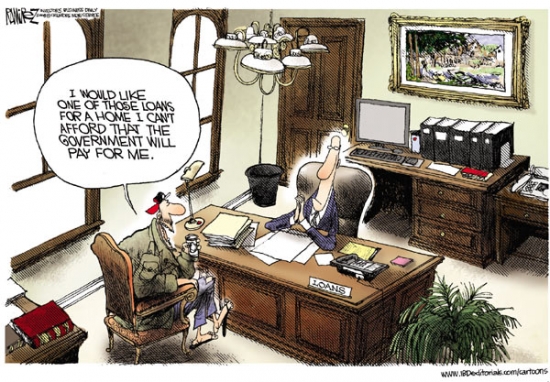

The limit on the size of the loan the GSEs will insure falls from $729,750 to $625,500 on October 1, 2011. The increased mortgage costs coupled with large inventories will lower house prices in that range and above.

Irvine Home Address … 9 SHADE TREE Irvine, CA 92603

Resale Home Price …… $987,000

Oh my God

Becky, look at her butt

It is so big

I mean her butt

It's just so big

Sir Mix-A-Lot — I Like Big Butts

Irvine borrowers like big loans, perhaps not with the same zeal as Sir Mix-A-Lot likes big butts, but borrowers here do like big loans. The cost of those loans is going up. This should be good news for squatters. If the banks are willing to wait until prices come back, delinquent mortgage squatters should get several more years of free housing.

Home buyers try to beat “jumbo” loans squeeze

By Linda Stern — WASHINGTON — Wed Apr 20, 2011 5:52pm EDT

(Reuters) – Bethany and Karl Schreiber are hunting for a nice big house in the pricey Washington, D.C., suburbs and they are facing a deadline: In just a few months their third child will be born, and the tiny two-bedroom they've been inhabiting will officially get too small.

So the story begins with a sympathetic couple who's burgeoning entitlements demand larger housing, reality be damned.

But there's a second deadline looming for them as well. Beginning on October 1, the government will dial back on the size of mortgages it guarantees in high-cost areas like San Francisco, New York and Washington.

After that, the maximum loan amount that Fannie Mae and Freddie Mac will back is scheduled to drop from $729,750 to $625,500. And that may make mortgages more expensive or harder to get for buyers like the Schreibers, who are shopping in the $700,000 range and would prefer to make a downpayment of 10 percent or less.

And Irvine. This change strikes at the heart of the Irvine single-family detached market. Many Irvine properties have loans between $729,750 and $625,500. Every buyer contemplating a loan in that range will face an interest rate half a percent higher. As a result, buyers will either need to come up with 10% more income to afford the same mortgage, or the loan they will qualify for will be 10% smaller. Since most Irvine borrowers are maxed out, loan balances in this price range will likely decline by 10%, and the houses they were intended to finance will similarly drop in price.

A lower conforming loan limit will seriously erode the upper-middle tier of the Irvine market. The already precarious high end will see continued pricing pressure as lenders continue to deflate loan balances.

“If we wait a year, we may not be able to afford as big a house,” Bethany said in an interview. “Rates and housing prices are probably going to go up.”

Either these people have been brainwashed by their realtor, or they don't understand the problems with supply which are more likely to see motivated sellers pushing prices down. In the long run, house prices will go up, but it may be a while.

The Schreibers concede their timing is mainly inspired by their own family circumstances. But others may be motivated to act now because of reduced government-backed loan assistance, housing experts say. Those programs were put in force as part of the stimulus package after the housing collapse.

“For people planning on exiting the market altogether (such as retirees), that is a compelling proposition,” says Stan Humphries, chief economist at Zillow. Home sellers may have to be patient to get the price they want. The curbs on government-backed loans could, at the margin, reduce the available pool of buyers, he said.

With prices going down, sellers will have to be patient, very patient. Many accepted facts of real estate become untrue when prices decline.

MILLION-DOLLAR DWELLINGS

Anybody who wants a government-backed mortgage for a $1-million home after October 1 may have to come up with a $370,000 downpayment instead of $270,000, says Rob Chrisman, an independent mortgage banking consultant from San Rafael, California.

It won't be quite that dramatic, but the already strained down payment levels on high end properties may get stretched once again. Sales volumes will fall from their already anemic levels.

The deadline will mean most to upper-middle-class buyers and sellers in costly real estate markets where $1 million buys a nice house, but not a mansion.

To be sure, that part of the market is picking up. Real estate agents operating in tonier neighborhoods are reporting brisker business this spring than in recent years.

Bullshit. Every word of those last two sentences was spin and bullshit. SoCal March home sales plummet 5.2% YOY, now 21.4% below average.

Sotheby's, which specializes in luxury homes, reports sales making double-digit gains for the first quarter of this year over last year. The National Association of Realtors reported that the sale of homes over $1 million were up 5.1 percent in March over the same month last year.

More spin and bullshit.

“We are seeing a normal recovery,” said Jed Smith, managing director of quantitative research. “I'm sure somebody will accelerate their activity (because of the expected drop in government-backed loan limits), but I doubt you'll see a lot of acceleration because of that.”

“That really isn't on anybody's radar,” agreed Linda Chaletzky, the Schreiber's agent, and a specialist on Washington's tonier suburbs. “But things are hopping.”

She said she is not worried about the loan clampdown,

“The mortgage industry will find a way around it, because they will have to. If they don't, they will go out of business,” Chaletzky said. She expects private mortgage lenders to step in and fill that space when the government backs down.

The level of ignorance among industry professionals is truly astounding. Financial innovation is an oxymoron. The industry doesn't have to find a way around anything. Underwriting stable 30-year fixed-rate mortgages can supply all the money the housing market needs to provide everyone who can afford to own the opportunity.

What puts mortgage lenders out of business is underwriting stupid loans to people who can't or won't pay them back. Unfortunately, that is usually the result of financial innovation. That plus a large government bailout.

BIG MORTGAGES

It was only in recent years that the loan limits went so high. Mortgages that are too big to be sold to Fannie and Freddie are termed jumbo loans and are backed privately. Until 2008, all home loans over $418,000 were considered jumbo loans. In that year, a stimulus-focused Congress twice raised the limit on loans the government would back in high cost areas, first to $625,500 permanently, and then to $729,750, temporarily.

Since then, Fannie and Freddie have backed an increasing share of that market. In 2010, so-called “jumbo conforming” loans, those over $417,000 and government-backed, made up 6.73 percent of loan originations, according to CoreLogic.

That top temporary limit was extended twice, but is expected to expire at the end of September.

It's an outrage this limit was ever extended above $417,000. Private lending market made incredibly irresponsible jumbo loans, and in order to bail out the banks, we needed to increase this limit to have the federal government guarantee the loans underwritten during the decline. It was the only way to shift much of the losses from private industry to the public sector.

When that happens, lenders who want to make loans over $625,500 will have to hold onto the mortgage themselves or find private investors to buy them. And while an active and hungry secondary market for these jumbo loans has yet to materialize in the post-crash world, there's some evidence that lenders are preparing to move into that space and pick up any slack that the government leaves.

“There's plenty of money out there,” said Steve Hopps, chairman of the California Mortgage Bankers Association.

Private lenders are preparing to step in, according to Guy Cecala of Inside Mortgage Finance, a research firm. In the last quarter of 2010, private lenders originated more loans over $417,000 (the traditional jumbo market) than did government agencies, he said.

Nice spin. He has compared apples to oranges and made the situation sound better. The fact is that government backing on loans over $417,000 is limited to a few high-price areas like Irvine, and it is capped at $729,750. The everything else market should be larger, much larger.

The lower loan limits will leave about $10 billion more in loans for private lenders to handle, reckons Cecala, and he expects lenders to go after the market aggressively.

Lenders are eager to throw away more money to support a declining market, right? Give me a break.

BIGGER DOWN PAYMENTS

Investors like the fact that jumbo loans tend to be safer and more profitable than smaller ones. The privately-backed mortgages require bigger downpayments (currently about 30 percent of the home's value, instead of the 20 percent more typical in less expensive loans), which adds security.

Also adding to their allure, the loans carry higher interest payments; the spread between the so-called conforming loans backed by Freddie and Fannie and jumbo loans is running about 0.5 percentage points higher, said Cecala. Furthermore, a higher proportion of jumbo loans are made on a variable rate basis, which is less of burden for holders, Cecala said.

Going still higher in the homes market, there will be less impact from the shrinking jumbo. Many buyers of multi-million dollar homes do all-cash deals and are relying on cash more than ever before, according to Stan Smith, a real estate agent who works in Beverly Hills area.

The biggest impact might be limited to that space and those neighborhoods occupied by people like the Schreibers — folks who see themselves as middle class but in very expensive areas.

“I see borrowers, if they want that kind of loan, paying a little more,” says Chrisman. “But it's not going to be a life changing event for a couple of orthopedic surgeons in Beverly Hills.”

(Reporting by Linda Stern; Editing by Richard Satran)

If the entire housing market were composed of orthopedic surgeons, then local house prices might not fall. Since that isn't the case, the upper-middle-class borrower is going to be impacted by the increased costs, loan balances will go down, and prices will go down with them. This fall and winter should see the end of any spring rally and another leg down in pricing for above-median properties.

It was a bear rally, not the bottom

Apparently, the owner of today's featured property did not see the recent post on the IHB demonstrating the double-dip in local home prices. This owner believes the resale value of this house has appreciated 15% while the market has gone down.

It delusional enough when sellers price their underwater properties at breakeven, but this owner actually believes profits are available. Recent comps paint a different picture.

|

$775,000

Sold on Apr 14, 2011 |

0.1 miles

2 bd / 2 ba 2,000 Sq. Ft. |

Each seller usually tries to indulge their fantasies of what their house is worth.The ones that sell their properties are the ones who abandon their dreams and take what the market will bear. The rest hold their properties forever waiting for the profit they are entitled to.

Irvine House Address … 9 SHADE TREE Irvine, CA 92603 ![]()

Resale House Price …… $987,000

House Purchase Price … $850,000

House Purchase Date …. 8/28/2009

Net Gain (Loss) ………. $77,780

Percent Change ………. 9.2%

Annual Appreciation … 9.0%

Cost of House Ownership

————————————————-

$987,000 ………. Asking Price

$197,400 ………. 20% Down Conventional

4.78% …………… Mortgage Interest Rate

$789,600 ………. 30-Year Mortgage

$177,138 ………. Income Requirement

$4,133 ………. Monthly Mortgage Payment

$855 ………. Property Tax (@1.04%)

$300 ………. Special Taxes and Levies (Mello Roos)

$206 ………. Homeowners Insurance (@ 0.25%)

$0 ………. Private Mortgage Insurance

$248 ………. Homeowners Association Fees

============================================

$5,742 ………. Monthly Cash Outlays

-$1000 ………. Tax Savings (% of Interest and Property Tax)

-$988 ………. Equity Hidden in Payment (Amortization)

$360 ………. Lost Income to Down Payment (net of taxes)

$143 ………. Maintenance and Replacement Reserves

============================================

$4,257 ………. Monthly Cost of Ownership

Cash Acquisition Demands

——————————————————————————

$9,870 ………. Furnishing and Move In @1%

$9,870 ………. Closing Costs @1%

$7,896 ………… Interest Points @1% of Loan

$197,400 ………. Down Payment

============================================

$225,036 ………. Total Cash Costs

$65,200 ………… Emergency Cash Reserves

============================================

$290,236 ………. Total Savings Needed

Property Details for 9 SHADE TREE Irvine, CA 92603

——————————————————————————

Beds: 2

Baths: 2

Sq. Ft.: 2330

$424/SF

Property Type: Residential, Condominium

Style: Two Level, Mediterranean

View: Mountain

Year Built: 2003

Community: Turtle Ridge

County: Orange

MLS#: U11001594

Source: SoCalMLS

Status: Active

——————————————————————————

Gorgeous 2 bedroom, plus den in beautiful gated community of Canyon s Edge in Turtle Ridge. This premium location is surrounded by rolling hills. This totally detached home is beautifully upgraded with custom cabinetry, dark wood flooring, and large marble kitchen. Den can be a 3rd bedroom or 2nd master on ground floor. Formal dining room, family room with fireplace and master bedroom with retreat, walk in closet, large bathroom with huge tub. Very private and custom designed yard with built in BBQ with refrigerator. A Fabulous fireplace with a separate lounge area with fountain. This elegant home has wonderful trails. Just minutes to beach and easy access to 73 & 405. Built in 2003 with over 2330 sq. feet. Located within the Irvine Unified School District.

I’m sorry, but WTF???

Maybe it’s the angle of the photo, but that house looks incredibly ugly. It looks like two completely different styles stuck together. Are those two houses, with just a really weird photo angle, because each style actually might work on its own. But together, FAIL!

Also, again, maybe it’s a weird photo angle, but the part in the foreground looks like it’s leaning to the right. Was it designed this way? Basically, the whole thing looks designed by a very conservative architect who had a bad acid trip. Or rather two architects.

They want a million dollars for THIS??? Good luck with that.

Henry

What is the deal with the half stone half tinder box look? This is an actual design?

Oh, that is easy to explain. Since this is a two bedroom dwelling, then one bedroom resides in the stone part while the the other bedroom resides in the tinder box part of the “house”.

I think they are actually two different houses built right next to each other. The builders realized that they could shoehorn another Irvine tract house onto the lot if they did away with the traditional 5 feet between neighboring houses.

How about that warm stone look straight of The Shawshank Redemption?

They ran out of stone that day. They also ran out of windows for the kitchen.

“She expects private mortgage lenders to step in and fill that space when the government backs down.”

Yes, one private lender already has re-entered the true Jumbo Market (Astoria):

740 FICO, no cash-out, no investment/2nd homes, no condos. 30% down. Limited DTI. AND 20% reserves (after down). NOT 6 months PITI, 20%.

So to buy a million dollar home, one needs $300,000 down AND $200,000. That is a very narrow target of borrowers…

Congratulations on being one of many blowing this way out of proportion. I’ve only seen calculated risk accurately analyze this.

In Irvine the vast majority of houses are purchased with a loan 417 or less and a large down payment. Even most of the more expensive homes are purchased with less than 417k when a third have no loan at all. Even excluding all of those purchaes which probably represent greater than 90% of Irvine transactions…the minuscule higher rate is cushioned by the tax deduction… In this tax bracket that reduces a 0.5% rate increase to more like a 0.35% rate… And even then most have the capability to pony up more cash to the deal if it makes sense.

Since this has such a minimal impact, why don’t we go back to the pre-2008 level of $417,000? You don’t want your tax dollars going to waste on a subsidy that doesn’t impact the housing market, do you? After all, there is an endless supply of heavy cash buyers eagerly snapping up every Irvine home. Have you seen the stellar sales rates?

I’m fine with it going back to $417k.

This was mostly done to have you the tax payer pay for the bubble debt in government backed modifications. Now that poison pill was transferred to the tax payer there is no use for it.

The time to blow this out of proportion was 4 years ago, when the tax payer was bent over a barrel.

This will have almost no impact on the current Irvine market.

I’m not sure that it will have almost no impact, but I too don’t see a significant impact due to this change. Houses where this change might have impact on buyer decisions represent only about 10% of total houses on the market in Irvine. So if we extrapolate that about 65% of these represent 20% or less down buyers (and therefore would be impacted by the lower cap), we’re looking at about 6% of homes impacted. And then how many will actually curtail their decision because rate is .5% higher?

I can see some trickle down/up effect on other price points because of this, but again I think we’re looking at a fairly insignificant impact. It makes sense that the price may be driven down slightly due to this, barring any other factors. But I think other factors in economy will have much greater impact on Irvine home prices than this change.

I… must… stop… agreeing with PR…

Haven’t chimed in a while but I’m third with this notion… Absolutly go back to $417k conforming loans… The Goverment should absolutly not be in the business of backstopping high dollar homes for the upper middle class.

http://news.yahoo.com/s/ap/us_housing_battle#mwpphu-container

agreed loans will be much more difficult to get because the risk is greater for the banks/mortgage firms.

Especially if Freedie and Fannie go away.

The federal reserve has a site on credit conditions:

http://data.newyorkfed.org/creditconditionsmap/

You can go to jumbo loans in the mortgage section and it will tell #loans/1000 housing units. For the OC it is 87, or 8.7%. Rough measure.

The other option banks have is a first at $417k, and a second to get to 10-20% down. Sell the first to the GSE’s and hold the 2nd.

Don’t be surprised when the banks start doing this again in volume.

It will start with only stellar credit scores and high asset levels.

You should now how the story goes from there.

It will be more likely that the second will be repackaged then sold to the GSE. When the default comes, the GSE/taxpayer can take the total hit.

History proves that people never learn from history.

One thing has puzzle me: Being called a “Turtle” is a very big insult for ABC’s and OBC’s.

If that is the case then it would be bad. I thought it OK if the originator held a chunk in first loss position. Do you have any evidence that (repackaging the 2nd’s) is what is happening?

That’s the game plan for later.

Currently most are GSE backed loans on the first with low down. If the borrower has high down, the bank will use their own money on the first.

The repackaging of bad seconds will occur once the economy picks up and memory fades with time and new financial inovations (i.e., new Ponzi or loan modifications).

i suspect it will have a very noticeable impact.

everyone is analyzing it from a financial perspective.

no one is looking at it from a psychological point of view.

the $8k home buyer’s tax credit very significantly affected the more expensive homes (case shiller shows prices went up for all tiers). not because people buying the expensive homes were saving a huge amount but because in the frenzy of the $8k credit, everyone caught the fever and created an environment that made it seem like it was a great time to buy whether it was a $100k house or a $1M house.

similarly, i believe it’s possible that the lowering of the mortgage limit will make it harder for people to buy dampening an already depressed market. as the sales numbers drop more than usual, more people will become cautious, fewer people will want to buy.

Well put, *. I completely agree. The 8K credit is the reason that we SOLD our house. And there is no way I’m buying an $800+ house in Irvine after the loan limit announcement. Those things will go down $100K or so in the next year based on that impact alone. (Other government interventions nonwithstanding).

By Oct 1, in Irvine we will likely see $5 gas, higher food prices and no real income growth.

Somehow I just don’t see a stampede into the private mortgage market, irregardless of terms offered.

another factor…

private bank lending is back with a vengeance. Virtual no covenant business loans (literally no exam required, no reviewed statements, no monthly reporting required for multiple $M lines of credit) and leveraged buyout loans for PE firms all the rage again.

the competition for risk is back. They hopefully won’t as crazy but don’t fool yourself into thinking bank lending is at 2009 criteria for any kind of lending.

So scared, exactly.

Just like the first move up was done for the banks to create a market to unload bad loans on tax payers, this move down is for the banks to create a profitable market for banks.

so_scared, go apply for your million dollar credit line. Tell them you are starting up a new Hog Washing business. Let us know how it turns out.

Dave,

not hog washing exactly but that is exactly how it turned out…multiple banks competing..result was covenant light and more line than originally requested by $Ms.

Don’t tell me, you are going to post that you don’t believe it. or this case is somehow special. I guess.

It is what is. As for LBO, you can read for yourself on how buyout deals are getting financed. Of course, you don’t believe those either.

I’m serious. Washing Hogs for Dollar-Dollar Bills is a viable business. Get out there and make those banks compete to give you millions. Hurry while the idea is still original!

This type of free money for all is limited mostly to public companies. If you are a small private company, I doubt you will find the money so freely flowing.

I am working with small private companies to get commercial RE loans and it is no easy matter. Possible, but not easy.

I work with many SMBs and their credit lines are opening up. Not at same levels of 2005 but definitely easier to do business. These companies are in the tech industry.

Yeah baby …

cnn.com: Home prices in ‘double dip’

Prices will likely fall for awhile. Conditions will start to improve once the economic recovery gains traction and job growth improves

Here we go again – some wonk equating increasing house prices as an “improvement” who completely misses the point that house prices shall continue to fall until prices are inline with salaries. “Job Growth” means nothing if the only jobs for growth are in burger flipping. I think it is safe to say that 100K Mortgage Pimping jobs are not going to be nearly as abundant going forward.

As a renter, I see conditions improving daily as house prices continue to fall and look forward to future improvements as affordability returns.

The house in the picture seems highly impractical…to pay that kind of money for a TWO BEDROOM house seems outrageous.

It has “Turtle” in the name of the community. That’s at least a 20% premium bump in Irvine.

Will obviously does not have children and if he did, they would most likely be attending 9/10 Star Schools – preparing for their hard lives ahead all because dad would not pay whatever was required for a piece of Irvine California.

AZDave – I understand how ridiculous it is for people to say they leveraged themselves up for their children’s education but the current buyers in Irvine aren’t highly leveraged. They are bringing 40%+ down. Also, the premium between 9/10 school cities near Irvine and Irvine with its 10/10 schools is about 10-20%…its much greater premium when compared to neighborhoods with lower scored schools.

While I personally might choose to save $100K and pick a 9/10 area, I wont choose to save $400K and pick a 6 or 7 area. Am I wasting my money? Maybe but it is truly my money – I don’t need a loan to buy the house.

You comment a ton on this children part – what would you pay if any more for better schools?

Renters have access to the same schools.

An off topic question for astute observers:

Last year Gov Schwarzenneger vetoed sb1178 which would have extended non-recourse protection to refinanced mortgages which many people obtained for the lower interest rates. It’ been stated that the essence of this bill has been re-introduced this year as sb458. My reading of 458 is that it applies only to short sales and requires the written approval of the bank or note holder; I find nothing addressing refi deficiency protection.

Anyone have any info on this?

Those two Shade Tree properties sure show how Agents really have no idea how to price a tract home these days. 52 Shade Tree is a comp killer no matter if it was distressed or an equity sale.

As another side note, at a recent area Realtor preview meeting an Agent got up to pitch his new listing. Practically verbatim: “Come and see my new listing. Please hurry as it’s just now on the market and the seller want’s it sold, so much so that they may have a price reduction in place next week”. Hurry????

Anyhoo. If you want a preview of what the $625k conforming jumbo market will do to sales prices, look no further than Riverside/San Bernardino. The Max Conforming an FHA loan amount out there is $500k. If in Chino, drive 6 miles to Walnut and the max is $729,750. Most higher end home prices in the IE have stabilized in a price range close to what borrowers can finance with 20% down – $625,000. Anything higher than that and you’ve got to put much more cash down. Financing in areas like Indian Wells or Palm Springs is another animal with either cash sales or private jumbo financing with a 1/2 percent higher rate than standard conforming. Outside of this desert community, you cannot use these jumbo loans without a much higher down payment – 25 to 30% – simply due to zip code restrictions.

The OC market may run down that same pathway. Specialized jumbo financing for NPB/QH/TR etc with $625k only for areas outside of those zip codes.

My .02c

Soylent Green Is People.

Can anybody confirm the square footage of 52 Shade Tree? That is, the listing says it’s exactly 2,000 square feet and also says “Square Footage Source: Estimated”, both big red flags that state “Square footage number pulled out of my butt”. In reality, it could be 1,704 square feet or something, which would affect the comps significantly.

If it is a Canyon’s Edge Plan B, the floorplan says 2000sft.

The listing doesn’t say what model it is but the pictures match up with the floorplan too.

Well, if there is a floorplan that matches, then the number is probably accurate. It’s just when you build a house, it’s rare for the square footage to come out to a round number, IMHO.

I kinda like that if you want a super expensive house, you would need to put 25 to 30 down. It’s a luxury that people should pay out of pocket to obtain.

Las Vegas High End Approaching Capitulation. Rest of market partying like it’s 1999.

If you are a Vegas renter, your moment is at hand.

Yes, if you are still employed, it’s time to move to some place with a better future.

Hey PR –

Have you been to Mandalay Bay recently? It’s like freakin Christmas (Even on Wednesdays!) over there! So much for the “crash”.

Hopefully Wednesday nights are so good they will need to hire even more high school drop out hourly workers.

Yes! They could be just like that New Century Financial in Irvine then!

Or the typical crop of RE agents in Planet Realty!

Hey, I worked at New Century! I was in IT, I pushed the button that shut down retail lending. It was a fun crazy place to work. Too bad it was even more of a basket case then I imagined.

Ah, that’s more like it! I knew it couldn’t last!

You’ll have to explain why you think it would be a good idea for someone who IS gainfully employed in now-dirt cheap Vegas would be motivated to get out to somewhere with a “better future”, like… Detroit?

Steady income, houses at bargain, rental surplus to keep prices down… I don’t get it. Though I have to admit the restaurant prices are now astronomical! What happened to $3.99 Circus Circus buffet? Okay, now I’m dating myself…

That classic Medieval-Mediterranean-Cathedral-cum-Fortress style….beeeeaaauuuutiful!