did his banking buddies put him up to this? Or is he a loan owner hoping for a personal bailout? Or is it preferable to conclude he had no nefarious motives, and instead he is a fool?

Countrywide's Option ARM with a 1% teaser rate

Bank of America is desperate for cash. They bought the toxic waste from Countrywide, and now the stupid loans like the one on today's featured property are eating a hole in their balance sheet.

This property is typical of the kind of loan I don't want to see bailed out. The former owner of this property couldn't afford it. He used a $624,000 Option ARM with a 1% teaser rate because he obviously couldn't afford a fully amortized payment. If the banks who underwrote these loans and the borrowers who used them are bailed out, what will they learn? They will learn that no matter how stupid and irresponsible they are, the government will remove any negative consequences for their decisions.

The former owner of this property and the bank who loaned him money were part of the problem. Their actions together inflated the housing bubble. They priced the prudent borrowers out of properties and forced them to rent and wait. We are still waiting.

The former owner of this property did endure consequences. He was foreclosed on, and with the HELOC debt he added to the mortgage, he will likely need to declare bankruptcy to wipe the slate clean. Bank of America is only getting a fractioin of the value they believed they acquired when they obtained this asset in the Countrywide deal. Both parties are experiencing consequences for their actions. So what's wrong with that?

Why do we need to bail out the parties to this stupid loan? What societal benefit will we obtain? Continually inflated house prices and more Ponzi borrowing? That's a benefit we can all do without.

REO BANK OWNED PROPERTY!!Beautiful condo close to lake! Has 3 bedrooms and 2.5 bathrooms. There is a half bath upstairs and all three bedrooms upstairs. Has an open floor plan with plenty of room. There is carpet through the bedrooms, stairs, and hallway. There is a fireplace in the family room. The backyard is set up great for entertaining. Association has a pool and spa for everyone to enjoy. Don't miss this opportunity to buy a bank owned home!

——————————————————————————————————————————————-

Proprietary IHB commentary and analysis

Resale Home Price …… $535,900

House Purchase Price … $780,000

House Purchase Date …. 9/22/2005

Net Gain (Loss) ………. ($276,254)

Percent Change ………. -35.4%

Annual Appreciation … -6.0%

Cost of Home Ownership

————————————————-

$535,900 ………. Asking Price

$107,180 ………. 20% Down Conventional

4.20% …………… Mortgage Interest Rate

$428,720 ………. 30-Year Mortgage

$119,017 ………. Income Requirement

$2,097 ………. Monthly Mortgage Payment

$464 ………. Property Tax (@1.04%)

$0 ………. Special Taxes and Levies (Mello Roos)

$112 ………. Homeowners Insurance (@ 0.25%)

$0 ………. Private Mortgage Insurance

$402 ………. Homeowners Association Fees

============================================

$3,075 ………. Monthly Cash Outlays

-$344 ………. Tax Savings (% of Interest and Property Tax)

-$596 ………. Equity Hidden in Payment (Amortization)

$161 ………. Lost Income to Down Payment (net of taxes)

My parents both retired from school system work last year. I grew up in a household where education was a focus, and public school issues were a common topic of discussion.

Many people believe certain schools have good test scores because they have better teachers. That usually isn't the case. While it's true that good teachers prefer to teach in highly rated schools, the quality of teaching isn't what makes test scores better. Good schools are largely a product of involved parents and motivated students. It's rare to find a school where the parents are heavily involved and the test scores are poor. It's equally rare to find a school where the test scores are good and the parents have other priorities.

Good test scores are like gravity. A good school attracts the most involved parents who place an emphasis on education and get involved in the school and with their children. In other words, good test scores beget good test scores. This is one of the reasons poor school test performance problems are so intractable. The worst performing schools are populated by students whose parents don't value education, don't get involved with the school, and don't motivate their children to succeed.

Everyone is searching for an answer to bring the quality of education up. Unfortunately, the real problems with education cannot be addressed in the classroom. The problems start at home and resonate through the community.

Donald Bren built a $12 billion fortune as a Southern California real estate developer and has been focused on philanthropic giving to support education. That includes gifts at the university level to UC Irvine and UC Santa Barbara as well as to K-12 schools in the city of Irvine (in Orange County), which his Irvine Co. master-planned and developed, and after school program Think Together.

Bren shared his thoughts with Forbes via email.

Donald Bren, real estate developer and philanthropist

FORBES:What is your best single idea for reforming K-12 education?

BREN: In my opinion, education is the finest gift an individual can give a young person. And many of our public schools are falling short in successfully educating the youth of our country today.

Gone are the days when state governments are fully able to fund our public schools. Future public education will require involvement and collaboration among various local, civic, private and nonprofit entities, a concept I like to refer to as “community entrepreneurship. ”

Irvine schools have been successful because of the community involvement. Once these schools gained a reputation, they became a magnet for people who value education — which is exactly what Donald Bren had in mind.

Over the past 30 years, I have sought to implement community entrepreneurship to benefit our local kindergarten through twelfth grade schools, working in partnership with community leaders, local school districts and well-run nonprofit organizations.

For example, in master planning and master building the new City of Irvine, we have gone to great lengths to ensure our elementary schools and neighborhood parks are contiguous and a focal element creating the important activity center for each residential community.

When state funding for Irvine public schools began to diminish some time ago, my Irvine Company colleagues helped me to provide private funding support for continuation of basic science, art and music programs that had been eliminated by lack of state funding. Additionally, we have developed annual teacher recognition and reward programs that provide financial awards for teachers who demonstrate outstanding results in educating our students.

By making capital available for unfunded programs and providing a balanced curriculum and financial incentives to teachers based on results, Irvine Unified School District continues to rank among the finest educational systems in the nation.

Yes, they are.

My additional observations for K-12 schools are:

1) Return full governance and financial control to the local school district board and the parents – they know best.

2) Eliminate the large bureaucratic administrative overhead expenses that prevent necessary funding from reaching classrooms.

My school teacher parents used to complain about the huge bureaucracy that seemed to exist only to consume resources.

3) Maximize the existing investment in school buildings and equipment by operating the school campus on a four-quarter or year-round basis.

4) Compensate professional teachers on a year-round basis, similar to most businesses and government. By the way, education is big business and should be approached in a similar disciplined manner.

5) Making a difference requires focus. Academic administrators will tell you that the most important school years are kindergarten through sixth grade, when students develop confidence in their ability to learn and foundational study skills. Focus efforts on the early years before trying to fix high school programs that often provide too little too late.

6) Consider a higher level European-style baccalaureate program for certain schools, and as an example, reducing the need for rudimentary freshman English classes at our prestigious University of California.

7) And don’t forget, students are living in a digital world where computers and information technology are used at home, at school and in everyday life. They must learn the new methods of our “plugged-in” society.

The classrooms at my son's school are full of computers.

FORBES: Is there any person or any school who you think is doing a good job of improving/reforming k-12 education now?

BREN: In my opinion, the person doing the best job improving education in California is Randy Barth, President and CEO of THINK TOGETHER in Santa Ana, Calif. He is the most dedicated and innovative professional in K-12 tutoring and mentoring education in California.

THINK TOGETHER provides academic learning through specially designed after-school and summer programs throughout Southern California to more than 100,000 students. With special attention given to areas such as the Santa Ana Unified School District, with more than 50,000 underprivileged K-6 students, the majority of whom have little chance to get ahead without this unique program. Thus the results are encouraging – academic improvement scores have been off the charts, so to speak.

Fixing our K-12 education system requires a new solution to a growing national problem. Community entrepreneurship is my recommendation, as it will bring together the necessary resources to make a difference. Our children are worth the extra human effort and investment.

I’m proud to be among a group of dedicated community entrepreneurs focused on improving our community education programs.

I live in Irvine for the schools

For those of you who have attended my Las Vegas cashflow presentations, you have heard about my son. I am the parent of a special needs child.

My son is a slow learner, and he has limited language and social skills. He is labeled as autistic, for whatever that means. All my wife and I know is that we love him, and he is an endless source of joy and happiness.

I get to spend a great deal of time with him, particularly now that I work from home. I see him for each morning as he and I make breakfast together. Most evenings we get some time to play video games or just hang out. He likes when I read books to him, and his skills at Mario Kart or Super Mario Brothers are remarkable. On Sunday morning, you can most often find us at Disneyland. I can't count how many times I have been on Splash Mountain, Space Mountain, Indiana Jones, Pirates of the Caribbean, Big Thunder Mountain, and the Matterhorn Bobsleds. It's the most precious time of my week. I will never look back and feel I missed out on enjoying my son as he grew up.

My wife and I have thought about leaving Irvine on many occasions. We have considered San Clemente, Ladera Ranch, Las Vegas, and other areas, but when we really think about moving out of Irvine, we think about the education program we would leave behind, and we change our minds. The Irvine special needs programs are truly outstanding. When I factor in the cost of providing this education privately, the cost of renting in Irvine seems reasonable. It would be much more expensive to rent or own somewhere else and have to provide a comparable private education.

The Irvine Schools do add value to Irvine Homes

The bottom line is that people willingly pay the Irvine rental and ownership premium to be in the Irvine school system. We know several parents who moved here from other school districts and even from out of state to have their special needs child educated in Irvine. Parents of typical children come here for the same reason. The high test scores are a big draw. Parents will do whatever they must to give their child every advantage. If that means paying extra to live in the best school district, that's what parents will do.

The responsible bagholder

HELOC dependency and abuse is deeply embedded into the California psyche. The property records on today's featured property show a HELOC abuser who sold it to a responsible bagholder who simply couldn't afford the property. Perhaps unemployment or a loss of income was a factor, but the later buyer didn't add to their mortgage, and they still lost the home. It's now an REO.

The story begins on 11/10/1998 when the property was purchased for $260,000. The buyers used a $234,450 first mortgage and a $25,050 down payment. The refied twice for $290,000 and $322,700 respectively taking out a little less than $90,000 in the process. Based on the frequency and amount of these withdrawals, those owners were clearly using their HELOC money to supplement their incomes.

Despite the bad habits those owners formed, they were amply rewarded when the sold the property to the bagholder on 5/7/2004 for $542,500. The subsequent owner used a $406,875 first mortgage and a $135,625 down payment. They never refinanced or took out any HELOC money.

The bagholder was unable to sustain the payments on their first mortgage, and the property went to auction on 4/5/2011 for $414,265. If the bank gets their asking price, they are out the amount of commissions buy little more. The 2004 buyer is out their entire $135,625 down payment, and their credit is shot. If they knew they were going to suffer those consequences, they probably would have refinanced and maxed out some HELOCs.

Chase has the property now, and they are hoping to sell it and get most of their loan balance back. At this price, they probably will.

This Chase Bank Owned property has been freshly painted and new carpet installed. This is the largest model in the Parkside Tract. Lots of room for a 3 bedroom, 2.5 bath home. Only one common wall for this townhouse style condo. Fireplace in the living room with 2 skylights. Formal dining, family room, new stove just installed in kitchen. Garage has direct access. Rare long driveway for Irvine. High vaulted ceilings. Secondary bedrooms are on opposite side of hall of Master Bedroom for more privacy. No neighbors behind property for increased privacy. Property is located in the Village of Woodbridge – one of the best communities to live in. Many pools, parks, Lakes with boating and Lagoons for Beachcombers, volleyball, basket ball courts, tennis clubs, too many HOA activities to list for adults, children, and families. Close to shopping, banks, houses of worship, schools, movie theaters – all in the heart of Irvine. Look at MLS MEDIA for disclosures.

——————————————————————————————————————————————-

Proprietary IHB commentary and analysis

Resale Home Price …… $419,900

House Purchase Price … $542,500

House Purchase Date …. 5/7/2004

Net Gain (Loss) ………. ($147,794)

Percent Change ………. -27.2%

Annual Appreciation … -3.4%

Cost of Home Ownership

————————————————-

$419,900 ………. Asking Price

$14,697 ………. 3.5% Down FHA Financing

4.03% …………… Mortgage Interest Rate

$405,204 ………. 30-Year Mortgage

$122,783 ………. Income Requirement

$1,942 ………. Monthly Mortgage Payment

$364 ………. Property Tax (@1.04%)

$0 ………. Special Taxes and Levies (Mello Roos)

$87 ………. Homeowners Insurance (@ 0.25%)

$466 ………. Private Mortgage Insurance

$313 ………. Homeowners Association Fees

============================================

$3,172 ………. Monthly Cash Outlays

-$302 ………. Tax Savings (% of Interest and Property Tax)

-$581 ………. Equity Hidden in Payment (Amortization)

$21 ………. Lost Income to Down Payment (net of taxes)

.png)

.png)

.jpg)

.png)

The economy won't recover until some sector other than real estate creates new jobs. Once some other sector creates jobs, new households will form which will in turn create demand for real estate. With fresh demand for real estate, housing employment will start to recover, and the demand will snowball from there. The catalyst will not be housing. It must start in another sector of the economy.

The economy won't recover until some sector other than real estate creates new jobs. Once some other sector creates jobs, new households will form which will in turn create demand for real estate. With fresh demand for real estate, housing employment will start to recover, and the demand will snowball from there. The catalyst will not be housing. It must start in another sector of the economy.

.png)

.jpg)

This contention is just wrong. Falling house prices will stimulate the recovery as it will put more money into the hands of consumers. We don't need another debt-fueled Ponzi scheme to save the economy. If we just let prices fall to their natural bottom and allow borrowers to borrow less, the extra disposable income will create the recovery we want to see.

This contention is just wrong. Falling house prices will stimulate the recovery as it will put more money into the hands of consumers. We don't need another debt-fueled Ponzi scheme to save the economy. If we just let prices fall to their natural bottom and allow borrowers to borrow less, the extra disposable income will create the recovery we want to see.

So every loan owner with no assets will immediately sign up for this program because they had nothing to lose anyway. Plus every borrower in a state like Nevada, where all loans are recourse anyway, would also sign up immediately. And would this agreement supersede state laws to the contrary? In Nevada recourse loans are extinguished after nine months if the lender doesn't try to collect. And does anyone believe the government would actually go after delinquent borrowers, or would they merely forgive the debt themselves in the end?

So every loan owner with no assets will immediately sign up for this program because they had nothing to lose anyway. Plus every borrower in a state like Nevada, where all loans are recourse anyway, would also sign up immediately. And would this agreement supersede state laws to the contrary? In Nevada recourse loans are extinguished after nine months if the lender doesn't try to collect. And does anyone believe the government would actually go after delinquent borrowers, or would they merely forgive the debt themselves in the end?