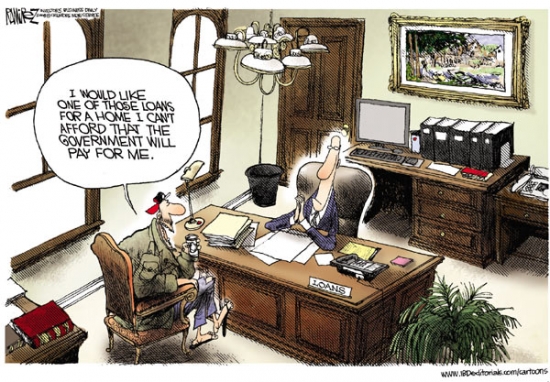

Richard T. Cirelli, President of RTC Mortgage Corporation, has proposed a series of self-serving policies to make his company more money, inflate house prices, and pass the risk on to US taxpayers. Needless to say, I disagree with his ideas.

Irvine Home Address … 9 OAKDALE Irvine, CA 92604

Resale Home Price …… $595,000

I used to flee safe

in the realm i did create

now i am all alone and cold

all my integrity has vanished

replaced with all the darkness

that's crawling inside

i realized that i had failed

pain, death, and deceit

Entrapped in a realm of insanity

The Sins of Thy Beloved — Partial Insanity

realtors aren't the only ones in the real estate industry who like to propose self-serving bullshit. Today a mortgage company executive is doing the same.

A Partial Solution to the Housing Crisis

July 14, 2011 — Richard T. Cirelli, President of RTC Mortgage Corporation

I think we can all agree on two things…

1. The economy won’t recover without a recovery in housing and 2. Underwriting guidelines are too tight.

No, actually we don't agree on those two things. Underwriting standards are not too tight. Lending is returning to prudent standards under which borrowers can make their payments and sustain ownership. Gone are the standards that were used to inflate a massive Ponzi scheme.

What follows is a series of proposals designed to put unqualified borrowers into loans by passing the risk onto the US taxpayer. It is the only way to sustain current pricing. What I think we can all agree on is that current pricing cannot be sustained by the number of borrowers who meet conservative lending guidelines. Where we disagree is on what should be done about it.

I don't believe we should try to sustain current inflated pricing by moving to an origination model where lenders have no risk and endlessly lobby the government to lower GSE and FHA standards so they can make more money from riskless originations. Supply and demand must come back into balance at price levels sustainable by private lenders who have evaluated the business risk and set interest rates and qualification standards. This must be private money that does not rely on government guarantees.

The result of the following proposals would be a completely government-backed housing mortgage market with significant taxpayer risk which supports a faulty origination-based business model that will inevitably inflate another Ponzi scheme and collapse when borrowers default. Only this time, the government will be liable for all the losses that should be absorbed by private lending.

Much has been said about underwriting guidelines being too tight. Fed Chairman Ben Bernanke admitted it in his press conference last month.

No, Bernanke did not admit that underwriting guidelines were too tight. Guidelines are tightening, and that is making mortgages harder to obtain, but that does not mean standards are too tight, it merely means standards have not tightened enough yet and we are still in the tightening process.

The majority of the U.S. senators said it in a letter to the U.S. House Committee on Financial Services in an effort to stop the proposed Qualified Residential Mortgage (QRM) bill that would make underwriting guidelines even tighter (there has been no ruling on QRM yet).

It’s been estimated that between 25% and 33% of the loans that are declined are “near misses” – people that fall just outside the guidelines but are otherwise qualified.

Aren't loans failing to meet government guidelines on the fringes supposed to create opportunity for private lending? Isn't that a good thing? Lenders should be cheering each tightening of government standards because it creates opportunities for them to make a loan on the fringes were risk is the smallest. In fact, the tightening of government standards and the resurgence of private lending is what we all want to see happen to stabilize the housing market. We must eliminate the system of government guarantees backstopping 98% of the loans in America.

Here are my thoughts on what’s wrong and how it can be improved without costing the government or the taxpayers more money.

Every one of these ideas will shift risk to the US taxpayer away from private enterprise which will cost the government and taxpayers more money. That is the nature or risk. Over time, the assumption of risk costs money. Just ask anyone in the insurance industry.

It’s my list of underwriting guidelines that are hindering the recovery and contributing to the continued slide in home prices

Before you read on, understand that I.m not advocating a return to the ridiculously loose days of no money down, no-income documentation, subprime loans.

Advocating loans just below the extremes of stupidity is still wrong. The free market must find the appropriate level of risk and price it accurately. What he is advocating is for the government to get behind the stupidest loans imaginable without going all the way back to the bubble peak. In other words, he wants to partially inflate the Ponzi scheme.

I’m suggesting some common sense ideas and tweaking of the existing guidelines that would enable more qualified people to buy and refinance their homes to help the economic recovery.

The age old appeal to common sense. Bullshit. Common sense is that you and I and every taxpayer does not want to pay the bill when some irresponsible borrower can't pay the mortgage.

• Eliminate Loan Level Price Adjustments (LLPAs)

These are adjustments to the cost or rate of a loan according to certain risk factors. Fannie Mae and Freddie Mac created these additional cost factors shortly after the government’s seizure of the agencies in late 2008. The most common LLPAs are for credit score and equity but others may also apply. The problem is that the borrowers that are most marginally qualified have to pay the highest rate, thereby creating a handicap right from the start.

The most marginal buyers should pay the highest rates because they are the ones most likely to default and cause losses. Has anyone noticed how high FHA insurance has become? FHA is the new subprime, and rather than raise the interest rate, they charge a 1.15% insurance fee that effectively raises the interest rate to over 6%. This is what should be happening to properly price risk.

It affects first-time homebuyers the most since they usually have the lowest down payments. It also affects homeowners that would like to refinance into a lower rate thereby making their home more affordable and the owner more likely to stay even if they have lost their equity. Instead, they may be forced into a higher rate simply because they had to increase their use of credit cards during a difficult period which lowered their credit scores while their equity diminished due to the economy.

Nobody had to increase the use of their credit cards. People could have made a choice to cut back on their entitlements. If they didn't choose to cut back on their spending, they are the most likely to default on their loan if the going gets really tough.

In short, loan level price adjustments are a good idea as it matches risk and cost.

• Prohibit Overlays

Overlays are restrictions or additional guidelines that some lenders impose that are stricter than the standard Fannie Mae/Freddie Mac guidelines. They often apply to the borrowers Debt-to-Income ratio thereby eliminating some borrowers that meet the industry guidelines but fall just outside of the guidelines of the particular lender that they unknowingly chose. Many lender-imposed overlays are seemingly minor adjustments, but collectively they prevent many potential homebuyers or refinancing homeowners from qualifying simply because they inadvertently chose a lender with an overlay that disqualified them. I’m in favor of requiring all lenders to offer the Fannie Mae/Freddie Mac guidelines without overlays.

Lenders have the right to impose whatever restrictions they want. If they are more conservative than they need to be to comply with the GSE standards, then competition should drive business away from them to lenders who are closer to the GSE standard. These should not be prohibited as the free market should make them go away in time on their own.![]()

• Loosen Condominium requirements

A condominium project with less than a 51% owner occupancy rate or with more than 15% of the homeowners delinquent in their HOA dues is disqualified from Fannie Mae and Freddie Mac financing. So, what happens when the project no longer meets the guidelines? It instantly prevents all potential buyers from buying, sellers from selling and existing homeowners from refinancing. That in turn forces the value lower for all units in the project. And, more unit owners are likely to walk rather than make their payments as they become increasingly further under water. There may be qualified investors willing to buy the backlog of inventory in many condo projects if they can finance them now and later re-sell them to someone that can obtain a mortgage. Wouldn’t it be better to have a project with 40-50% investors or 16% delinquency than one with 100% of the units unmarketable?

No matter how loose you make the requirements, some projects are not going to meet the standard. To characterize these as 100% unmarketable is bullshit. These units are still marketable to cash buyers. in fact, these communities are a special opportunity for cash buyers who are willing to come in and clean up the mess. What bothers the author is his inability to generate a loan commission while cash buyers do their thing.

• Regulate or License the Underwriters

Does it seem strange that the underwriters charged with the responsibility of making the decision as to who qualifies do not need to be regulated or licensed? Mortgage Brokers have to be licensed and pass rigid state and federal exams and background checks. But those that are responsible for approving or denying a loan don’t. In my experience, the underwriters that have the least amount of experience or confidence will create the largest number of conditions when underwriting a loan. If the borrower can jump through enough hoops or provide enough documentation to compensate for an underwriter’s lack of ability, the loan might be approved. I’m sure all lenders have their own internal system for monitoring their underwriter’s performance but this most-important part of the process is not consistent. (Note-FHA underwriters do have to be licensed but Fannie Mae/Freddie Mac underwriters don’t).

I'm not sure what this will accomplish. It sounds like he wants them licensed so they will be requried to approve more of his dodgy loans.

• Extend temporary loan limits to 729,750 indefinitely

Congress temporarily increased the loan limits for certain high-priced markets such as Orange County from $417,000 to $729,750. While these temporary limits were extended last year, they are set to expire again and be reduced to $625,500 on September 30, 2011. While there are some jumbo lenders, their rates are higher than those offered with Fannie Mae/Freddie Mac eligible financing. Down payment requirements are usually higher too. Let’s keep the limits as they are until the housing market recovers.

Obviously, I think this is a really, really bad idea. Since when is a $729,750 house a candidate for affordable housing subsidies? These limits should never have been raised from $417,000 to begin with. The era of riskless origination must end. Fortunately, the government is not going to do this.

• Allow Special Circumstance Refinances

Many responsible people lost a job or had a major hardship due to the economy and are now perhaps able to get back on their feet. Yet, these people may be prevented from qualifying for a mortgage for many years. I’d like to see some rules written to allow consideration for those who that had a temporary setback for reasons outside of their control.

Another bogus example to lowering standards to help this guy underwrite loans to people who aren't qualified. It may be sad that people fell on hard times, but that doesn't entitle them to some special government subsidy.

• Permit Short Refinances Without layers of LLPAs

We have programs allowing underwater homeowners to refinance up to 125% of the value of their home if their loan is owned by Fannie Mae or Freddie Mac.

Those programs are a bad idea and should be eliminated. It allows lenders to push their loans most likely to go bad from strategic default onto taxpayers.

But, most lenders have imposed an “overlay” that limits these refinances to just 105% or less.

Lenders do this because they know these people will default, and if they push too many bad loans onto the GSEs, the GSEs will quit taking their loans. That's why we have loan level price adjustments.

And, there are Loan Level Price Adjustments that drive up the rate or cost due to the owner’s lack of equity. Let’s allow these homeowners to take advantage of the program designed by the government to help them take advantage of lower interest rates and payments. And, prohibit the Overlays and LLPAs mentioned above. Wouldn’t a rate reduction from say 6% to 4.5% enable many homeowners to stay rather than add their home to the inventory of future foreclosures?

Allowing borrowers to refinance into lower rates would cost the GSEs billions of dollars in revenue at a time when they are already costing taxpayers billions of dollars. The GSEs will lose less money on foreclosures than they would if they allowed everyone to refinance.

• Penalize Servicers for Taking Too Long for Loan Modifications and Short Sales

The biggest problem with Loan Mods and Short Sales is that they take too long. After waiting months and sometimes more than a year for the current servicer of a loan to approve a transaction, the buyer has given up and the seller is deeper in debt. And, the government pays a reward of $1,000 for a servicer to complete a transaction. Take away the reward and charge them a penalty for not completing or denying a request within a reasonable period of time. The reward certainly hasn’t been enough incentive to entice the servicer to complete the transaction. It will greatly speedup the process and reduce the number of homes and people in distress.

Actually, I favor this idea, but not for the reason he suggests. If there was a penalty, the denial and amend-extend-pretend would come to an end, and lenders would finally get on with the serious business of foreclosing on the delinquent mortgage squatters.

Remember the reason for the bank bailouts and the stimulus programs? It was to AVOID A FORECLOSURE CRISIS.

No. It wasn't. The bailouts were designed to mask the insolvency of our banking system, and the stimulus was designed to inject money into the system at a time when lenders could not. It was hoped lenders could earn their way back to solvency, but it is taking much longer than anyone anticipated — except us bears that understood the problem.

Did the banks that were “too big to fail” use those funds to help avoid a foreclosure crisis? No. They used those funds to get richer – not to help the people.

Yes, they did. That's why people were opposed to the bailouts to begin with. The banks should have been allowed to go down with the people who borrowed money.

And the government continues to let them impose unnecessary restrictions on homebuyers and homeowners trying to refinance.

Nonsense.

Along with jobs, housing is the key to an economic recovery. Home values must be stabilized and foreclosures must be avoided.

Wrong again. Foreclosures must be encouraged. They are the key to economic recovery.

Let’s lighten up on the unnecessary and mostly unregulated guidelines I mentioned. It won’t solve the entire problem but I think it would help millions of people without adding to this country’s deficit or the potentially growing inventory of foreclosed homes.

These dumb ideas won't solve anything, but they will help him originate some more riskless loans while temporarily inflating another housing bubble.

Richard T. Cirelli is a 35-year veteran of the mortgage industry. He is the owner of RTC Mortgage Corporation, a full-service mortgage company based in Laguna Beach. He is a Certified Mortgage Planning Specialist. RTC Mortgage offers all types of residential and commercial real estate financing. Contact him at 949.494.4701 or Rick@RTCmortgage.com. Visit www.rtcmortgage.com.

I think its fair to say, I strongly disagree with this man's ideas.

A profit from early an 2008 sale?

When I saw today's featured property on the MLS, it seemed familiar. I profiled it back in late 2007 when the current owner bought it. As always, the old comments are an interesting look into the view of market participants back in 2007. We had blog tolls back then too.

Back in November of 2007, this property was listed for $620,000. The property records say they paid $520,000, but the price is unconfirmed. If they managed to negotiate $100,000 off the asking price, they are pretty savvy. I suspect they paid more. In either case, they only borrowed $416,000 originally, and they refinanced for $417,000 in 2009, so this is not a distressed sale.

——————————————————————————————————————————————-

This property is available for sale via the MLS.

Please contact Shevy Akason, #01836707

949.769.1599

sales@idealhomebrokers.com

Irvine House Address … 9 OAKDALE Irvine, CA 92604

Resale House Price …… $595,000

Beds: 3

Baths: 2

Sq. Ft.: 1440

$413/SF

Property Type: Residential, Single Family

Style: One Level, Contemporary

Year Built: 1977

Community: 0

County: Orange

MLS#: S666592

Source: SoCalMLS

Status: Active

——————————————————————————

Here is the one-story, single-family detached home you've been looking for in Woodbridge! Cathedral ceilings and designer colors greet you as you enter this charming 3-bedroom home. Step down into the formal living room awash with natural light streaming in from the many dual-pane upgraded, energy saving windows. The cozy dining area with its tasteful chandelier and tile floor connects the living room and galley-style kitchen that features expansive, decorator tile countertops and plenty of cabinet storage. A gorgeous master suite includes a large bathroom with dual-sink vanity. Relax with family and friends in the comfortable wraparound backyard while a private patio serves one of the secondary bedrooms. Central air conditioning plus ceiling fans with handheld remote controls in all bedrooms and the living room insure your summer time comfort while saving energy. Highly-rated Irvine schools. * * * LOW HOA DUES * * * NO MELLO ROOS * * * STANDARD EQUITY SALE * * * NOT A SHORT SALE * * *

——————————————————————————————————————————————-

Proprietary IHB commentary and analysis ![]()

Resale Home Price …… $595,000

House Purchase Price … $520,000

House Purchase Date …. 1/25/2008

Net Gain (Loss) ………. $39,300

Percent Change ………. 7.6%

Annual Appreciation … 3.9%

Cost of Home Ownership

————————————————-

$595,000 ………. Asking Price

$119,000 ………. 20% Down Conventional

4.48% …………… Mortgage Interest Rate

$476,000 ………. 30-Year Mortgage

$103,122 ………. Income Requirement

$2,406 ………. Monthly Mortgage Payment

$516 ………. Property Tax (@1.04%)

$0 ………. Special Taxes and Levies (Mello Roos)

$124 ………. Homeowners Insurance (@ 0.25%)

$0 ………. Private Mortgage Insurance

$82 ………. Homeowners Association Fees

============================================

$3,128 ………. Monthly Cash Outlays

-$401 ………. Tax Savings (% of Interest and Property Tax)

-$629 ………. Equity Hidden in Payment (Amortization)

$197 ………. Lost Income to Down Payment (net of taxes)

$94 ………. Maintenance and Replacement Reserves

============================================

$2,389 ………. Monthly Cost of Ownership

Cash Acquisition Demands

——————————————————————————

$5,950 ………. Furnishing and Move In @1%

$5,950 ………. Closing Costs @1%

$4,760 ………… Interest Points @1% of Loan

$119,000 ………. Down Payment

============================================

$135,660 ………. Total Cash Costs

$36,600 ………… Emergency Cash Reserves

============================================

$172,260 ………. Total Savings Needed

—————————————————————————-

FAMILY ROOM WITH WET-BAR THAT OVERLOOKS A $500,000, RESORT STYLE PALM TREE STUDDED POOL FEATURING A HUGE ROCK SLIDE AS WELL AS A 5 SEAT SWIM UP BAR. THIS HOME TRULY IS AN ENTERTAINERS DELIGHT WITH ITS OWN OUTDOOR KITCHEN INCLUDING A BUILT IN BARBEQUE, MINI FRIDGE AND RECESSED GROTTO WITH TV AND FULL BATH. THE POOL AREA ALSO FEATURES BUILT IN GAS AMBIENT HEATERS AS WELL AS A ROUND FIREPIT WITH SEATING. THIS HOME IS A MUST-SEE WITH TOO MANY UPGRADES TO LIST!! THE ESTATE IS FEATURED ON BRAVO'S HIT TELEVISION SHOW, 'THE REAL HOUSEWIVES OF ORANGE COUNTY. ' THIS HOME SHOWS WELL AND WILL SELL FAST!

FAMILY ROOM WITH WET-BAR THAT OVERLOOKS A $500,000, RESORT STYLE PALM TREE STUDDED POOL FEATURING A HUGE ROCK SLIDE AS WELL AS A 5 SEAT SWIM UP BAR. THIS HOME TRULY IS AN ENTERTAINERS DELIGHT WITH ITS OWN OUTDOOR KITCHEN INCLUDING A BUILT IN BARBEQUE, MINI FRIDGE AND RECESSED GROTTO WITH TV AND FULL BATH. THE POOL AREA ALSO FEATURES BUILT IN GAS AMBIENT HEATERS AS WELL AS A ROUND FIREPIT WITH SEATING. THIS HOME IS A MUST-SEE WITH TOO MANY UPGRADES TO LIST!! THE ESTATE IS FEATURED ON BRAVO'S HIT TELEVISION SHOW, 'THE REAL HOUSEWIVES OF ORANGE COUNTY. ' THIS HOME SHOWS WELL AND WILL SELL FAST!

.png)

.jpg)

.png)

.jpg)