New faces in the political landscape will decide the fate of Fannie Mae and Freddie Mac.

Irvine Home Address … 24 BULL Run Irvine, CA 92620

Resale Home Price …… $749,900

The Broken clock is a comfort

It helps me sleep tonight

Maybe it can stop tomorrow

From stealing all my time

And I am here still waiting

Though I still have my doubts

I am damaged at best

Like you've already figured out

Lifehouse — Broken

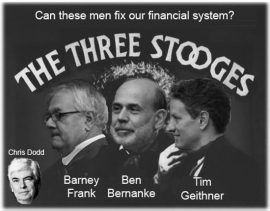

Back in 2009, I posed the question: Who will fix the System? The balance of power in Washington shifted in the last election. A new debate over the future of the GSEs and the housing market is just beginning. Let's take a fresh look at the gentlemen who will be deciding the fate of the housing market.

Obviously, those guys didn't get it done. Who's next?

Factbox: Key players in the debate on housing finance

Wed Jan 5, 2011 4:31pm EST — Reporting by Corbett B. Daly; Editing by Leslie Adler

{To avoid giving you pages of italics to read, the remainder is from the article}

(Reuters) – The Obama administration is set to unveil its proposal for an overhauled system of U.S. housing finance by the end of this month.

The administration's plan will just be a starting point. Congress is expected to debate the issue thoroughly before making changes to the current system, centered around ailing mortgage finance giants Fannie Mae and Freddie Mac.

Differing views on the merits of the current system among Republican and Democrats suggest the debate will be lively.

The following is a list of some of the key players in the debate:

U.S. Treasury Secretary Timothy Geithner:

Geithner, a former president of the New York Federal Reserve Bank, played a key role orchestrating bank bailouts during the financial crisis

He also was instrumental in the administration's push for sweeping Wall Street reforms last year, which did not address Fannie Mae and Freddie Mac. The mortgage finance companies have received more than $150 billion in direct taxpayer support since being placed in a government conservatorship in 2008.

At an event on the future of housing finance last August, Geithner sketched out some basic tenets of the administration's likely approach, but offered no details.

“It is not tenable to leave in place the system we have today. We will not support returning Fannie and Freddie to the role they played before conservatorship, where they fought to take market share from private competitors while enjoying the privilege of government support,” he said.

“I believe there is a strong case to be made for a carefully designed guarantee in a reformed system with the objective of providing a measure of stability in access to mortgage finance even in future economic downturns.”

Treasury Undersecretary Jeffrey Goldstein:

Goldstein is a former private equity executive tasked with being the administration's liaison to Wall Street. Goldstein has kept a low profile since taking office in 2010, though housing finance reform is expected to be a key component of his portfolio. In a July blog post on the White House website, Goldstein stressed “the vital importance” of the housing market to “our country's future,” but steered clear of any specifics.

Federal Housing Administration Commissioner David Stevens:

Stevens is a former executive with Long and Foster, the largest independently held residential real estate company in the United States, and has worked in top positions at Wells Fargo and Freddie Mac. Stevens is credited with shoring up the finances of the FHA by hiring the agency's first chief risk officer and tightening lending standards. Loans backed by the FHA account for close to 20 percent of new mortgage originations. Stevens wants to reduce the FHA's role in the mortgage market from those elevated levels.

Treasury counselor Gene Sperling

Sperling is currently a counselor to Geithner, but is in the running to be named as President Barack Obama's chief White House economic adviser, a post he held in the 1990s under President Bill Clinton. Sperling is known as a capable coordinator for economic policy. He spent a significant amount of his time at Treasury on initiatives aimed at boosting small business lending, though the programs had limited success.

House Financial Services Committee Chairman Spencer Bachus:

The soft-spoken Alabama Republican is quite a change, in both style and substance, from his predecessor, the outspoken liberal Barney Frank. Bachus believes the United States needs to be weaned from its reliance on government funding of mortgages. “What we now have is an addiction to government funding of mortgages,” Bachus told Reuters late last year. He has also said the two firms should be in “liquidation,” not “conservatorship.”

House Republican Conference Chairman Jeb Hensarling:

Hensarling, from Texas, is a conservative Republican who has been a vocal critic not only of Fannie Mae and Freddie Mac, but of any government support for the U.S. housing market. He holds the No. 4 Republican leadership post in the House of Representatives.

“Fannie and Freddie were not born of a competitive marketplace, but in a government laboratory. They were allowed to exploit their implicit government guarantee to take on enormous risks. These two entities expose the taxpayer to unlimited risk and will likely end up receiving the mother of all bailouts,” Hensarling said in a statement on his website.

Rep. Scott Garrett, chairman of the House Financial Services subcommittee on capital markets and government-sponsored enterprises:

Garrett, a New Jersey conservative Republican, this year takes the helm of the subcommittee responsible for oversight of Fannie Mae and Freddie Mac. He wants to wind down the firms within two years, a more radical position than even many of his Republican colleagues hold.

Senate Banking Committee Chairman Tim Johnson:

The Democratic lawyer from bank-friendly South Dakota is more conservative than his predecessor, Christopher Dodd, who retired last year. Johnson underwent brain surgery in 2006 and came away healthy, but with impeded speech. He has recovered and was present through the all-night talks leading to passage of the Dodd-Frank revamp of Wall Street regulation. Johnson is expected to take a go-slow approach to Fannie Mae and Freddie Mac, holding a number of hearings to gain a thorough understanding of their complexity before putting forth any specific Senate proposals. Keywords: USA HOUSING/PLAYERS

Senate Banking Committee top Republican Richard Shelby:

Another conservative Republican, Shelby has been a vocal critic of Fannie Mae and Freddie Mac. Late last year, he blocked Obama's pick to be the regulator of the two government-sponsored enterprises. Shelby accused the nominee, North Carolina's commissioner of banks, Joseph Smith, of being a “tool” of the Obama administration who would throw government money at the mortgage market and send the bill to taxpayers.

Fannie, Freddie acting regulator Edward DeMarco:

DeMarco is a career civil servant who has been acting director of the Federal Housing Finance Agency since August 2009. He had been expected to be replaced by Smith, but with the nomination blocked, he could stay in the acting role for some time. DeMarco is very focused on limiting taxpayer losses from Fannie Mae and Freddie Mac and has the power to exert substantial influence over how the two firms conduct their business.

House Financial Services Committee top Democrat Barney Frank:

Frank, a key architect of the financial regulation law that bears his name, lost the gavel of the House Financial Services Committee when Republicans took control of the House. However, as the panel's top Democrat on the key House committee responsible for Fannie Mae and Freddie Mac, he is likely to still wield considerable influence. He is a key ally of the Obama administration.

Frank has said the GSEs should be “abolished” in “current form” and a new housing finance system should be created. At the same time, he has stressed the importance of developing a new system before shutting the two firms down. “You can't really tear down the old jail until you've built the new one,” he has said.

{End of article}

I know this stuff is a bit wonkish, but it is good information to know. We will see these guys pontificate in debates over the next 18 months on the fate of the GSEs. Don't underestimate the importance of the GSEs to the housing market. Most middle-class mortgages are GSE insured. High wage earners often borrow from a jumbo loan lender because their loans exceed the $729,750 loan limit at the GSEs and FHA.

I know this stuff is a bit wonkish, but it is good information to know. We will see these guys pontificate in debates over the next 18 months on the fate of the GSEs. Don't underestimate the importance of the GSEs to the housing market. Most middle-class mortgages are GSE insured. High wage earners often borrow from a jumbo loan lender because their loans exceed the $729,750 loan limit at the GSEs and FHA.

Whatever happens to the GSEs matters to Irvine.

If they are dismantled, and if the home mortgage interest deduction is scaled back, the cost of borrowing will rise and the amounts borrowed will go down. That will put continued pressures on pricing. House price increases require greater borrowing, and with interest rates and other costs working against borrowing, house prices will likely stagnate for a very long time as these subsidies unwind.

Japan had more than 20 years of real estate deflation. What if we had 20 years of real estate stagnation?

Don't worry. We will probably print enough money to create all kinds of inflation including wage inflation. That will put house prices back on a steady upward march in 2 to 5 years. Hopefully, in order to save house prices, you aren't paying $14 per gallon for gas and gold is selling for $3,200 an ounce. My guess is Bernanke will error on the side of over-printing.

It was a great bull run

I do feel a hint of jealousy when I see homeowners like today's. They bought at the bottom of the last real estate recession on 7/31/1997 and paid $283,000 for this house. They borrowed $226,400. A few months later they borrowed $28,000 of their equity, probably to do some necessary renovations. On 9/10/2001 they had $247,000 in debt in a new first mortgage. The refinanced two more times, but the final mortgage is for $238,500 which puts them near their entry point.

They did not borrow anything extra when given plenty of opportunities.

Great job.

I can't give them an A because their mortgage balance is larger than when they started. I am giving them a B instead of a C because I believe the increase was a modest renovation cost. After their mortgage increased initially, it went downward to where it is now.

When they sell this house at bubblish prices, they stand to get a check from escrow for nearly $450,000.

Wouldn't that be a cool check to cash?

These owners obtained significant wealth advantage from fortuitous timing in the housing market. They missed the peak for maximum sale, but with their diligence to pay down the mortgage and the huge run up in prices, they get the pot of gold.

We have seen plenty go the other way….

They passed on all temptations and diligently paid down their mortgage at a time when everyone else was seeking ways to maximize borrowing to obtain free money to spend.

How did they do it?

Irvine Home Address … 24 BULL Run Irvine, CA 92620 ![]()

Resale Home Price … $749,900

Home Purchase Price … $255,000

Home Purchase Date …. 9/10/1993

Net Gain (Loss) ………. $449,906

Percent Change ………. 176.4%

Annual Appreciation … 6.2%

Cost of Ownership

————————————————-

$749,900 ………. Asking Price

$149,980 ………. 20% Down Conventional

4.86% …………… Mortgage Interest Rate

$599,920 ………. 30-Year Mortgage

$152,809 ………. Income Requirement

$3,169 ………. Monthly Mortgage Payment

$650 ………. Property Tax

$0 ………. Special Taxes and Levies (Mello Roos)

$125 ………. Homeowners Insurance

$0 ………. Homeowners Association Fees

============================================

$3,944 ………. Monthly Cash Outlays

-$770 ………. Tax Savings (% of Interest and Property Tax)

-$740 ………. Equity Hidden in Payment

$280 ………. Lost Income to Down Payment (net of taxes)

$94 ………. Maintenance and Replacement Reserves

============================================

$2,808 ………. Monthly Cost of Ownership

Cash Acquisition Demands

——————————————————————————

$7,499 ………. Furnishing and Move In @1%

$7,499 ………. Closing Costs @1%

$5,999 ………… Interest Points @1% of Loan

$149,980 ………. Down Payment

============================================

$170,977 ………. Total Cash Costs

$43,000 ………… Emergency Cash Reserves

============================================

$213,977 ………. Total Savings Needed

Property Details for 24 BULL Run Irvine, CA 92620

——————————————————————————

Beds: 4

Baths: 1 full 2 part baths

Home size: 2,190 sq ft

($342 / sq ft)

Lot Size: 5,400 sq ft

Year Built: 1979

Days on Market: 7

Listing Updated: 40546

MLS Number: S642830

Property Type: Single Family, Residential

Community: Northwood

Tract: Ch

——————————————————————————

AWESOME REMODEL….NO STONE LEFT UNTURNED! Walk into this home and feel the rich, warm welcome! Remodel just completed includes gourmet kitchen with granite counters, rich, dark wood cabinetry, gas cooktop, electric oven, microwave/convection oven and roll out center island. All baths have been remodeled with granite counters, new sinks, faucets, lighting, etc. Walk behind wet bar in family room for entertaining features granite counter too. Great floorplan with breakfast nook and large family room off of kitchen. Rich wood and tile floors, chair rails, crown molding, wainscotting, custom paint and more. Master bedroom has walls of bookshelves and storage space with walk in closet, master bathroom with granite counters, double sinks and more. Very private backyard with tons of color, potting shed, patio area AND secluded spa with sitting area. All of this and Northwood High School too!!!

I hope you have enjoyed this week, and thank you for reading the Irvine Housing Blog: astutely observing the Irvine home market and combating California Kool-Aid since 2006.

Have a great weekend,

Irvine Renter

They probably have paid down their mortagage since the $238 refi so they may still be an A. I’d give them an A- or B+.

It is nice to see owners like this. Now the question is…what will they do with the check? Do they rent for a couple of years and get 1.6% on the cash? Do they move out of state?

Is it me, or does the front of that house look like a locomotive?

LOL! that’s too cool.

The average 30-year fixed-rate mortgage fell to 4.71% in the week ended Jan. 13, reaching a four-week low, Freddie Mac said. The rate was 4.77% in the prior week and 5.06% in the prior year, according to Freddie Mac, a buyer of residential mortgages.

—–

OMG..what is happening?

I was bet my entire down payment I rolled over from selling from bubble height days on TBT (Ultra bear of treasuries) because awgee and others guaranteed rates are going up and only up based on his thorough economic analysis.

He was so convincing that 4% rates are gone forever since he was posting daily about how rates were going up….

Now a big chunk of the down payment I had ponzi’ed from selling my house during the peak is gone and I don’t know what to do since there isn’t any possible way I can save up for a down payment even though my wife and I are both professionals and each make 6 figure incomes.

Help awgee! can you please explain why rates are going down again? how is this possible? The Chinese were supposed to only buy commodities.

so_scared.

———

Per DataQuick, Single-Family Median Home Price:

2010 Monthly/Weekly

$490,000 = Jan

$490,000 = Feb

$515,000 = Mar

$505,000 = Apr

$515,000 = May

$515,000 = Jun

$517,500 = Jul

$530,000 = Aug

$525,000 = Sep

$500,000 = Oct

$500,000 = Nov

$480,000 = Dec 22 <-Today's median (LoL) FAIL! “You will continue to be wrong as long as you look at the possibilities through the lens of desire rather than the harshness of reality.” ~ AWGEE

Dude – The last thing I said about interest rates was that they would be going down first. The chinese are not buying T’s. The Fed is.

A number of people here including AZDave ripped PR last month when there was a slight uptick in rates.

The continuous improvement in the credit markets and low borrowing rates still drive demand in Irvine.

PR’s been right all along.

It’s amazing how the vast majority here cherry pick based on their desires instead of acknowledging the facts.

I know, I know the banks are scared to death and Lee can bold that it’s going to be a very interesting week

This whole Irvine housing crash continues to be a freaking yawner. Wall $treet Won, I’d rather deal with that reality then have BS hope for something else.

If I’ve learned anything from this blog it’s that when IR says something can’t happen it usually happens:

IR: the government can’t influence housing prices

Yeah well it happened, and the BS continues

IR: interest rates are heading up

Yeah well the opposite continues

IR: prices have been going down since 2008/9 in Irvine

Yeah well the opposite happened

IR: foreclosure contract law does not apply to deadbeats

Wrong again

Next up is probably cram downs and sleu of other things that can never happen

It seems that every recent buyer is counting on the Fed to save their investment. I for one hope you are right but something deeper tells me you are wrong especially when the big players are free and clear of their bad debt, the little guys will get screwed.

Of course the little guys will get screwed, that’s how the game is set up. However nobody will get screwed more than those who were responsible.

PR is starting to sound like mark hanson ( that is pretty good company) on the cram downs. If the crisis and follow on response has taught us anything it is that the government will go to extraordinary lengths to reverse market forces, and wields power.

Planet Reality has acknowledged many times that he/she doesn’t own a home in Irvine. So is Planet Reality a renter?

You have way too much faith in the Fed. From the last two decades they have proven to be an absolute abysmal FAILURE. Sooner or later all this stupidity will catch up with them…and I think it will be sooner.

On another topic, I have no desire to purchase in Irvine for many reasons. However, I have noticed that many houses in Huntington Beach (the area that I follow) are seeing steep discounts. What was selling for high 6XX and low 7XX K at the peak are now being advertised with a number that starts with 4. Keep on dropping baby!

“From the last two decades they have proven to be an absolute abysmal FAILURE.”

That all depends on what the Fed’s goal was.

What do you think the Fed’s purpose is?

One of the Feds major goals, though not published, is to produce inflation disguised as real growth. The Fed has been pretty sucessful at that.

Every time I hear an inflation number reported without food or energy cost I have to laugh. Only the two most important expenses, excluding housing and education which also have not been included in the CPI for the past 20 years.

Inflation numbers that don’t have food and energy? No seriously, are they for real?

Awgee, I see the Fed’s purpose as making the tough (often unpopular) economic decisions that will keep our country financially healthy. These decisions should be completely devoid of politics and not catering to banks, Wall St., corporate America. If economy needs stimulation or if it needs to be cooled, they can act with interest rate adjustments. Additionally, their job is to spot bubbles of any type and hopefully take the air out of them…which will be far less painful than having them run their course.

We have seen the last two idiots have been nothing but a bunch lap dogs for politicans and the crony Wall St. bankers. Massive bubbles have formed on their watch and wreaked havoc with the world economy. Their interest rate policy is reckless, it caters to the irresponsible and not the responsible savers. History will show that Alan and Ben were complete buffoons.

Abolish the Fed.

The job of the Fed is to do what the designers of the Fed intended it to do, enrich and empower the member banks. The legislation to create the Federal Reserve was written by bankers and was intended to enrich banks.

The easiest way to figure out anybody’s intention is to look at what they have done. What has the Fed done in its 97 year history? If that is too long to research, what has the Fed done in the last 10 years?

You will know them by their deeds.

PR,

Why allow the facts to get in the way of a HOPEful story on how inflation is remaining surprisingly low and that we should all feel wonderful about our economy and that pesky food and energy thing is really nothing to worry about.

PR: “Every time I hear an inflation number reported without food or energy cost I have to laugh. Only the two most important expenses, excluding housing and education which also have not been included in the CPI for the past 20 years.”

How many times must we go over this? Food and energy costs are not included in SHORT-TERM inflation stats due to their volatility, not due to their unimportance. Food and energy costs are ALWAYS included in longer-term inflation reporting, such as annual or multi-year inflation stats.

-Darth

Irinve is not Chicago:

http://www.chicagotribune.com/classified/realestate/foreclosure/ct-biz-0113-walkaway–20110113,0,515928,full.story

Borrower walk away. Now bank walk away.

Recession has “ended” for the business, but what happens when the business have little buyers in America? …sell overseas.

New folks in control, but is it new in name only and still under the thumb of GS?

You link Goes Nowhere and Does Nothing.

Hmmmm…

So they are all Zionist Jews with duel citizenship with Israel? Oh, wait… Israel is owned by the Zionist Rothschilds, who have 600 Trillion Dollars, own all of the banks and Associated Press and Reuters News service. I wonder…are these guys own by them too?!!

Who let the cat out of the bag?

My best friend is a Jew and a business lawyer. I’ve known him for over 25 years. He works his ass off, and he’s brilliant … NOTHING has been given to him. He learned this work ethic from his mother and father (Jews), and he is teaching it to his children.

That’s the secret of the Jews prosperity/cat.

People who think like this are why I will never take the Ron Paul crowd seriously.

-Darth

Since we’ve now got a conspiracy theorist in our midst that is determined to dump the housing boom/bust on “Tha Joos!”, here’s an article for your reading enjoyment:

Book Details German Citizens’ Role in End of War Killings

“The more the war approached its end, and the more obvious the prisoners’ presence in the midst of the German population became, the more regularly German civilians participated.”

http://www.spiegel.de/international/germany/0,1518,739518,00.html

Don’t ever, EVER, EVER forget what road people like this poster would have us walk down.

-Darth

P.S. My wife is a German citizen. My personal ancestry is heavily German. So far as I’m aware, I have no Jewish heritage whatsoever. If there were any room for equivocation on this issue, I would have as much reason as anyone.

Now the the Dems no longer control the house I doubt that Mr Frank will continue to wield as much influnce as you suggest. Plus, I think he’s feeling a bit guilty over the housing bubble which he realizes he’s partly responsible because of his past policies.

Your first sentence I mostly agree with, although Barney Frank has a particular knack for wielding influence, even from the minority.

Your second sentence, I don’t believe is true at all.

-Darth

P.S. Untrue as to the feeling guilty part, that is. He most certainly is and was guilty, but I doubt that he admits it even to himself, and I definitely don’t think he feels that his actions were negative in any way. I’m certain that he has managed to blame any and every one else.

-Darth

I’m glad IR profiled a non-Ponzi home this time. It shows that Irvine is not the “epicenter” of HELOC abuse that some think it is.

I actually believe there is less HELOC-fu in Irvine than there are in other OC cities but I don’t have the data to prove it.

Maybe this is one of those people who will use their equity profit to put a large down payment on another Irvine house.

I think they are more likely to buy AZdavids dream home in Scottsdale for $300K cash.

You are likely to be correct. I noticed that most Irvinians are driving typical cars for their income or occupation, while many other OC’er are driving more high end cars especially considering their occupation. But the HELOC siren is hard to resist.

http://www.calculatedriskblog.com/2011/01/fomc-debates-housing-bubble-in-2005.html

Hoocoodanode? The Fed!

Why has it taken 5 years to get this information made public? I don’t agree with Ron Paul about much, but if he can get the minutes of the FOMC down to maybe 3-6 month lag before they’re made public, that would be a positive step.