The process of market capitulation requires the individual participants to realize their folly. Their pocketbooks are aching, and they ask themselves how long they should let it go on breaking, and finally they realize they were the fool.

As prices fall in the wake of the housing bubble, whatever equity wasn't spent through rampant HELOC abuse is being washed away by falling prices.

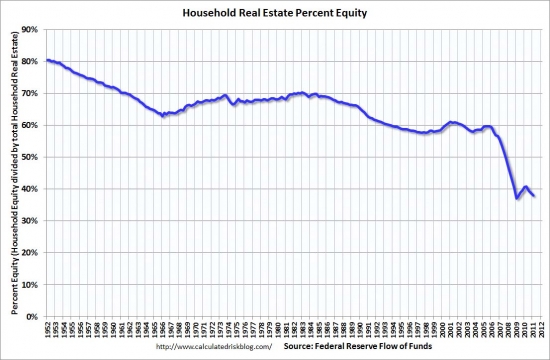

One data series that shocked me when I first saw it was the graph of home equity during the housing bubble. Everyone assumed home equity went orbital when house prices rose so far so fast. It would have except for one inconvenient truth: people were extracting that equity and spending it the moment it appeared. As a result, the expected huge increase in aggregate home equity from 2003 to 2006 never happened. Loan owners spent it all.

June 9, 2011 — The Associated Press, Bloomberg News

Falling home prices have shrunk the equity Americans have in their homes to nearly the lowest percentage since World War II.

Average home equity plunged from more than 61% at the start of 2001 to 38% in the January-March quarter this year, the Federal Reserve said in a report Thursday. That drop comes as home prices in big metro areas have reached their lowest level since 2002.

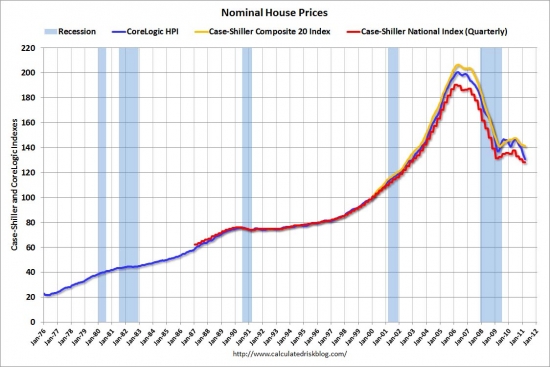

Prices fell 33% in 20 cities through March from their 2006 peak, reaching their lowest level since 2003, according to the Standard & Poor's/Case-Shiller index of U.S. home prices on May 31. The decline signaled a “double dip” as the index fell below its previous post-housing-bubble low set in April 2009. Prices more than doubled from 2000 to July 2006.

Further declines in home prices are likely.

Robert Shiller, the economist who co-founded the S&P/Case-Shiller index, said a further decline in property values of 10% to 25% in the next five years “wouldn't surprise me at all.”

“There's no precedent for this statistically, so no way to predict,” Shiller said Thursday at a Standard & Poor's conference in New York.

It's called overshooting to the downside, and it is very difficult to predict because the reasons it occurs is part mechanical and part psychological.

Mechanically, downside overshoot is caused by excess supply. With the millions of foreclosures lenders have already absorbed, and the millions more waiting in shadow inventory, housing markets everywhere have a huge supply problem. It has been masked over the last 3 years by withholding this inventory, but the problem didn't disappear, it's merely being held in abeyance to prevent a catastrophic price decline.

Psychologically, downside overshoot is caused by a change in buyer psychology. Since capturing appreciation was the primary reason people were buying during the bubble, and since prices are now depreciating, buyers who once were enthusiastic about real estate are shunning it like the plague. And they should.

Buyers need a new reason to buy, and and realtors calling the bottom is not sufficient. Only when prices are less expensive than competing rentals will buyers find a new motivation to buy real estate. And since rental parity is well below current pricing in markets like Irvine, buyers sit and wait, and sales volumes are anemic.

A backlog of foreclosures poised to hit the market means prices may stay depressed, dissuading builders from starting new construction.

The main reason for our ongoing economic doldrums is the lack of new residential construction. Housing is the economy. Nearly every recession since WWII has ended when residential investment picked up. Residential investment will not increase until the housing market has found a natural, sustainable bottom. The reason is simple: unemployed construction workers don't buy goods and services and stimulate the economy.

When the government tried to stimulate the housing market with tax credits and the federal reserve bought mortgage debt, their goal was to stimulate housing and jump start the economy. It failed.

The stimulants all failed because prices had not fallen to the point of affordability where real demand could sustain the momentum. It's like drinking coffee to stay up studying for an exam. You might get a temporary boost, but if the body is tired, it needs sleep, not stimulants. Similarly, if prices are inflated, temporary stimulants may cause prices to rise temporarily, but if what the market needs is a deeper price adjustment, that is what is eventually going to occur. And in fact, that is what's happening now.

How could someone tell if the market needed a deeper correction? On a macro level, measures of price-to-rent or price-to-income provide a clue. Plus, simply looking at long-term trendlines reveals prices are still too high.

On a micro level, rental parity is the best indicator. If prices are not affordable as measured by the cost of ownership compared to comparable rents, then prices need to come down. By both macro and micro measures prices are still too high in many markets.

Unemployment, which rose to 9.1% in May, and stricter lending conditions are signs that any recovery in housing may take years.

The CEO of Bank of America is telling people prices will go down. He is a good person to listen to because he will be one of the primary agents of the decline. Other than the GSEs, B of A has more REO than any other lender, and they are planning to liquidate. They won't dump the properties all at once, but they will liquidate, and their activity will push prices lower.

While it would be a surprise to see prices fall steeply, it's possible for homes to lose more value if inflation picks up, Karl Case, co-founder of the index, said Thursday.

“You could have flat nominal prices but still have it go down 20%,” Case said during an interview at the conference.

“If house prices stabilize, they could still go down in real terms. If we had inflation, it'd be great, because it'd mask a 25% decline.“

Did Karl Case just say inflation would be great because it would mask a 25% decline? A professional economist really said that? WTF? Does he really think it's a good thing for prices of everything else in our economy to rise significantly relative to housing is good because it keeps housing prices up? I'm starting to wonder who the real brains behind the Case-Shiller Indices is.

The Fed report showed that household debt fell in the January-March period at an annual rate of 2% from the previous quarter.

That drop was due entirely to a decline in mortgages.

Auto loans, student loans and other consumer credit rose 2.4% — the second-straight gain after nine consecutive declines.

We still have a long way to go to write down all the bad mortgages lenders are holding. Appreciation is not going to bail them out. The moment prices begin to rise, lenders will sell into the rising prices in order to liquidate their inventory. If both prices and volumes rise, lenders will quicken the pace of liquidations to stop the bleeding from their carrying costs. Any increases in lender selling will snuff out appreciation before it gains any momentum.

As long as lenders have copious amounts of houses and droves of delinquent mortgage squatters, house prices will not go up. Excess supply and carrying-cost pressures for liquidation will prevent price appreciation. Affordability will be excellent.

100% financing makes everything affordable

By far the dumbest idea that was fully executed during the housing bubble was embracing 100% financing. When lenders ran out of people with down payments and high credit scores, they took anyone off the street and gave them all the money to buy a house. With absolutely no barriers to entry to the housing market, everyone could afford to buy, and prices went straight up.

Of course, giving out the money is easy for lenders, but getting it back is more problematic, particularly when they loaned money to people under terms that nobody could meet.

What we are left with are properties like today's featured property. The owners paid $245,000 on 7/25/2002, and they obtained a $245,000 first mortgage. They put nothing down.

After a refinance for $225,600 and a stand-alone second for $24,000 on 6/5/2003, the owners went back to the housing ATM on 5/18/2006 and refinanced the second for $165,000.

Basically, they put nothing down and extracted about $130,000 in HELOC booty during their first four years of ownership. Now that prices have dropped more than 30% for small condos like this one, these owners are underwater and bailing out. Why wouldn't they?

They already extracted whatever the lenders was going to give them, and now with the large debt, it costs them far more than a comparable rental. Since they don't have any of their money in the deal, only their emotional attachment to the property or a sense of moral obligation would keep them paying. Since people don't often fall in love with tiny condos, and the moral obligation to repay debt is largely washed away, short sales like this one should not be surprising.

This is the type of inventory that will prevent appreciation until it is cleared from the market.

-$141 ………. Tax Savings (% of Interest and Property Tax)

-$401 ………. Equity Hidden in Payment (Amortization)

$18 ………. Lost Income to Down Payment (net of taxes)

$59 ………. Maintenance and Replacement Reserves

============================================

$2,099 ………. Monthly Cost of Ownership

Cash Acquisition Demands

——————————————————————————

$3,150 ………. Furnishing and Move In @1%

$3,150 ………. Closing Costs @1%

$3,040 ………… Interest Points @1% of Loan

$11,025 ………. Down Payment

============================================

$20,365 ………. Total Cash Costs

$32,100 ………… Emergency Cash Reserves

============================================

$52,465 ………. Total Savings Needed

Property Details for 165 ROCKWOOD Irvine, CA 92614

——————————————————————————

Beds: 2

Baths: 2

Sq. Ft.: 1125

$280/SF

Property Type: Residential, Condominium

Style: Two Level, Contemporary

Year Built: 1983

Community: 0

County: Orange

MLS#: P782595

Source: SoCalMLS

Status: Active

——————————————————————————

Wonderful Woodbridge living at its best. This is a completely remodeled townhome. Nice laminate hardwood floors, beautiful upgraded kitchen w/ granite countertops, new cabinets & appliances. Bathrooms have been remodeled and upgraded. Features scraped ceilings with recessed lighting. Keep cool with energy efficient attic fan and ceiling fans in both bedrooms. Both carports are directly behind patio. Enjoy the Woodbridge Village Association amenities, including the lakes, parks, sport courts, and much more!

RELAY FOR LIFE is THIS WEEKEND

June 11-12 (9:00 am to 9:00 am) CENTRAL PARK in RSM (Behind the Bell Towers, across from the movie theatres) The Relay event is a 24 hour team relay supporting our survivors and in memory of those we have lost and a fundraising effort on behalf of the American Cancer Society. As of this morning we have raised approximately $13,500 with only $1,500 left to raise to meet our goal of $15,000 for St. John's. We have about 30 official team members toward our goal of 50. There is still time to JOIN the official St. John's team on line (avoid filling out waivers on the day of the event) and/or DONATE to the team or a team member — www.relayforlife.com/ranchosantamargaritaca

You are welcome to make cash donations on the date of the event as well. Please note that the despite a possible misunderstanding, there are NO DOGS allowed on the track during the event, sorry. Please note that if you did not get your St. John's black shirts they will be available at the event, and those that pre-registered on line as a team member and raised $100 or more will also be provided with an official RSM Relay for Life T-Shirt as well. As in years past, St. John's will have a booth and will be providing free food and drinks all day to St. John's members as well as providing to the general population on a donation basis (all proceeds will go to the RSM Relay event).

On Sunday morning our own Bob Hayden will be making his “world” famous waffles as a fundraiser to the event as well. Please feel free to stop by and walk a few laps as part of our team and in support of those you have loved and cared about that have survived or fallen to this disease. Help wipe it out…..run, walk, eat, play…. ALSO, there is a silent auction taking place from 11:00 a.m. ending at 6:00 p.m. with over 35 baskets available for bidding (along with our own donated basket from Kathy O'Connor of fabulous Silpada jewelry).

Twenty-four year member of the Orange County Association of realtors, David R. Sparks, has admitted to lying to clients to cover up his fraud and theft in a $4,300,000 Ponzi scheme.

In every profession or organization there are a few bad apples. The behavior of a few does not necessarily reflect the values and actions of the many. Today we have the story of one really bad apple in an organization already rotting from within.

As I have stated on many occasions, chasing appreciation is a fool's errand. Unlike realtors who will tell anyone who will listen that prices only go up, I have been telling people to pay attention to the cashflow. That's where the real value is.

Chasing appreciation is part of today's story. The twenty-four year member of the Orange County Association of realtors made a massive bet on appreciation in rural Utah at the peak of the housing bubble in 2005. Given that he is a realtor, his poor judgment on the housing market is understandable, but the deception and fraud that followed is truly remarkable.

Ordinarily, I don't write about individuals, but like Michael Pines, he has achieved infamy without my help, and there is no way to tell the story without mentioning who he is.

David R. Sparks – a veteran real estate broker, former Irvine Planning Commissioner and active church-member – defrauded 34 friends, relatives and clients of $4,265,091 with an elaborate Ponzi-style investing scheme starting in 2007.

The 50-year-old Irvine family man cooperated with the FBI, confessed his crimes and agreed to plea guilty to felony interstate wire fraud, according to documents filed this week in Federal court in Santa Ana by the local U.S. Attorney’s Office.

At least one realtor is taking responsibility for his false representations about real estate appreciation.

Details from his signed plea agreement, two uncontested civil lawsuits and victim statements to The Register paint a picture of Sparks as a charming man and talented liar who claimed to be buying, rehabbing and selling foreclosed or pre-foreclosure homes that he never actually purchased.

Mr. Martinez, the reporter for the OC Register, should be careful when calling a realtor a liar.

If they did not want to reinvest their money with him, Sparks made up excuses for why he could not give it back.

As an upstanding member of the Orange County Association of realtors since 1987, Mr. Sparks embodies the character and ethics many have come to expect from realtors. The following is from his Active Rain profile:

I have been a full-time, professional REALTOR® since 1987 specializing in the sales and marketing of homes in Orange County, Long Beach and Coastal San Diego County. As a licensed broker, I am the owner of Sparks Realty, Inc.

Honest and full of integrity, I work to achieve a win/win situation in my transactions. While always keeping my clients' best interests in the forefront, I know that a truly successful transaction is one in which everyone feels as though they were treated fairly. As an excellent and open communicator, I owe much of my success to the fact that my clients always know exactly what is happening with their sale or purchase. By keeping everyone fully informed at every step, I makes the real estate process easy and stress-free. My constant accessibility as well as my knowledge of the industry and its affiliated services makes me the perfect choice for the real estate consumer interested in total service.

If you are seeking an honest real estate professional who is committed to your satisfaction and peace of mind, call Dave Sparks today.

The bold text is not added by me for emphasis. That was from Mr. Sparks. His honesty and integrity are beyond reproach since he is a realtor.

“We look forward to serving screwing you, your friends and your family for many years to come.”

Back to the OC Register article:

“I am glad he admitted to it but I am sorry I was a part of this,” said victim Aggie Kobrin of Irvine. “I am still very angry and very disappointed and that will stay with me a long time.”

The defendant started speculative real estate investing in the late 1980s, according to the plea agreement. In 2005, he believed that real property in Utah’s Cedar City was likely to see a dramatic increase in value, so he used his own funds and investor cash to buy 35 properties for approximately $7 million in Utah and California, the document says.

i give the guy credit for the courage to act on his analysis. Of course, he was as wrong as wrong gets, and he lost everything, and took his investor's money down the drain with him.

By 2007, the rents Sparks was collecting from the properties were no longer sufficient to cover the debt service.

Let's be real; the rents never covered the debt service. Cashflow positive properties were practically non-existent in 2005. By 2007, he ran out of whatever cash he had, and rather than admit defeat, he opted to commit fraud.

There must have been a moment only Mr. Sparks will understand when he realized he made a huge mistake. At that point, probably when the cash ran out and the market was plummeting, he had to make a choice. He could either admit his failure, tell his investors he lost their money, and give them back whatever he still had, or he could start a Ponzi scheme, delay the Day of Reckoning, and pray for a miracle. He chose the latter.

This was a choice. The twenty-four year member of Orange County Association of realtors had other options, and he chose to lie, cheat, and steal.

Sparks began soliciting cash from investors to cover the debts – deliberately lying to them by telling them the funds would be used to buy new properties. To back up his lies to investors, Sparks created false paperwork.

Sparks took in about $4.8 million under the false pretenses. He spent about $500,000 on “lulling payments” to the investors and about $4.3 million on his debt, the plea agreement states.

Lulling payments are money given to investors to placate their worries and buy time.

One thing that isn't clear to me is where the $4.3 million went. The debt service on $7 million in real estate over a few years wouldn't be more than $1.5 million at hard-money rates. Where is the rest of the money?

Sparks has agreed to pay the $4.3 million as restitution. That figure does not include any taxes the victims paid on the false profits, the costs incurred in the ordeal or interest payments and late fees promised in the investment agreements. Victims will have to seek reimbursement for that money via civil lawsuits.

Some assets are to be transferred to the United States government to liquidate. If his current assets and cash can’t cover the restitution, he will presumably have to pay the rest of it back from his earnings once he gets out of prison, if he goes to prison.

Since he is a member of the Orange County Association of realtors, he shouldn't have any problem finding clients willing to work with him when he gets out.

There is no minimum sentence for the Sparks’ crime and the maximum prison time he could get is 20 years. The U.S. Attorney’s Office in the plea deal agreed to recommend the lower end of that range, but that is ultimately up to the judge.

“Mr. Sparks’ agreement to plead guilty is an important step in his accepting responsibility for his fraudulent conduct,” Assistant United States Attorney Andrew Stolper said.

The guilty plea will also help his victims win their civil lawsuits against this member of the Orange County Association of realtors since 1987.

Two lawsuits were already filed in January – one by a 22-year friend of Sparks from Santa Ana and one by a married couple from Wisconsin. Sparks never responded to the courts, which handed the plaintiffs default judgments.

The FBI’s investigation did not find any evidence that Sparks is in possession of a large sum of money. But some victims say they still believe Sparks has money stashed away somewhere because he was “cheap” and didn’t like to spend money.

The fact that so much money is unaccounted for does raise suspicion.

The FBI began investigating Sparks in late January. Sparks resigned from the Irvine Planning Commission on Feb. 8.

Irvine City Councilman Steven Choi appointed Sparks to Irvine’s Planning Commission in December 2008. Sparks’ resignation letter to the city said the decision came “after careful consideration” and “discussions” with Choi but it did not give a reason for resigning.

Choi said Sparks told him he could not serve any longer because of personal business matters.

While running a Ponzi scheme, he served on the Irvine planning commission. Nice.

“This is a shock, because he appeared to me to be an honest man, and sincere,” Choi said. “I never expected he was involved in anything like this. It is very unfortunate.”

Choi said he first met Sparks when Sparks’ children – who are now adults – were coming to the Choi family’s tutoring center and the two became friends. He appointed the real estate broker to the Irvine Planning Commission because Sparks communicated that he had experience in real estate development out of state and because he had political experience as president of Irvine Republican Council.

“I haven’t analyzed his voting record, but as far as I know he did a good job as a commissioner and did not do anything wrong involving the city,” Choi said.

Fortunately, planning commission decisions do not manage budgets or expenditures.

The ordeal has caused financial hardship to several Orange County residents who say they personally trusted Sparks.

Gary Schultz of Huntington Beach and his father gave Sparks a combined $52,500 toward the purchase of three homes in the San Francisco area. Schultz knew Sparks from attending Westminster High School together.

He’s “a face-to-face guy” who is so cheery and nice that “you let your guard down around him,” Schultz said. He comes across like “Mr. Rogers,” but he is the “worst of the worst,” Schultz said.

Robert Edwin Anslow of Santa Ana, who was friends with Sparks for 22 years, provided $200,000 in 2007 for him to use toward the purchase, rehab and sale of a home in Simi Valley. Sparks reported that he purchased the property for $700,000 in 2007 and sold it for $910,000 in 2008. After allocating $64,000 in profit to Anslow, he talked him into reinvesting all of the money as an unsecured loan to Sparks for future investing. The problem: Sparks never bought or sold the Simi Valley home.

Later, when Anslow sought his money in accordance with the written agreement, he encountered resistance. After pressuring Sparks, he finally got back $100,000. Sparks defaulted on the other $100,000, as well as the interest and profit.

“He has put me in an extremely precarious financial situation,” Anslow said.

Sparks is president of several business entities, including Irvine-based Sparks Realty & Investment Inc. and the Nevada-based Wellington Grant Ltd. that he used in the fraud.

Sparks is also a twenty-four year member of the Orange County Association of realtors. Be careful who you trust these days.

Mortgage debt nearly three times the purchase price

The owners of today's featured property paid $199,000 on 9/13/1988, and now they have a $555,000 first mortgage. Hmmm… I think that qualifies as HELOC abuse.

My records don't go back all the way to their original purchase-money mortgage, but on 6/3/1998 they had increased their first mortgage to $221,250 which is $22,250 more than they paid.

On 8/4/1998 they obtained a $37,600 HELOC.

On 10/20/1999 they opened a $100,000 HELOC.

On 6/30/2000 they got a $90,000 HELOC.

On 11/5/2002 they refinanced the first mortgage for $318,000 and obtained a $62,000 HELOC.

On 9/9/2003 they refinanced with a $312,000 first mortgage and on 9/20/2004 they got a $250,000 HELOC.

On 6/30/2005 they refinanced with a $550,000 first mortgage.

Total mortgage equity withdrawal is at least $351,000, and if they put 20% down, the number is closer to $390,000.

Here they are selling twenty-three years after buying the property — only one year less than Ponzi scheme operator David R. Sparks was a member of the Orange County Association of realtors — and they are going to be a short sale.

Mediteranian style interior, corner lot . 2 story w/ 2nd floor. Hardwood floor upstairs master suite , cranit counter top. Jacuzzi tub custom built, double pain windows throughout the home, upstairs patio and much more. could also be a bonus room-inlaw, another master bedroom with full bath, downstais with 3 additional rooms and 2 full bath, itilian tile floor downstairs, Firplace, carpet in rooms. 2 separate airconditon unit, for up/down lots of mature fruits trees, large back yard. Close to shops parks, Schools. Library, Fwy 5/405. Property sold as-is This is a HAFA SHORT SALE worth the waite

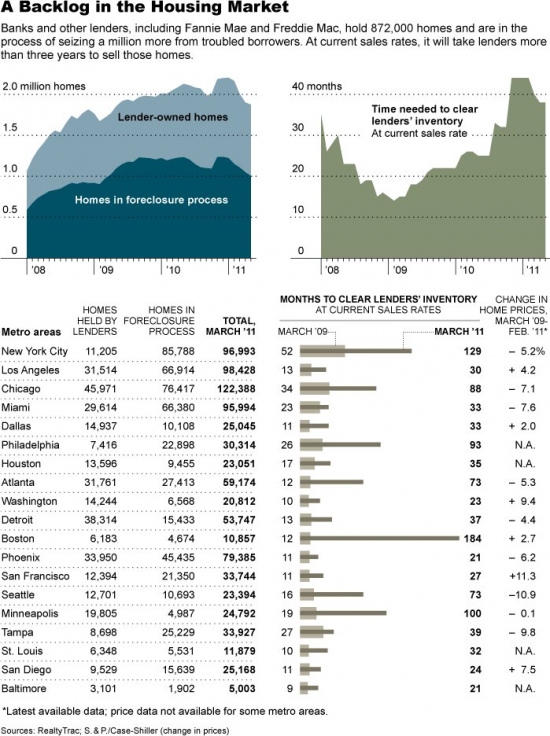

The one market with the fewest foreclosures relative to its mortgage delinquency is New York City — the homes of banksters are being spared foreclosure and the resulting declines in value.

Right through the very heart of it – New York, New York

Frank Sinatra — New York, New York

One of the most irritating behaviors I have witnessed during the deflation of the housing bubble is the way banksters have chosen to foreclose in some markets and allow delinquent mortgage squatters to flourish in others. The worst market in the entire country for shadow inventory, the place with the most delinquent mortgages and the lowest foreclosure rate is where the banksters live: New York City.

There is only one plausible explanation for this phenomenon: banksters are choosing not to foreclose in places where it would negatively impact the value of their personal real estate.

If pressed on the issue, they would likely spout some nonsense about New York City being different. It's special, everyone wants to live there, and so on. Markets obey laws of supply and demand, and right now, demand for overpriced NY real estate is very low, and the supply of shadow inventory is very high. Of course, that is shadow inventory. If they simply leave that inventory in the shadows, they can balance supply and demand and meter out these properties as the market can absorb them — at least that's the theory.

Strategic default will take over

There is one basic flaw with their plan. As more and more people stop paying their mortgage and don't get foreclosed on, the people who are paying their mortgage realize they are being foolish, so they stop too. Think about it; if you can possess property forever with or without paying for it, why would you pay? Moral obligation? On Wall Street?

Strategic default is usually associated with a beaten down market like Las Vegas where it is foolish to continue paying a $300,000 mortgage on a $100,000 house. However, at the other extreme is New York City where all consequences for default have been removed. And mortgage default has major benefit to someone putting 40% or more of their income toward a mortgage. Each person who decides to quit paying gets to keep their house, and they get to keep the money they used to put toward paying down the mortgage. For many it's like a 40% raise in pay.

We are quickly approaching a tipping point in New York City where residents recognize it is in their best interest to default and pocket the payments. Once that becomes common wisdom, strategic default will become the norm just as it has in Las Vegas. If lenders continue to allow these borrowers to squat, it will eventually rise to the level of entitlement on Wall Street. Everyone who works in New York City in finance will look to their company's REO for their housing and expect it to be free. If nobody else has to pay, why wouldn't they expect it for nothing?

Strategic default is not only a phenomenon of beaten down markets. If mortgage delinquency becomes rampant because borrowers know the repercussions are non-existent, strategic default will take over there too.

I never stated that the collapse was imminent. I said I had no way of knowing when the banks would start foreclosing on all those delinquent borrowers. But they will. Now is a good time to take a look at why the entire New York City (NYC) market is headed for collapse.

Based on the volume of shadow inventory in New York City, the housing market should collapse, but the banksters are determined to prevent this from happening even if that means giving away properties to delinquent mortgage squatters. New York City may be on its way to a decade-long slow deflation. If they sell the properties slowly enough, incomes will eventually come back. Right now it would take an astounding 129 months to clear out their backlog.

First, let’s see what’s happened to home prices around the country since the expiration of the first-time buyer tax credit. The best source for this is Clear Capital and its excellent Home Data Index (HDI) Market Report.

Since the end of last summer, home prices nationwide have plunged by an average of 11.5% through April 2011. Some of the worst major metros have fallen even more. Talk of home prices bottoming has stopped. For a year, I’ve been saying that there is no housing recovery in sight.

Yet NYC median home prices have held up pretty well during this period. Why?

Prices have held up in New York City for the same reason they are holding up here in Orange County: lenders are not foreclosing on delinquent mortgage squatters.

In my two articles about Queens, I pointed out that the servicing banks are simply not foreclosing on delinquent homeowners. They aren’t even putting them into default (NOD). Take a look at this chart from the first article showing the rise in serious delinquencies in that borough.

A year ago, 11.2% of all Queens homeowners with a mortgage were delinquent by 60 days or more. I obtained these figures from TransUnion, the credit-reporting firm which puts out a quarterly mortgage delinquency report based on its database of 27 million anonymous credit reports. In the first quarter of 2008, that figure was only 3.9%.

That 11.2% figure equaled roughly 25,000 seriously delinquent homeowners. This number was confirmed by a fairly recent NY Federal Reserve Bank report which stated that 10% of all first liens in Queens were delinquent by 90 days or more. Remember, these figures are for only one of five boroughs in NYC. The NY Fed’s report also showed a 90+ day delinquency rate of 11.8% for the Bronx and 9.5% for a Brooklyn.

The delinquency rates in the New York City boroughs are higher than the rest of the nation. With 25,000 delinquent mortgage squatters in Queens and a liquidation rate of less than 250 per month, it will take over 100 months to clear out the existing inventory.

Are the banks making any attempt to foreclose on all these delinquent homeowners who are living rent-free? You judge.

Let’s take a good look at this amazing graph. New York City has roughly 8 million residents, easily the largest city in the nation. The graph from PropertyShark breaks down the new foreclosure auctions (actually sheriff sales) scheduled by borough. You can see that the vast majority scheduled are for Queens. None of the other four boroughs exceeded 150 scheduled auctions in any month since the end of 2008.

Notice carefully that the peak number for Queens starts to decline well before the robo-signing mess occurred last fall. Sorry, that problem had nothing to do with the bank’s refusing to foreclose on delinquent homeowners. It did provide some cover for the banks, though.

Lenders will use whatever news story that's available to continue to put off foreclosure. They are trying to buy time because they know prices will crash if they liquidate. If they don't liquidate, their borrowers will figure it out and strategically default.

The plain truth is that for more than two years, the servicing banks have made no effort to foreclose on these seriously delinquent borrowers throughout the Big Apple. Take a look at these incredible figures for the number of NYC REOs for sale on foreclosure.com on May 30.

Repossessed Properties on the Market in NYC — May 30

Queens: 232

Brooklyn: 95

Bronx: 76

Staten Island: 75

Manhattan: 27

I’m not making these numbers up. Go to foreclosure.com and check for yourself.

So what does all this mean for the NYC housing markets? Homeowners in any of the five boroughs do not have to compete with foreclosures for sale as they do in every other major metro. So can they list their property for anything they want. And they do. Every once in a while, like the Venus flytrap, a seller is fortunate enough to catch a buyer.

That is the Orange County experience as well, particularly at the high end. I see delusional sellers all the time on Redfin who bought at the peak and think their property value has gone up. Occasionally, they are right. Of course, it requires borrowers to come up with enormous down payments, and as a result sales volumes are very low, but if lenders are willing to drag this process out for ten years, they might be successful. In the meantime, they will be supporting a lot of squatters.

Sellers don’t catch many, though. In Jonathan Miller’s thorough quarterly report on the Queens market put out by Prudential Douglas Elliman Real Estate, he counted a total of 2,483 1-3 family houses, coops, and condo units sold during the fourth quarter of 2010. That is roughly 830 per month. This is for a borough with roughly 2.2 million residents. These buyers paid a median price of $363,000. If you weren’t aware of what I’ve explained, you would think that the Queens market has held up fairly well. No way. The overwhelming majority of properties on the market in all five boroughs just sit … and sit … and sit.

That also sounds like Orange County.

Where All Five Boroughs Are Headed

At some point, the banks will be under tremendous pressure to foreclose on the huge number of seriously delinquent properties that are now either vacant or occupied by “walkaways” who have been enjoying the free ride longer than anywhere else. Look at this shocking chart from Lender Processing Services.

It shows that In New York State, homeowners with a notice of default (NOD) on their property have not made a mortgage payment for an average of 644 days. That is more than 21 months. Nice deal, isn’t it?

That is the best deal in the country. People who quit making their loan payments get two years of free housing. If they save that money, after the lender finally does foreclose, they can wait two years and buy another property. Since prices will likely continue to fall, particularly at the high end, they will repurchase at a lower price and have equity from their down payment. The people who don't strategically default will make payments and fall further and further behind.

When the banks begin to foreclose and dump the REOs on the market, prices in all five boroughs will completely collapse. This is almost as certain as night follows day. Ignore it at your own risk.

Keith will be focusing on the entire NYC housing market and the suburbs in the seventh issue of his Housing Market Report due out in mid-July.

Looking at the continuum of lender liquidation behavior, Las Vegas is on one extreme and New York is on the other. Desirability has nothing to do with it. Las Vegas has been pummeled by foreclosures and liquidation selling. New York has been spared any meaningful price declines because there are very few foreclosures and almost no liquidation selling.

Both Las Vegas and New York have a huge problem with mortgage delinquency and strategic default, but for opposite reasons. In Las Vegas, borrowers are hopelessly underwater and see continued payment as pointless. In New York, borrowers are offered two years of free housing if they quit paying, so many are taking advantage. Both markets have a huge shadow inventory.

Orange County has been somewhat more balanced in its foreclosure and disposition efforts. Lenders have foreclosed and process more homes at the low end than at the high end, so high end prices are still inflated while low end prices are nearer the bottom. Only time will tell which path is the correct one for lenders. For future borrowers, the tiny mortgages in Las Vegas will be a huge benefit. For buyers in the slowly deflating markets like New York, the huge mortgages will be an economic dead weight.

Get out while you can

With the leading edge of prices now in 2003 in Irvine, many 2003 buyers are chosing to bail while they still can. The owner of today's featured property paid $353,500 on 3/28/2003. She borrowed $282,000 and put $71,500 down. She opened a HELOC for $35,200 on 11/17/3003, but didn't add to her mortgage again until 1/8/2007 when she took out a stand-alone second for $80,000. Her total property debt of $362,000 is only slightly more than she paid. That's conservative by Irvine standards.

She must have fallen on hard times because she stopped paying the mortgage and decided to sell.

Foreclosure Record

Recording Date: 05/18/2011

Document Type: Notice of Sale

Foreclosure Record

Recording Date: 01/26/2011

Document Type: Notice of Default

She could be one of many working in a real estate related industry who succumb to the long recession. With no history of HELOC abuse, and what appears to be a relatively small mortgage, she could be an innocent casualty of the housing bubble.

-$325 ………. Tax Savings (% of Interest and Property Tax)

-$528 ………. Equity Hidden in Payment (Amortization)

$24 ………. Lost Income to Down Payment (net of taxes)

$72 ………. Maintenance and Replacement Reserves

============================================

$2,366 ………. Monthly Cost of Ownership

Cash Acquisition Demands

——————————————————————————

$4,150 ………. Furnishing and Move In @1%

$4,150 ………. Closing Costs @1%

$4,005 ………… Interest Points @1% of Loan

$14,525 ………. Down Payment

============================================

$26,830 ………. Total Cash Costs

$36,200 ………… Emergency Cash Reserves

============================================

$63,030 ………. Total Savings Needed

Property Details for 208 MONROE #152 Irvine, CA 92620

——————————————————————————

Beds: 3

Baths: 2

Sq. Ft.: 1495

$278/SF

Property Type: Residential, Townhouse

Style: Two Level

Year Built: 1985

Community: 0

County: Orange

MLS#: H10122016

Source: CRMLS

Status: Active

————————————————-

GREAT PRICE FOR THE LARGEST FLOOR PLAN TOWNHOME IN TIMBERLINE. 3 BR 2.5 BA 1495 SQ. LAMINATED FLOORING THROUGHOUT. OPEN FLOOR PLAN IN PRIME LOCATION. LOW HOA FEES.

Thank you, IHB readers

I want to thank everyone for the kind words of support yesterday. I hope to put the issue behind me, but depending on how foolish and vindictive the Orange County Association of realtors wants to be, we may see this story resurface again. Wouldn't that be fun? Perhaps they will quietly go away and drop their complaint. I'm not holding my breath.

The Orange County Association of realtors has accused IrvineRenter of “knowingly telling lies about competitors.” They demand I appear in front of their grievance committee for disciplinary action.

June 6th, 2011, 12:00 pm — Marilyn Kalfus, real estate reporter

The Orange County Association of Realtors has filed a grievance against an Irvine real estate broker who writes a blog that takes critical looks at the housing crash, homebuyers and real estate agents.

.

Larry Roberts, who writes the IrvineHousingBlog.com, freely admits going “over the top” in his posts, which are particularly harsh on homeowners who default on loans. He frequently shows MLS photos of properties that have gone into foreclosure. He also has accused real estate agents, in general, of being dishonest.

I sometimes do go over the top. It's part of my sense of humor, and It's one of the reasons I don't single out individuals. Sometimes it takes going over the top to draw attention to important issues and get people to think.

The grievance says Roberts and two other people have violated a code of ethics rule stating that “Realtors must not knowingly lie about competitors” as well as a general set of regulations governing how MLS information is used on the internet.

Roberts says OCAR is trying to impinge on his freedom of speech, and that the organization has no standing to keep him from posting in his blog.

This is clearly an attempt to silence my free speech because OCAR does not like the content of my speech. Why else would they bring this complaint? The complaint filed by OCAR is “anonymous” — nobody at OCAR has the guts to stand up and publicly accuse me. To make it worse, OCAR has not even notified me of what specific actions I took which violate their rules.

They want to drag me before a biased kangaroo court made up of its own members and keep the hearing secret and non-public. Anonymous accusations, secret trials, and refusal to substantiate charges sound more like the political trials of the Soviet Union, Cuba or North Korea than American notions of due process. Joseph Stalin from the old Soviet Union would be proud of OCAR and their methods.

He has a broker’s license, he says, but he doesn’t run a brokerage or sell real estate, and he is not a Realtor or a member of OCAR.

The complaint, which Roberts furnished to the Register, was accompanied by a printed version of a post he ran saying that real estate agents lie.

“Realtors take advantage of their status as trusted experts to manipulate buyers, and they feel no responsibility when their statements are exposed as lies,” the statement said.

Roberts says he believes he wrote it as an introduction to an article in the blog by a University of Arizona law professor. The piece, entitled, “Trust, expert advice and Realtor responsibility,” was later removed from the blog at the professor’s request because it was going to be published elsewhere, Roberts said.

In an interview, Roberts elaborated, saying, ” …Many Realtors make representations about investment value and appreciation without regard to whether or not such statements are true. Most make these statements in ignorance, which technically isn’t lying, but some make these statements knowing better, which is lying.”

Roberts added that while he has been hard on real estate agents in general, ”I have never singled any Realtor out and called them a liar.”

I don't focus on individuals. The behavior is the problem, not the person doing it. People make mistakes. I have. I don't seek to shame people, I try to point out what people do whether it be borrowers or realtors so people can see the wisdom or the foolishness in the behavior for themselves.

OCAR’s Rena Budesky, who signed the grievance, declined to answer questions from a reporter seeking specifics about what Roberts did to prompt the action. “Everything that relates to grievance complaints, it’s all confidential,” she said.

OCAR president Jean Tietgen did not respond to a reporter’s call.

They want to call me in front of their Kangaroo court of realtors, keep me in the dark regarding their trumped up charges, find me guilty, then keep everything quiet.

Roberts’ attorney Scott H. Sims sent a letter to Budesky and OCAR demanding they withdraw their complaint, which he called “frivolous .. and a clear effort to interfere with Roberts’ right of free speech.”

“Even if Roberts had engaged in wrongdoing, which he has not, any disciplinary action taken by an OCAR grievance panel would carry no legal force and effect and OCAR would be exposing itself to liability for any and all damages to Roberts,” the letter read in part.

“If OCAR or any of its members disagree with Roberts’ opinions they are free to dispute them in ‘the marketplace of ideas,’ ” the letter says, “and leave it up to the public to decide who is right .. We recognize that engaging in a civil debate about the health of the housing market may not blindly pad the pockets of OCAR’s members who are paid on commission — and thus have no incentive to tell their clients to do anything except to ‘buy,buy,’buy” — but such is the risk of doing business in a free market.”

Hallelujah! The IHB has always been an open forum. People are free to come here and put forward their ideas and opinions of the housing market. I have always encouraged differing points of view as evidenced in the daily astute observations. Ideas with merit are scrutinized, and the collective wisdom of the group separates the good ideas from nonsense. That's how a healthy debate should work.

The allegations brought against me include (1) knowingly lying about competitors, and (2) violating MLS rules. Yet OCAR won’t tell me how I did either. Isn't it obvious these are silly attempts to shut down one of the few truthful and accurate sources of real estate information and analysis in Orange County? They are pissed about my public comments, and they hope they can find some MLS violation to shut me down. In their complaint, they provided absolutely no evidence of any MLS violations. If there are any legitimate violations, they should tell me and give me the chance to correct them. Unfortunately, OCAR is more interested in keeping me in the dark, holding some secret proceeding and then trying to shut down the IHB and infringe on free speech.

Do any of you believe the information presented on the IHB is inaccurate or misleading in any way? Does OCAR need to sue the IHB to ensure the data presented is accurate and useful? Who do you believe is more concerned with accuracy, the IHB or OCAR?

This is really embarrassing for OCAR. I criticize the national association for knowingly providing inaccurate information to buyers — which they did — and the local association accuses me of lying and providing bad information. Unbelievable! I cringe when I think of the thought process that was behind this complaint. OCAR should be asking itself what the hell is going on. They want to call a non-member in front of their secret panel, and then make up bogus charges designed solely to infringe on someone's freedom of speech. Brilliant!

Isn't this America? Perhaps OCAR might be more comfortable in Communist China? Oops, I better be careful. I wouldn't want to get called in front of a disciplinary board in China for my statements….

What is wrong with the association of realtors?

My issues with the association of realtors is well documented:

Since Barry Ritholtz post on How to Read National Association of Realtors News Release, I have been contemplating the utter disrespect the NAr demonstrates for its customers through its constant manipulation of data for the sole purpose of convincing buyers to act even if it isn't in the buyers best interest to do so. It angers me that such a corrupt and self-serving philosophy of business is at the core of the NAr because their actions harm so many people.

How many buyers from the bubble rally were soothed by the comforting advice of their expert realtors who were telling them house prices only go up? How many of those buyers relied on their realtor's statements and now find themselves financially destroyed by the purchase they made? Are realtors responsible for the financial ruin of those buyers who believed their representations of financial performance?

On 3-23-2011, I wrote the post As trusted experts realtors are responsible for their bad financial advice. That post was a reprint of Dr. Brent White's paper, Trust, Expert Advice, and Realtor Responsibility. From the abstract:

Real estate agents benefit from the trust associated with portraying themselves as real estate experts, yet are generally not legally responsible for the advice that they give. This lack of legal responsibility is at odds with psychological propensity of individuals to trust perceived experts. It also creates a genuine moral hazard, fueled the housing market bubble and contributed to the suffering of homeowners whose real estate agents encouraged them to buy as the market began to burst. This article proposes that real estate agents be required to accept legal responsibility for their advice or be required to represent themselves as mere salespersons.

My post is no longer on the IHB. As mentioned in the OC Register’s article, I emailed Dr. White when my post came out, and he requested I take it down because the paper was about to be published in a major journal, and he didn't want problems with his publisher. Since I was trying to help Dr. White by calling attention to his paper and not cause him grief, I took the post down per his request.

The post containing Dr. White's paper is apparently part of the the OCAR complaint against me — A post that was 90% someone else's writing. I was drawn to Dr. White's paper because he was making the same argument I was in The Great Housing Bubble and in many posts on the IHB: realtors should stop making representations of financial returns in real estate as an inducement to buy.

Since one of the goals of regulatory reform is to inhibit the behavior of irrational exuberance, the sales tactics of the National Association of Realtors should be examined and potentially come under the same restrictions as securities brokers through the Securities and Exchange Commission. After the stock market crash which helped precipitate the Great Depression, Congress created the Securities and Exchange Commission to regulate the sales activities of securities brokers. There are strict regulations in place governing the representations made concerning the future performance of investment opportunities. These protections were put in place to protect the general public from the false promises made by stockbrokers in the 1920s which many naïve investors believed. The same analogy holds true for Realtors. The National Association of Realtors has launched numerous advertising campaigns suggesting erroneously that residential real estate is a great investment and appreciation will make home buyers wealthy.

Some people mistakenly believe that realtors are regulated by the SEC and need a securities license to make representations about returns in real estate. Not true. They say whatever they want, and if a buyer relies on that information, too bad for the buyer.

In the complaint against me, the post with Dr. White's paper is singled out as evidence that I “knowingly lied about my competitors.” In an amazing example of cognitive dissonance, OCAr is accusing me of lying.

I believe this is an attempt to silence my voice and undermine my business. What other explanation could there be?

OCAR should leave me alone

Is spending OCAR resources on this complaint in the best interest of the organization? If OCAR is trying to vault me to national attention through its frivolous lawsuit, they just might succeed if they don't let their complaint drop. Dr. Brent White, the author of the paper that was the subject of the post they objected to, was on 60 minutes for his controversial stance on strategic default. My attorneys represented Tyler Hamilton on his recent 60 Minutes appearance. Producers at 60 Minutes are contacts of both Dr. White and my attorneys. Is attacking my freedom of speech on the issue of realtor responsibility newsworthy enough for 60 minutes? If they keep pushing, we might find out.

I am not looking for a fight. Personally, I would rather focus my energy on developing my own business and holding to a higher standard. If the people behind the complaint against me were to put a fraction of that energy toward raising their own standards and creating their own success, they might serve their clients better and make more sales.

Shevy is a personal friend and we speak regularly about the market and ways that real estate services can be improved. Shevy is a member of OCAr, NAr, and participates in LGrS through OCAr. He participates in these groups to bring perspective and hopes of influencing positive change for consumers through OCAr and NAr policy improvement. He was very surprised and disappointed that OCAr chose this path. Open forums like the IHB should be embraced by groups like OCAr and NAr as an opportunity to gain insight and address important real issues.

What is a lie?

First, let's dispense with their allegations. In order to tell a lie, someone must know the facts of a situation and knowingly state something contrary to fact. Let's look at my statements and contrast that with statements of some realtors and representatives of their association.

I have stated uncomfortable truths (see links above), but I have not lied about anything. Like Dr. White and Barry Ritholtz, I happen to believe that realtors do at times make misleading statements about house price appreciation to induce a buyer to act. My statement is my reality. If I am mistaken, and if no realtor has ever made an intentionally misleading statement as to future value of a house, then I am mistaken, not a liar. That being said, I don't think I am mistaken:

In the video above featuring NAr representative Tom Adkins above from 2008, he is embarrassingly wrong, and as Peter Schiff points out, he was just as wrong the year before. But why does he keep saying it? Does he know better and chooses to lie? Is he ignorant to the truth and merely passing on his foolish opinion?

Not every instance of a realtor making representations of financial rewards is intentionally misleading. Sometimes they are merely delusional and genuinely believe what they are saying. The post The OC Register Says California had no real estate bubble documents that phenomenon rather clearly.

… it was fascinating to watch the realtor mind at work. The presentation included many “reasons to buy” realtors could use in their own manipulations consultations with customers. There was little or no regard for the veracity of the claims, it only mattered that realtors have something, anything to create urgency in buyers. Many realtors see their job as presenting buyers with reasons to buy, any reason, and hope the buyer is gullible enough to believe them.

The lack of concern for the truth is the defining characteristic of bullshit. When the bullshit is being offered to obtain a sales commission, the bullshit is self serving. How would you characterize the ad below from the peak of the housing bubble in 2006? It was the worst possible time to buy real estate as an investment. Everyone who did so lost money, yet the NAr claimed real estate was a great investment in 2006.

How would you characterize the behavior of the NAr when they put out advertising like this? They were obviously totally wrong.

Were they lying?

Were they delusional?

Or were they bullshitting showing an indifference to the truth?

And are any of those answers acceptable to you?

So what does the general public think of OCAR's complaint?

Who's Dat says: It’s given that Realtors are liars. How many times have we been told “Now is the best time to buy…”?

NueeArdente says: All salesmen do their best to make a sale, yes that means manipulation… and while many might not lie outright.. I can see truth stretched like taffy quite a bit. Then theres a whole pack of them that knowingly sold homes to families that could not afford it while the banks enabled that behavior.

BigLandlordsays: I will double the vote that 90% of Realtors LIE all the time! I know, I was a Realtor from 1976 to 2006. LEFT A VERY BITTER TASTE IN MY MOUTH Dealing with so many LIARS. That’s why Escrows are so complicated & take so long!

jules says: It’s true… Realtors do lie. And, it’s not just one life…it’s one lie after another. I have experienced it myself. Why do you think so many people fell for these overpriced homes over the last several years? I realize that realtors weren’t the only factor, but I experienced it myself. The realtor kept lying and lying. Inside I was thinking “Wow…” I can’t believe that anyone would behave this way… Amazing…

jon says: Realtors are getting DESPERATE. They can’t stand the truth. 6% is above God and morality. IHB is nice enough not to call them names, but I will. Realtors = Rodents.

mojoj says: The statement in question about investment values of homes was exposed in the book Freakomics. In the book, they had a real life example of a real estate agent that urged the home buyer to purchase the home because it was a good investment. Shortly thereafter (with no measurable shift in the market, the buyer sought out the same agent to plan on selling the house to benefit from the “investment”. The agent then told him that it was a down market and that it wasn’t a good time to sell a home. The book also shows that real estate agents don’t have enough of an incentive to maximize the sale price of your home so they settle on what gets them the most amount of money with the least amount of effort without regard to your best interests. We all know this, but it looks like some local buffoons want to sue someone for blogging about it.

ocbear says: During the housing bubble, the National Association of Realtors were huge cheerleaders getting people in over their heads, and are a big cause of the whole mess. The post cards that I received from realtors during those years contained so many lies I couldn’t believe it!

And my favorite:

Surprised says: The only thing I am going to say is that there needs to be a new industry trade group.

I challenge the NAr to raise their standards

There is a simple reason the local realtor association wants to harm the IHB: Their customers prefer the higher standard we set, and we are taking their business. I offer a series of challenges to the association of realtors.

1. Stop presenting inaccurate data to suit your purposes.

Back in 2007, realtors changed their methods of data collection to get the data they wanted to present rather than be accurate to what really occurred in the market. I documented this in National Association of realtors caught lying about home sales. This behavior needs to stop.

2. Stop manipulating accurate data with spin and bullshit to influence buyers.

Zillow's Stan Humphries among other real estate economists, has demonstrated a willingness to tell a dark truth about home prices or sales regardless of how this will impact Zillow's business in the short term. Telling potential customers the truth generates more sales in the long term than ceaseless bullshit.

3. Stop encouraging agents to create a false sense of urgency.

In Urgency Versus Reality: realtors Win, Buyers Lose, I documented what everyone already knows — realtors rely on creating false urgency to sell homes. Shouldn't people be given accurate information and be encouraged to make their own decisions? I think so. And so do the customers we have served. realtors need to stop creating false urgency in buyers.

4. Place the needs of your clients above your own.

Since I announced the IHB would help people buy and sell real estate, I have remained truthful to my view of the housing market. The IHB has consistently advised caution, while realtors were consistently calling the bottom and telling people they have nothing to fear. Many people have chosen to rent because of our advice, and since prices are still falling five years after the peak, our advice has served clients well. The IHB could have generated more sales if we had “gone realtor” and put our own financial interests above our clients. We chose not to do that because we believe it is the right thing to do. I challenge realtors to do the same.

5. Admit the sales techniques encouraged by the organization hurt millions of customers — and apologize.

Most realtors who read this — and they all will with the attention this issue is getting — will dismiss my challenges as the ravings of a hater. Nothing could be further from the truth. I would rather see everyone who buys real estate be treated the way IHB treats its clients. I rant and rave to foster change, not hate.

Many good agents don't like how their trade association works, but they feel powerless against the machine. They aren't powerless. Many secretly agree with me, but feel compelled by the pressure of the group to say nothing. Now is the time to stand up and be heard. Good agents need to raise their standards and demand the same of everyone else in the organization. Clients everywhere would benefit from that.

Better and more useful data

The property profile below is typical of an IHB post. It has two links to MLS sources for more information than is presented here. From the MLS data, which gets much of its information from the County Assessor's office and other public records, I break down the cost of ownership and acquisition. It's a shortened version of an IHB Fundamental Value Report. The data presented is accurate, and I provide more information that is useful to borrowers than other sites.

Learning what not to do

In addition to the basic property data, I provide purchase and loan information on the property from public records. Prior to the housing bubble, this information was dry data, but with the mass financial insanity that became common during the bubble, the public records now contain interesting stories of foolish borrowing that cost people their homes.

When I first began writing about this behavior, people didn't believe me, and for the first several posts, most dismissed it as cherry picking. Over the last four years I have profiled hundreds of HELOC abuse cases to show how widespread this activity really was. And for the record, I don't print the owner's names. It is public record, but I want to expose the behavior, not the person caught up in it.

The owners of today's featured property paid $377,000 on 12/14/2001. The first mortgage information is missing, but they needed a $75,000 second to close the deal. Their down payment probably wasn't very large. It doesn't really matter because on 4/16/2003 they obtained a new first mortgage for $436,500 which refinanced their previous mortgages, got back their down payment, plus gave them over $50,000 for spending money.

Over then next four years they took out various loans and refinances, and ended up with $674,260 in property debt. Hence, we have a short sale. The total mortgage equity withdrawal was around $300,000. Not bad for doing nothing.

A superb opportunity to acquire this stunning and spacious Two-Story Home with Just One Common Wall for a great price. It truly feels like a Single Family Residence. This home boasts an elegant front yard leading to the tastefully upgraded interior. The gourmet kitchen with granite countertops and matching appliances is a delight for every Chef. The crownmolding complements the high quality tile floors and the newer carpet throughout this bright and spacious home.

House prices volatility, both up and down, results from residential real estate appraisers using the comparative sales approach without considering a properties potential rental income.

Most people would agree that preventing financial bubbles is preferable to cleaning up the mess in the aftermath. The ups and downs of housing prices must end. The housing bubble shattered the dreams and aspirations of a generation. Some of the wealth lost was an illusion, but those who lost their family homes lost something tangible and real.

Great Britain is trying to recover from its fourth housing bubble in the last 40 years. That rivals California's three bubbles during that span. They too are looking for answers to prevent bubble number five from wiping out their wealth and their economy.

London: UK lenders should cap mortgages at 90 per cent of the property's value and no more than three-and-a-half times a household's annual income to prevent another housing bubble, the Institute for Public Policy Research said.

In The Great Housing Bubble, I proposed capping lending at a 90% loan-to-value ratio just as this group has done. I like the idea:

There are a number of reasons why high combined-loan-to-value lending is a bad idea: (1) it promotes speculation by shifting the risk to the lender, (2) it encourages predatory borrowing where borrowers “put” the property to a lender, (3) it promotes a high default rate because borrowers are not personally invested in the property, (4) it discourages saving as it becomes unnecessary, and (5) it artificially inflates prices as it eliminates a barrier to market entry. This last reason is one of the arguments used to get rid of downpayment requirements. The consequences of this folly became readily apparent once prices started to fall.

Also in The Great Housing Bubble, I explored capping the loan-to-income ratio, and I found the approach lacking:

Another proposed solution is to regulate the loan-to-income ratio of the borrower. When 30-year fixed-rate mortgages first came out, mortgage debt was limited to two and one-half times a borrower’s yearly income. It was an artificial limit that made sense when interest rates were higher and people were accustomed to putting less money toward housing payments. A legislative cap on the loan-to-income ratio would prevent future housing bubbles, if it was enforced. This would not work for the same reason lenders went away from the two-and-one-half-times-income standard years ago: it does not reflect changes in borrowing power due to changes in interest rates. This idea of regulating loan-to-income ratios is actually an evolution of the idea of regulating interest rates. If the total loan-to-income ratio is limited, very low interest rates do not cause dramatic price increases, but since low interest rates were not really the cause of the bubble, limiting the loan-to-income ratio is not addressing the real cause of the bubble. Plus, there are ways to get around a cap on home loan borrowing by obtaining other loans not secured by real estate. It would be relatively easy for a borrower to obtain bridge financing to acquire a property and then obtain a HELOC to pay off the bridge financing. In the end, the borrower would have borrowed more than the cap amount thus rendering any cap meaningless. To close the various loopholes, more regulations would be required, and a regulatory nightmare would ensue.

Back to the article:

The UK's “addiction to house-price inflation” is damaging the economy and the Conservative-led coalition government should make price stability a priority, the London- based advisory group said in a report.

“Britain has suffered four housing bubbles in the last 40 years, each of which contributed to major economic and social problems,” Nick Pearce, a director at the IPPR, said in the statement. “We need tougher mortgage-market regulation from the FSA, especially caps on loan-to-value and loan-to-income ratios.”

The Financial Services Authority regulates UK mortgage providers and other lenders. House prices tripled in the ten years through 2006, rising by 12 per cent a year, IPPR said. Mortgage lending is 81 per cent of GDP in the UK compared with 73 per cent in the US.

No deposit

The average loan for a first-time buyer was 3.15 times annual household income in March, IPPR spokesman Richard Darlington said by e-mail. In 2007, when the UK's real estate market peaked, 28 per cent of all advanced mortgages had loan-to- income ratios of 3.5 or more. First-time buyers regularly took out mortgages of 100 per cent of the property's value.

Great Britain was doing the same stupid things we were in the United States.

… Fall in demand

Mortgage applications in the US fell for the first time in five weeks as refinancing cooled.

The Mortgage Bankers Association's index of loan applications dropped 4 per cent in the week ended May 27. The group's refinancing index declined 5.7 per cent and the purchase gauge was unchanged.

Falling home prices are keeping more buyers on the sidelines while making it harder for homeowners to refinance current mortgages. Unemployment at 9 per cent and the prospect of more foreclosures in the pipeline mean housing will take time to recover.

“Nobody wants to buy an asset they think will go down in value,” Neil Dutta, an economist at Bank of America Merrill Lynch in New York, said before the report.

Capping lending and tethering it to a reasonable and affordable percentage of borrower income is essential to prevent future housing bubbles, but the problem is more complex because capping a loan at 90% value requires understanding what value is. Our current approach to residential property valuation relies exclusively on comparative sales, and it is a flawed system.

The income approach appraisal

When lenders underwrite investment property loans, they have an appraiser establish fair-market rents, and they generally consider between 65% and 75% of that income toward qualification for the loan. In places were properties are trading 25% or more below rental parity, the net income of the property will cover the payment, taxes, and insurance. These are low risk loans for lenders that provide them higher interest rates.

If applied to a typical residential real estate transaction, an income approach appraisal would reveal which properties generate sufficient cashflow to cover the loan in the event the lender had to take the property back. If lenders had the income information to compare to comparable sales, they would quickly see which properties are inflated in price and are thereby the riskier loans.

Loans on properties in Orange County with a negative cashflow should require larger down payments and more borrower income and assets. In contrast, a Las Vegas property with a positive cashflow would require smaller down payments and no other collateral to cover the loan. In the event of foreclosure, a lender could rent out the cashflow positive property and receive their desired income stream which effectively mitigates their risk. Lenders take on more risk than they realize when they loan on cashflow negative properties.

There is one potential market-based solution that would require no government regulation or intervention that would prevent future bubbles from being created with borrowed capital: change the method of appraisal for residential real estate from valuations based exclusively on the comparative-sales approach to a valuation derived from the lesser of the income approach and the comparative-sales approach. … In the current lending system, the income approach is widely ignored.

… When the fallout from the Great Housing Bubble is evaluated, it is clear that the comparative-sales approach simply enables irrational exuberance because the past foolish behavior of buyers becomes the basis for future valuations allowing other buyers to continue bidding up prices with lender and investor money. Prices collapsed in the Great Housing Bubble because prices became greatly detached from their fundamental valuation of income and rent. This occurred because the comparative-sales approach enables prices to rise based on the irrational exuberance of buyers. If lenders would have limited their lending based on the income approach, and if they would not have loaned money beyond what the rental cashflow from the property could have produced, any price bubble would have to have been built with buyer equity, and lender and investor funds would not have been put at risk. There is no way to prevent future bubbles, and the commensurate imperilment of our financial system, as long as the comparative-sales approach is the exclusive basis of appraisals for residential real estate.

When I wrote those words, the deflation of the housing bubble had not overshot to the downside in any market. My focus above was on preventing prices from going up too much, but this approach can also address problems we are seeing in markets like Las Vegas where prices have gone down too much.

In a declining market, lenders are cautious because nobody knows what anything is worth, and if lenders underwrite big loans that subsequently go underwater, borrowers walk away from their debts and leave lenders holding collateral worth less than their loan balance. As a consequence, lenders want to be conservative, so they rely on appraisers to keep values comfortably within range of recent comps, no matter how low those comps may be.

There comes a point when recent comps are so low that a property is undervalued based on its potential for cashflow, but since lenders don't use the income approach when evaluating residential real estate, they are not aware of these key price support levels and they approve short sales and REO resales at very low prices. An example comes from a recent community I saw in Las Vegas:

I discovered this neighborhood while looking at another auction property nearby. The property of interest is in a cluster product neighborhood in a nice part of Henderson, Nevada. All the properties were built in 2005 and sold new in the mid 200s.

The list of comparables below are all in the cluster neighborhood, and they are arranged in descending order of closing dates. Take a careful look at the sales price in the column second from the right.

The properties in the above list would all rent for about $1,000 to $1,100. The properties that sold in the $110,000 to $115,000 range represented good cashflow investments yielding 8% or more. In an environment of 1% CD rates and 4.5% mortgage interest rates, an 8% yield is fantastic. The resale value of this neighborhood did not need a 40% reduction to attract buyers. Lenders should never have approved those sales.

If the lender had merely rented their property out instead of dumping it for 40% under comps, the cashflow from the rental would have been nearly double the cashflow from the subsequent loan on the property. A lender in Las Vegas trying to finance its own REO would be well served by renting the property instead. Lenders can get $450 per month in a loan payment if they sell it and underwrite the new loan, or they can net about $750 a month on the rental if they keep it.

Of course, banks aren't REITs, and they don't want to own property long term, but in the short term, they would be much better off renting property. The could dispose these assets through a special home investment trust. An entity receiving the positive cashflow from the millions of rentals would have significant value, and it would provide better asset recovery than lenders are getting now.

Sell with new debt or keep as rental?

For example, B of A and other major banks try to sell their REO to people who take out loans from them. B of A gets capital out of a non-productive asset and converts it to loan payments. They can hold this new loan on their balance sheets or they can sell it in the secondary market. With Bernanke giving them free money, most banks are keeping the best loans for themselves.

However, instead of converting this non-performing asset to a performing stream of income by selling the property and underwriting a loan, the bank could retain ownership and rent the property. Banks would get more value from these properties by selling off the shares of a cashflow property REIT than they will by underwriting loans with much smaller cashflow.

If lenders also looked at cashflow values in terms of rental yields, they could see when they are selling undervalued properties and chose to rent those out instead. The amend, extend, pretend policy they are using to prop up prices in some markets is an attempt to hold on to what they believe to be undervalued assets. But since they are not looking at cashflow, they have no idea which markets have undervalued properties and which ones are overvalued.

In Las Vegas, some version of amend, extend, pretend is the best course of action for lenders because they can rent the properties and obtain better cashflow than if they sold them and put new debt on them. In Orange County, most properties are still reselling for more than rental parity, so lenders cannot rent them out for better cashflow than selling them and putting on new debt.

If lenders were basing their decisions on rental cashflow value — something they could do if they were obtaining appraisals using the income approach — they would quickly realize (1) they are selling properties they should be holding, and (2) they are holding properties they should be selling.

In a recent article, Dean Baker pointed out the foolishness of current government policies toward housing:

As far as the housing market, a little clearer thought would get policy to distinguish between markets where the bubble is still deflating (e.g. Seattle, Los Angeles, Boston) and markets where prices are likely overshooting on the low side (e.g. Los Vegas and Phoenix). It might make sense to have policies to boost prices in the latter set of cities. It makes no sense to have policies to boost prices in the former.

Mr. Baker proposes the right-to-rent as a public policy to address this problem. I believe income approach appraisals would give lenders better valuation tools so they could make better decisions concerning property liquidations on a market by market basis. Any lender looking at rental parity would liquidate their holdings where prices were inflated and hold properties where prices have overshot to the downside. Currently, that is the opposite of what lenders are doing, and their failure to understand valuation is going to cost them billions of dollars while the liquidations go forward over the next several years.

Large down payment lost

The owner of today's featured property paid $645,000 using a $417,000 first mortgage and a $228,000 down payment. He obtained a $100,900 HELOC on 1/15/2008, but there is no indication he used it. If this property sells for its current asking price, the owner will get a check for $6,000 of his remaining equity. That's $228,000 put in and $6,000 coming out. This was probably not the real estate investment this owner was looking for.