We are preparing for some exciting upgrades here at the IHB. Today, I'll talk about some of these changes and why we are making them.

Irvine Home Address … 51 STOWE Irvine, CA 92620

Resale Home Price …… $949,900

Here I am, on the road again

There I am, on the stage

Here I go, playing star again

There I go, turn the page

Bob Seger — Turn The Page

Life is always moving forward. It's time for us to turn the page and embark on a new era at the IHB. But first, a look at one of the reasons we are looking to enhance the IHB experience.

Flawed housing data might mask depth of woes

Critics say Realtors' monthly report overly optimistic

By John W. Schoen Senior producer — March 25, 2011

Two high-profile reports on home sales this week confirmed that the housing market is still mired in a deep slump with prices still falling and sales activity sluggish at best. In fact, the market may be in much worse shape than even those numbers suggest.

Figures from the National Association of Realtors that are among the most closely watched indicators on the housing market have been called into question by economists who say they may overstate existing-home sales activity by up to 20 percent.

The issue is more than just an academic dispute among economists. Without a working barometer, it's hard to see the next storm coming.

It's time to take this task away from the NAr and create some bloated and inefficient government bureaucracy to collect and disseminate this data instead. I would rather deal with the problems of government waste than realtor duplicity.

“It's very important for the industry but also for policy makers,” said Mike Fratantoni, head of research at the Mortgage Bankers Association, one of the groups that is challenging the Realtors' data.

“Folks at the Fed and at the Treasury and anyone involved in economic policy throughout government are very concerned about the health of the housing market. So if your primary indicator is giving you an overly optimistic reading, that's cause for concern,” he said.

It's only a concern for those interested in the truth. Accuracy is not as important to realtors as creating a false sense of urgency.

The Realtors, a trade group of licensed real estate agents and brokers, concede that there has probably been some “upward drift” in its numbers since the unprecedented collapse of the housing market in 2006. But Realtors spokesman Walter Molony says the group's data still accurately track the monthly ups and downs of home sales, providing valuable insight into sales trends.

“In terms of broad market characterizations, it's really not that big of a deal,” said Molony.

Not that big a deal? They grossly overstate housing sales numbers to manipulate buyers for purely self-serving reasons, and this is not big deal? I'm sure it's not… to them.

But if the data is as badly flawed as critics fear, it could be a big deal for home buyers and sellers because it could mean prices are more likely to head even lower. That's because an unrealistically optimistic assessment of the pace of home sales could be artificially buoying home prices.

The possible breakdown of the barometer couldn't come at a worse time for the housing industry. After signs of life last year — helped by generous government tax breaks—there are ominous signs that those incentives simply pulled future sales forward.

According to the Realtors, sales of existing homes fell nearly 10 percent last month, snapping three months of gains. Sales of new homes, which are tracked by the government, plunged in February for a third straight month to the lowest level in records dating back nearly 50 years.

Analysts have theorized that new-home sales have been hurt because prices of existing homes have fallen more quickly, making them relative bargains. But analysts have been unsettled by data suggesting that the housing market is headed into another leg down for sales and prices.

“This is really unknown territory for us,” said Evan Barrington, head of economic analysis at The Stephenson Company, a market research firm. “We haven’t been through this before.”

'Upward drift'

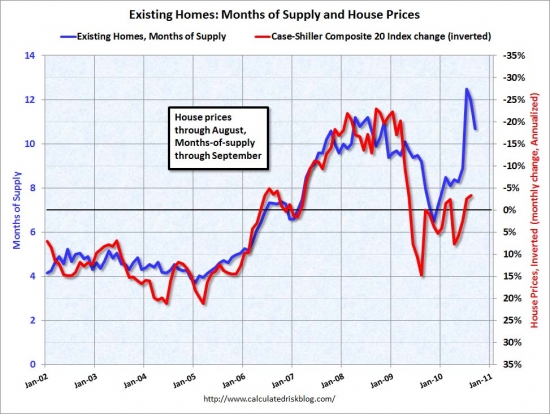

One reason for concern about the Realtors' data is that when assessing the outlook for future sales, forecasters rely heavily on the inventory of homes on the market, which is generally expressed in number of “months' supply.”

That number is derived by comparing the number of unsold homes and the current pace of sales. Prices tend to be fairly stable when the market has about six to eight months' worth of unsold homes. Tighter supplies tend to push prices higher, bigger supplies tend to depress prices.

According to the NAR's latest monthly data, the number of unsold homes in February represents an 8.6-month supply at the current sales pace, based on an annual sales rate of 4.88 million.

But other measures — including mortgage data tracked by the mortgage bankers, show a much lower sales pace. Private research firm CoreLogic, which counts closings filed in more than 2,000 counties, says the pace of home sales in February was just 3.6 million units on an annual basis. If true, that means the inventory of unsold houses is more like 17 months' supply, or roughly double the level reported by the NAR, according to Mark Fleming, chief economist at CoreLogic.

“(Overstating the pace of homes sales) makes a big difference in terms of that month's supply measure,” said Fleming. “That implies significant downward price pressure — which we're actually observing. Prices are falling month over month — and year over year again — at a pretty significant pace at the moment.

So what could account for such a substantial overcounting of home sales?

The desire to lie. realtors feel the need to puff the market with bogus statistics. The rest is merely the mechanics of the deception.

To begin with, monthly statistics like home sales data are the murky underpinnings of economics – a prime example of why it's called the “dismal science.” Almost all economic statistics — from widely watched employment data to more obscure measures of industrial output – are only estimates based on data samples that are designed to stand in for a more complete reporting that would take months or years.

In the case of NAR's existing home sales report, the association polls about 40 percent of its members and logs sales based on the widely used Multiple Listing Service. Up until 2010, it periodically “benchmarked” its data based on the more complete count conducted by the U.S. Census.

Unfortunately, the Census dropped several key questions about housing in the 2010 Census, which left the NAR without that data set to recalibrate its own data series.

“That kind of threw a monkey wrench in the works for us,” said Molony.

The collapse of the housing industry may also have played a role, according to housing economists who are talking a closer look at the data. One theory is that the consolidation of the housing industry also brought a consolidation among real estate agencies that the NAR's model hasn't kept up with. An agency used in the NARs sample, for example, may have increased sales because it acquired smaller agencies, not because sales in that market rose.

Offering excuses only hides the reality that the NAr knew their methods would inflate the numbers, and they chose to deceive the American people because the numbers were not what they wanted them to be.

Moloney said the NAR is working with the Federal Reserve, Fannie Mae, the Federal Housing Finance Agency, the MBA, Corelogic and academic economists to get its monthly sales data back on track.

“It's a normal process, but now we have to obtain a consensus with a lot of parties,” he said.

That could be a big challenge, given the number of businesses that keep an close eye on the NAR data.

The housing industry's outsized role in the U.S. economy touches thousands of businesses whose sales rely heavily on the level of home sales. From appliance makers to home improvement centers, businesses have to decide month-to-month how many workers to hire and how much inventory to stock. The NAR's monthly number is one of the most critical pieces of data they rely on to make the right decision.

“These data really do have a real world impact,” said Franatoni.

Data is important, isn't it?

It's a shame the NAr has gone down the path it has. Few reliable sources of real estate analysis and information exist, and few signs the NAr is going to become one of them. That leaves a void. Uncharted waters buyers must navigate without a reliable guide. It's a void we seek to fill here at the IHB.

We are in the process of assembling our own private database of housing and related economic statistics. Over the next several weeks as I have time to digest the new information, I plan on a number of new analysis posts to truly illuminate the activity in our local housing market.

I have no agenda to spin the data. Let's see what is really going on. I want to be accurate. People can make their own decisions and draw their own conclusions from accurate data. If approached without the built-in bias of a realtor, data analysis can be revealing rather than deceiving.

I will still have a dog in this hunt. I do run a business that makes money from real estate transactions. I am subject to the same biases as any other human being. I sell real estate, but I am not a realtor. The truth needs no salesman. I will present data as accurately as I can. If reality motivates you to buy or rent, the IHB can help you. I have no desire to manipulate data in order to make a quick buck. This is a part-time hobby for me, not my livelihood.

What about the OC Register?

I recently gave the OC Register grief because The OC Register Says California had no real estate bubble. It's a legitimate beef when a supposedly impartial newspaper starts permitting realtors to revise history with self-serving bullshit.

I probably would have overlooked that silly article in the past. I was once on the cover of the OC Register. I think much of their reporting is very good, particularly Marilyn Kalfus who I think does outstanding work.

Did you see their recent blogger anniversary series?

- Blogger: Home prices could dip extra 10%

- Blogger: Home-price gains years away

- Blogger sees 5 more years of housing decline

- Blogs keep real estate media honest

I wasn't noteworthy enough to make their list. ~~ sniffle, sniffle ~~ Perhaps they forgot about me? Their readers haven't. Note September 2010 when IHB stood atop the list.

I don't know how compete.com does their traffic counts, so I can't comment on the accuracy of their data.

How is the IHB unique?

When I started writing for the IHB in February of 2007, I had a simple message: don't buy, prices are going to crash. It was an important news story to a population gripped with the insanity of a financial mania. The message stood out, and the blog readership quickly grew.

I put a great deal of time and effort into writing a series of analysis posts which became the basis for my book, The Great Housing Bubble. It was my the equivalent of a doctoral thesis in real estate economics. My credibility on real estate is evidenced by the book, the daily writing here, and the fact that I predicted a market decline, and explained why it was going to happen. I could have been lucky.

in order to stay relevant and change with the times, I need to provide you a compelling reason to come back. I hope you enjoy my writing and my cartoons, but coming back for a good laugh isn't all I have to contribute. With this new data, I can provide a unique view into the workings of our local housing market.

Data analysis is core strength

I have some skill in data analysis, and with the collective wisdom of the blog that shines through the astute observations, we will come up with some compelling ways to look at data. Many of the silly arguments that dust up in the comments can be put to rest with data.

For instance, are heavy-cash buyers supporting house prices in Irvine? With data, we can answer this question. I am getting the median home price and the median loan amount history back to 1988. We will be able to trace exactly how down payments have fluctuated over time. We can correlate changes in the down payment with changes in price. If down payments go up when prices go down, then heavy cash buyers are indeed keeping prices up.

I have no idea what the truth is. I haven't looked at the data. This tempest in a teapot has been whirling in the comments for months. Wouldn't it be great to know the truth?

How many homes did the Irvine Company really sell?

Do you remember the recent news article where the Irvine Company claimed they sold 1,200 homes? Well, they didn't actually sell that many homes, they “signed 1,234 buyers” whatever that means. According to DataQuick, there were 643 new homes sold in Irvine in 2010.

The blue line above is the raw data, and the red line is the trailing twelve months as a moving average. The smoothing effect of the moving average reveals the underlying trends in new home sales.

I didn't realize they sold so few new homes after the 2001 recession. The bubble rally years of 2002-2004 were not as lucrative for new home sales as I would have thought. It looks like late 2004 through 2005 was a very profitable period for them. They sold a lot of houses at peak prices. From July 2004 to December 2006, they sold 2,455 homes.

The utter collapse of sales in 2008 is apparent. After recording two sales in January of 2009, there were zero sales in February and March of that year. In all of 2009, there were 90 new homes sold in Irvine. The average since 1988 is 52.5 homes per month.

The good news is that the trend is decidedly up. It's hard to go below zero.

What data is coming?

That is probably a follow-up post all to itself. I am getting data down to the zip code level for most items. For the MLS data, we are grouping builder codes into neighborhoods to overcome the clumsy village codes in the local MLS. Knowing the median price in Northwood is not as useful as seeing the difference between Northwood Pointe, Northwood I and Northwood II. Granularity of data is important for it to be meaningful.

I have closed sales, asking prices, rents, sizes, ages, and a number of other data points all broken down by zip code, village, and neighborhood. We will be able to identify high-equity neighborhoods and high-debt neighborhoods. We will be able to rank villages and neighborhoods desirability as measured by median and $/SF for both resales and rentals. Which do you think is more desirable, Turtle Rock or Turtle Ridge? The numbers will tell us.

Where is the data coming from?

I am getting data from three sources:

- MLS listings and transactions raw data

- Dataquick

- Various public sources

No NAr nonsense data or projections. I am using raw MLS data which is subject to its own errors. The information I am getting from Dataquick is one level removed from the raw data, but Dataquick's reputation for accuracy is good, certainly better than the NAr.

I also discovered a great source of public data at the St Louis Fed. They call the system FRED for Federal Reserve Economic Data. They go to the various government agencies, compile their data, and put it in a consistent format so data analysts like me can use it. If you are in to data, this site is a treasure.

How will Shevy get involved?

I didn't handle the announcement of the brokerage well. I thought the shock value would be interesting and positive. I was wrong. Unfortunately, that put Shevy in a difficult circumstance to share is perspective on the market. We are going to change that.

Shevy has been working daily with IHB clients since 2009. Our sidebar has testimonials from IHB clients on the quality of his work, and his sales volumes have been fantastic. In other words, he has satisfied a lot of IHB clients.

We have asked Shevy to start writing posts we will air on Sundays. He may not write every Sunday, but he will share his experiences working with clients. It's a perspective on the market I don't have.

Do you like the Shevy graphic? I was inspired by the common interpretation of Raphael's The School of Athens: “It is popularly thought that their gestures indicate central aspects of their philosophies, Plato's his Theory of Forms, Aristotle's his empiricist views, with an emphasis on concrete particulars.”

i believe Shevy will contribute much to the IHB conversation.

That Mille Fleurs you're waiting for has a squatter in it

The myth of Irvine's high end immunity continues to prove wrong. The reality of squatting to boost prices is inescapable.

Today's featured property isn't supposed to exist. All the heavy-cash buyers with stable finances are allegedly holding all of Irvine's prime properties. Apparently, there are still a few posers out there.

This property was purchased on 5/3/2005 for $1,247,000. The owners used a $935,200 first mortgage, a $186,750 second mortgage, and a $125,050 down payment. I thought this would be a tale of woe from a peak buyer. Nope. These owners got some HELOC booty.

On 2/6/2007 they refinanced with a $1,218,750 first mortgage and a $225,000 HELOC. The total property debt is $1,473,750, and they managed to extract $351,800 — unless you don't believe they maxed out the HELOC. In that case, they only got out $96,800, which recoups most of their down payment.

They quit paying about two years ago.

Foreclosure Record

Recording Date: 02/11/2011

Document Type: Notice of Sale

Foreclosure Record

Recording Date: 12/18/2009

Document Type: Notice of Sale

Foreclosure Record

Recording Date: 09/17/2009

Document Type: Notice of Default

Foreclosure Record

Recording Date: 09/17/2009

Document Type: Notice of Rescission

Foreclosure Record

Recording Date: 07/07/2009

Document Type: Notice of Default

During the next recession, if I fall on hard times, I hope I am allowed to squat in a Mille Fleurs. As for the buyer waiting to pay for the house, too bad.

Irvine House Address … 51 STOWE Irvine, CA 92620 ![]()

Resale House Price …… $949,900

House Purchase Price … $1,247,000

House Purchase Date …. 5/3/2005

Net Gain (Loss) ………. ($354,094)

Percent Change ………. -28.4%

Annual Appreciation … -4.5%

Cost of House Ownership

————————————————-

$949,900 ………. Asking Price

$189,980 ………. 20% Down Conventional

4.79% …………… Mortgage Interest Rate

$759,920 ………. 30-Year Mortgage

$192,011 ………. Income Requirement

$3,982 ………. Monthly Mortgage Payment

$823 ………. Property Tax

$450 ………. Special Taxes and Levies (Mello Roos)

$237 ………. Homeowners Insurance

$105 ………. Homeowners Association Fees

============================================

$5,598 ………. Monthly Cash Outlays

-$964 ………. Tax Savings (% of Interest and Property Tax)

-$949 ………. Equity Hidden in Payment

$347 ………. Lost Income to Down Payment (net of taxes)

$119 ………. Maintenance and Replacement Reserves

============================================

$4,151 ………. Monthly Cost of Ownership

Cash Acquisition Demands

——————————————————————————

$9,499 ………. Furnishing and Move In @1%

$9,499 ………. Closing Costs @1%

$7,599 ………… Interest Points @1% of Loan

$189,980 ………. Down Payment

============================================

$216,577 ………. Total Cash Costs

$63,600 ………… Emergency Cash Reserves

============================================

$280,177 ………. Total Savings Needed

Property Details for 51 STOWE Irvine, CA 92620

——————————————————————————

Beds: 5

Baths: 3

Sq. Ft.: 3650

$260/SF

Lot Size: 5,339 Sq. Ft.

Property Type: Residential, Single Family

Style: Two Level, Contemporary

Year Built: 2005

Community: Woodbury

County: Orange

MLS#: P775061

Source: SoCalMLS

Status: Active

On Redfin: 1 day

——————————————————————————

New Listing (24 hours)

This elegant Mediterranean style 5bd 4bth home is located in the prestigious Woodbury Community in Irvine near 405 & 5 fwys. Mille Fleurs Plan 1 (Giverny) built by Standard Pacific homes offers plenty of upgrades that include ADT alarm system, corian countertops, built-in BBQ & fireplace, Koi pond, and many more ammenities. Truly resort style living. Hurry, wont last!!!

Breaking News!!!

Do you remember my Wii Golf hobby? I just broke the course record on the back nine.

That's going to be tough to beat….

What’s interesting is how bad the early 90’s were. It looks like late 93 was as bad as early 2009. The sub-25 home/mo period stretched from mid 1990 to mid 1994, longer than the current down period. Talking to a builder, he mentioned (for our area in NC) that this downturn in building would not be as bad as the early 90’s. It somewhat seems like, at least in Irvine, he might be right.

What happened to the column earlier this week about real estate brokers?

Did you have to pull it due to copyright issues?

Yes, I emailed Dr. White the post, and he asked me to take it down as it is about to be published in a major journal. I thought it already was published when I wrote the post. I wanted to help him out, not cause him grief, so I took it down when he asked.

Thanks for the explanation. I thought I was going mad and dreamed the whole thing. Alternatively, it would have reinforced my paranoia about the dark powers of realtors. What they don’t like, they simply make disappear…

I like your data approach… I work in govt contracting and we handle contract/supply chain/payment data for DLA and it’s very compelling what data tells you in terms of processes, perception, and the ability to save govt money and get manufacturers paid ontime with accurate data flow… real estate seems to be a great arena for that data consolidation and publication… the results will be fascinating I’m sure…

This article says that many desperate homeowners in Las Vegas try to rent their vacant properties much cheaper than it costs to own them. It contradicts your facts.

http://www.8newsnow.com/story/5558987/new-ghost-towns-sprout-up-in-las-vegas

…one thing that’s added to this trend is the buyer’s mentality.

“They’re not buying. They’re sitting on the sidelines. These investors that own all these vacant properties they can’t sell are turning to rental markets. So they’re renting them out at actual rents that are much less than what these people would pay if they were owning them.”

It’s true for Irvine too. Many homeowners who have bought recently lose at least $1,000 when they rent.

I think that Las Vegas article is old. The post has no date, but it did have this statement: “In September, the median price for a home was $285,000. That’s exactly the same as it was one year ago.”

The median in Las Vegas is around $115,000, and it has been in decline since 2007. I think the article must have been written in 2007. Everything stated in that article was true in 2007, but not today.

“They’re not buying. They’re sitting on the sidelines. These investors that own all these vacant properties they can’t sell are turning to rental markets. So they’re renting them out at actual rents that are much less than what these people would pay if they were owning them.”

Dang, and this quote is coming from a ‘r’ealtor. Imagine that. No bubble quote whatsoever.

Did anyone see this article in the NY Times?

http://www.nytimes.com/2011/03/26/business/26nocera.html?_r=1&ref=business

Thank you. That will be a post next week.

Just looked at this over at necked capitalism:

http://www.nakedcapitalism.com/2011/03/paul-jacksons-follow-the-money-shows-housing-wire-deep-financial-ties-to-mortgage-market-bad-actors.html

It reads like a petty hit piece to me.

But wasn’t Paul Jackson petty in the first instance? NC’s point is that Housing Wire has no moral high ground from which to complain about. Furthermore, lawyers, from a professional ethics point of view, are required to zealously advocate for their clients, including, at times, finding ways to finance litigation (heck, our whole system of tort-law is based on contingency-based lawyer fees). Journalists on the other hand, based on best practices (reality tends to undermine best practices) are supposed to avoid conflicts of interest and at the very least identify them. I hardly see why pointing out all the reasons why Jackson and Housing Wire can never claim to be objective sources of news is “petty.”

There is nothing wrong with pointing out conflicts of interest. I made a point of disclosing mine.

I was merely pointing out that the writing was personal, and it’s tone was that of a hit piece. There are other ways the author could have pointed out the conflicts of interest without the innuendos and disparagements.

Irvine Renter,

I don’t view the Housing Wire Blog so will depend on your evaluation. Does it spin real estate news any worse or better than what you see in the blogs you frequent?

We are also NV rental property owners – Reno in our case. We own outright so we don’t depend on cashflow to pay a mortgage. So far so good as the rental returns are much better than what we were getting from our investments.

I also have rented my old residence in Silicon Valley for the last 15 years. Total returns have more than compensated me for the total nominal cost of the property plus I had a place to raise my family.

I always knew that the California Property Pyramid was the way to real wealth but never had the cash to play and too many responsibilities to be risky. Only late in life has it become possible. Thank goodness, even if the properties crash and burn we will be OK.

Thanks for the blog efforts and good luck with LV.

I read housing wire nearly every day. I haven’t noticed an agenda to spin information to benefit advertisers or industry insiders. In fact, Paul Jackson has been nearly as critical as I have about the practices that led to the housing bubble.

It sounds like you have done well with your property investments. The virtue of paying them off rather than Ponzi borrowing is apparent every month you cash those rent checks.

Sounds like a data bomb may soon be dropped on planet realty and bull entourage.

We have a myriad of subsidy and still the numbers need massaging.

Small thing… though colloquial usage varies and there is some uncertainty, I believe data are plural. So I think the post should read, “Where are the data coming from?”