An academic debate over the causes and the expansion of housing bubbles.

Irvine Home Address … 139 STANFORD Ct 38 Irvine, CA 92612

Resale Home Price …… $462,000

If you start me up

If you start me up I'll never stop

If you start me up

If you start me up I'll never stop

Ride like the wind at double speed

I'll take you places that you've never, never seen

If you start it up

Love the day when we will never stop, never stop

Never, never, never stop

Tough me up

Never stop, never stop

The Rolling Stones — Start Me Up

Over the last couple of years, a few academics have been making the case that land-use regulation is the cause of the housing bubble. Most of the post that follows summarizes their argument.

I think they are only partially correct. Land use regulations do restrict supply, and therefore they do impact prices. As I noted in The Great Housing Bubble:

Speculative bubbles are caused by precipitating factors.[1] Like a spark igniting a flame, a precipitating factor serves as a catalyst to begin the initial price increases that change the psychology of market participants and activates the beliefs listed above. There is usually no single factor but rather a combination of factors that stimulates prices to begin a speculative mania. The Great Housing Bubble was precipitated by innovation in structured finance and the expansion of the secondary mortgage market, the lowering of lending standards and the growth of subprime lending, and to a lesser degree the lowering of the Federal Funds Rate.

Supply shortages caused by land use regulations can cause short-term volatility in prices. The perception of a chronic real estate supply shortage in California helps sustain prices at the high levels of income debt support. The initial price rally caused by the shortage can serve as the precipitating factor causing the irrational exuberance to take over. It is the irrational exuberance and creative financing that causes the housing bubble.

So when these academics proclaim that land use regulations cause housing bubbles, they are as correct as saying matches cause forest fires. The match may start the flame, but the flame consumes the forest for a variety of other reasons not explained by the initial spark. Similarly, housing bubbles may be precipitated by a supply shortage causing a price rally, but it is the irrational exuberance of buyers thinking prices will go up forever that gives housing bubbles their strength. The full rise and fall of bubble pricing is not explained by the supply shortage alone.

The Truth About the U.S. Housing Market

Leith van Onselen — January 06, 2011

The Unspoken Truth

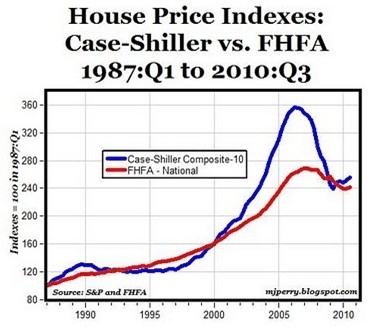

As bad as last week's housing data was, the 20 cities that comprise the Case-Shiller Composite Index are not representative of the entire United States housing market. In fact, the United States housing bubble/bust was confined to only a minority of cities. To illustrate this point, first consider the below chart (courtesy of Carpe Diem), which compares the 10-City Case-Shiller Composite Index against the FHFA House Price Index based on 50 states:

As you can see, the United States housing bubble/bust was confined, to a large extent, to the 10 cities making up the Case-Shiller 10-City Composite Index: Boston, Chicago, Denver, Las Vegas, Los Angeles, Miami, New York City, San Diego, San Francisco, and Washington, D.C.

So why was there so much variability in house price performance between United States cities, with some cities booming then busting while other cities remained relatively stable? It certainly wasn't due to liberal lending policies (easy credit), since essentially the same lending conditions were available across the United States. It wasn't because of differences in population growth, since states like Texas, which has experienced the highest population growth over the past 10 years, never had a housing bubble/bust. Rather, the differences in house price performance are accounted for by the way in which these markets regulate land use.

No. His conclusions are completely wrong. The key difference that made Texas stand out was not its less restrictive land use, it was the difference in laws pertaining to HELOCs and cash-out refinancing. Read my detailed argument here: Desire for Mortgage Equity Withdrawal Inflated the Housing Bubble.

The below table, which comes from Demographia's 6th Annual International Housing Affordability Survey, shows the extent to which the various housing markets employ restrictive land use regulations.

Restrictive land use regulation, often referred to as “smart growth,” “growth management,” or “new urbanism,” refers to policies that force people to live in higher densities while significantly restricting the expansion of suburban residential development. Measures include, but are not limited to, urban growth boundaries, areas declared off-limits to development, building moratoria, development fees and charges, and excessively large minimum lot sizes.

These academics are making themselves correct by how they define “restrictive” land use. The devil is in the details and the definitions. How should we compare the land use regulations of Texas and California? How do we determine if one place is restrictive and another permissive? How much of the data is subjective evaluations of regulatory effects subject to a wide degree of interpretation?

The data gathered by these researchers presented in different forms all boil down to the same subjective evaluations of land use regulations. If you agree with their assessment, then you will agree with their conclusions.

Cities that have adopted liberal market-based approaches (“more responsive land regulation”) have experienced relatively stable housing markets, whereas those that have implemented prescriptive land use regulations have experienced volatile boom/bust cycles.

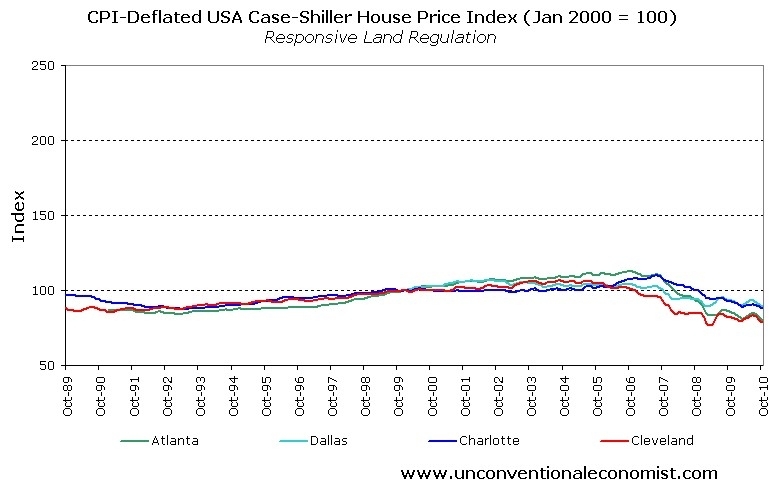

To illustrate this point, first consider the below chart, which plots the CPI-adjusted house price performance of the cities included in the 20-City Case-Shiller Composite index and deemed by Demographia as having “more prescriptive land regulations.”

As you can see, prices have been highly volatile, with all cities experiencing wild boom/bust conditions.

Now consider prices in the cities within the 20-City Case-Shiller Composite Index with “more responsive land regulations.”

As you can see, real house prices have remained relatively stable in the supply-responsive cities.

The situation is similar at the state level using FHFA housing data. First, consider the states with “more prescriptive land regulations”:

Now consider states with “more responsive land regulations”:

Again, it's the same story, with the highly regulated states experiencing wild boom/bust cycles whilst prices in the market-oriented states remained relatively stable.

If you accept their methods of classifying land use regulations, then you will agree with their findings. If not, you won't. Garbage in, garbage out.

Economics 101

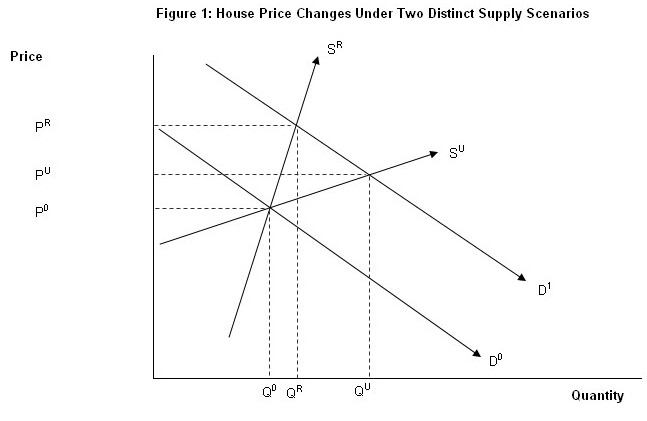

The economic forces underpinning the above findings are perhaps best explained through basic supply and demand analysis. Consider the below chart taken from an earlier article on this issue.

Q0 and P0 represent the initial equilibrium situation in the housing market. Initial demand is provided by D0, whereas supply is shown as either SR (restricted) or SU (unrestricted), depending on whether land supply constraints exist.

Following an increase in demand, such as that brought about by a significant relaxation of lending standards, the demand curve shifts outwards from D0 to D1. When land supply is restricted, house prices rise sharply from P0 to PR. By contrast, when supply is unrestricted, prices rise more gradually from P0 to PU.

The situation works the same way in reverse. For example, if there was a sharp fall in demand following a contraction in credit availability or a sharp rise in unemployment, causing demand to fall from D1 to D0, then prices fall much further when land supply is constrained.

The key point is that increases (declines) in demand can bring sharply rising (falling) house prices when supply is constrained. However, when land supply is not regulated, it adjusts to demand and house price volatility is reduced.

The effect on markets in the short term is how they describe above. However, that only explains the first stages of a market rally. Once prices are high, and they have been rising long enough for people to take interest, the market needs help in order to keep going higher. It is financial innovation folly that must take over to build a significant real estate bubble.

These observations are consistent with those of Glaeser and Gyourko, who summarised the findings of a number of studies in this area:

Recent research also indicates that house prices are more volatile, not just higher, in tightly regulated markets …. price bubbles are more likely to form in tightly regulated places, because the inelastic supply conditions that are created in part from strict local land-use regulation are an important factor in supporting ever larger price increases whenever demand is increasing.

…. It is more difficult for house prices to become too disconnected from their fundamental production costs in lightly regulated markets because significant new supply quickly dampens prices, thereby busting any illusions market participants might have about the potential for ever larger price increases.

Learning history's lessons

As long as commentators focus primarily on the demand side of the housing market, whilst ignoring supply-side constraints, they will never fully understand the drivers of housing bubbles and busts. The resulting incorrect diagnosis will inevitably lead to poor policy prescriptions and outcomes.

By all means, let's crack down on the destructive speculation, predatory financing and financial alchemy that have fuelled the world's housing bubbles. At the same time, let's not ignore the supply-side barriers that have enabled the credit-fuelled demand to feed into skyrocketing house prices which, in the case of the United States, later collapsed once the artificial demand evaporated.

Readers seeking detailed information on issues pertaining to the supply-side of the housing market are encouraged to visit the Demographia and Performance Urban Planning websites. Also, please be advised that the 7th Annual Demograhia International Housing Affordability Survey will be released on 24 January 2011. It's sure to be another great read.

Having worked most of my career in the land development industry, I understand the desire to reduce land use regulations which hinder our ability to deliver housing. When we can't deliver housing, there are shortages and short-term price rallies. However, much of our land use regulation is good and should not be abandoned, and the likelihood of the regulations rolling back to some more permissive era is slim to none.

How to ruin a good cashflow investment with excessive borrowing

There was a time when banks were smarter about loaning money on cashflow properties. Besides an appraisal showing comparable sales, a process prone to bouts of irrational exuberance, lenders on rental properties also look at stabilized cashflow to determine if the cashflow from the property can cover the loan payments in the event of foreclosure.

During the Great Housing Bubble, lenders did not bother to check actual cashflow. During the savings and loan disaster, developers had to make up rosy financial projections to demonstrate income in order to get lenders to approve the loan. During the bubble, since lenders thought they were passing the risk on to others in mortgage-backed securities, lenders did not care about whether or not the cashflow covered the income.

At some point after this property was purchased and before the owner went Ponzi, rents rose enough to make this property cashflow positive. By 2002, this was finally a profitable rental. At least until the owner started his borrowing spree which culminated in a $450,000 ARM.

The owner quit paying the ARM in mid 2008, and he is probably still skimming rent from whoever lives there.

Foreclosure Record

Recording Date: 01/05/2010

Document Type: Notice of Sale

Foreclosure Record

Recording Date: 12/15/2008

Document Type: Notice of Sale

Foreclosure Record

Recording Date: 09/05/2008

Document Type: Notice of Default

Irvine Home Address … 139 STANFORD Ct 38 Irvine, CA 92612 ![]()

Resale Home Price … $462,000

Home Purchase Price … $275,500

Home Purchase Date …. 11/3/1992

Net Gain (Loss) ………. $158,780

Percent Change ………. 57.6%

Annual Appreciation … 2.8%

Cost of Ownership

————————————————-

$462,000 ………. Asking Price

$16,170 ………. 3.5% Down FHA Financing

4.86% …………… Mortgage Interest Rate

$445,830 ………. 30-Year Mortgage

$94,143 ………. Income Requirement

$2,355 ………. Monthly Mortgage Payment

$400 ………. Property Tax

$0 ………. Special Taxes and Levies (Mello Roos)

$77 ………. Homeowners Insurance

$300 ………. Homeowners Association Fees

============================================

$3,133 ………. Monthly Cash Outlays

-$386 ………. Tax Savings (% of Interest and Property Tax)

-$550 ………. Equity Hidden in Payment

$30 ………. Lost Income to Down Payment (net of taxes)

$58 ………. Maintenance and Replacement Reserves

============================================

$2,285 ………. Monthly Cost of Ownership

Cash Acquisition Demands

——————————————————————————

$4,620 ………. Furnishing and Move In @1%

$4,620 ………. Closing Costs @1%

$4,458 ………… Interest Points @1% of Loan

$16,170 ………. Down Payment

============================================

$29,868 ………. Total Cash Costs

$35,000 ………… Emergency Cash Reserves

============================================

$64,868 ………. Total Savings Needed

Property Details for 139 STANFORD Ct 38 Irvine, CA 92612

——————————————————————————

Beds: 3

Baths: 3 baths

Home size: 1,354 sq ft

($341 / sq ft)

Lot Size: n/a

Year Built: 1985

Days on Market: 4

Listing Updated: 40547

MLS Number: 11498103

Property Type: Townhouse, Residential

Community: West Irvine

Tract: Ws1

——————————————————————————

According to the listing agent, this listing may be a pre-foreclosure or short sale.

This is an Approved Shortsale at $462,000 (was appraised at this price 2 weeks ago)we have until the 20th of January to close we wont accept anything less then $462,000, This is a Beautiful 3+3 Townhome, w one car garage and one covered carport.Last time we had 4 offers in 2 days, Previous Buyer paid for inspection an appraisel last minute decided to stay over sea's and not move to the U.SWe might need to use their lender since they have all paperwork and can close in 12 days approx. to make an offer or any questions please look at privete remarks.

we wont accept anything less then $462,000? Don't hold your breath waiting for my offer of $461,500.

Last time we had 4 offers in 2 days. Wow! What a great realtor….

There is also the idea of how an area is described. Miami might have smart-growth land restrictions, but I doubt they apply to its suburbs like West Kendall, or even the suburbs of Ft Lauderdale that are included in the Case-Shiller index for Miami. While it is not in the Tampa MSA, places like Ft. Myers and its burbs like Cape Coral saw more ridiculous run-ups than Tampa, but have much less restrictive use measures.

What are the land-use restrictions in Vegas?

I 100% agree that land-use regulations (it’s only restrictions on certain types of activities) might have caused some of the initial run-up (03-04), it cannot explain the behavior of 05-06. This is because of the fact that a massive percentage of purchases nation-wide at that time were not owner-occupied homes – usually ‘investment’ properties. 80% of condos in Miami were going to investors! Land-use has zero impact on how investors view an area. It is these speculators, fueled by terrible financing products and wholly irresponsible actions by investment banks and players like AIG.

Houston, and TX in general, has minimal land-use regulations. However, they used to have terrible fluctuations in housing values. It doesn’t take much to figure out why.

This type of analysis (land-use regs caused the bubble) is especially troubling because it is often pushed by those that are strongest against improving bank regulations. Keeping alternate theories around allow them to say that changing the most dangerous banking practices is unnecessary.

“This type of analysis (land-use regs caused the bubble) is especially troubling because it is often pushed by those that are strongest against improving bank regulations. Keeping alternate theories around allow them to say that changing the most dangerous banking practices is unnecessary.”

I hadn’t thought about that, but you are probably right. I had assumed the agenda of the authors was merely to roll back land use regulation, but their larger purpose may be to serve as a distraction to prevent banking regulations from being passed.

The exception to this is Krugman. He summarized bubble vs. non-bubble as flatland & zoned-zone. “But in the Zoned Zone, which lies along the coasts, a combination of high population density and land-use restrictions – hence “zoned” – makes it hard to build new houses.”

He seems to be sticking by his land-use idea

I’m glancing through the zoning info from his Brookings link. It definitely shows a difference between Dade County and Broward County zoning, but there was little difference in how their prices moved.

It’s also hard to analyze the data presented. But I did a quick comparison of FL vs. NC looking at population gain vs. total housing units change. Looking at census data from 2000 and the 2005-2009 survey, both populations rose by 13%, while number of housing units rose by 18%. Prices have declined all across FL, so they could not fall back on the ‘less homes were built in the bubble areas’, which would probably be false anyway. If there were really more barriers to construction, we should see significant differences between a high-regulation state (FL) and a low-reg state (NC).

I would offer an alternative theory of areas that have the most house-price volatility: the higher the DTI, the more volatility you will see. If an area has lower DTI’s then people are evaluating homes primarily wrt replacement costs-depreciation. If people are maxing out their DTI – well above GSE recommended levels (Miami MSA had an average much higher than the national average at bubble-peak) – any change in financing pushing payments down directly translates to higher prices. Option-ARMs were available everywhere, but only had large impacts in certain areas. The common feature of those areas is high DTIs.

The other problem was that banks viewed the collateral as always increasing in value so that a default is a non-event. Refi or sell, or we foreclose and get the appreciation.

It’s interesting to think, every bank was working on this assumption, and many pension funds or other MBS buyers implicitly also. However banks did not hold a lot of real-estate directly on their books. If their assumption were true, then they were leaving a lot of cash on the table.

DOW down this morning after UE numbers, probably green by close, or down fractionally, with futures up again tomorrow. Main Street twitching to get in the game now and BUY after pressing their noses against the glass watching everybody else get rich. Orderly entrance, orderly exit. Lather rinse repeat.

Hey all you experts, have you seen this:

U.S. Foreclosure Filings May Jump 20% in 2011 as Crisis Peaks

That guy seems pretty confident about a peak in foreclosures. What evidence is there that foreclosures WILL peak?

Foreclosures would have peaked in 2010 if the banks had continued on their course to increase foreclosures in 2010. Since they changed their minds in March of 2010 and decided to focus on short sales, it has taken them nine months to realize that would fail, so now they are back to where they were at the beginning of 2010.

They really don’t have much choice but to increase foreclosures. Their alternative is to allow widespread squatting and give away houses.

Nicely said.

The banks are scared to death … and this is the exact reason why they are not loaning money. Their reserves are growing in anticipation.

“Banks are scared to death”

“Banks are not loaning money”

What planet are you living on, you’re definitely not living in Irvine or Orange County.

Apparently you haven’t talked to anyone at the FDIC, nor anyone in commercial lending, nor anyone trying to get a business loan, etc. etc.

Bank B/Ss are SHRINKING. Huh? Why is that you ask?

C’mon, I know you’re not that stupid.

He didn’t get the memo

Wall $treet Won!

I mean’t Lee not PR

Bank B/S’s are shrinking because they are writing down bad loans. They are originating a huge number of loans for sale to the GSE’s. I do not think the GSE balance sheets are shrinking. The GSEs can then semi-offload their MBSs to the FED (either directly or through buyers who would be buying the treasuries that the fed is buying. The Fed’s balance sheet is definitely not shrinking.

Banks are eager to lend to those that meet reasonable standards. Lending is much looser now than it was a year ago.

Wrong. Bank balance sheets are deflating because commercial underwriting ground to a halt, and Basel III capital requirements require even higher capital requirements to maintain meaning lower leverage ratios. The result is continued pressure to de-lever.

As banks take the hits on bad loans they immediately pressure capital ratios, and must either rase capital or sell assets.

Strong land use regulations reflect the triumph of the haves against the have nots, often using environmental or energy conservation arguments to support their desire to keep out more people. Once you legistlate, say, a large minimum lot size it becomes almost impossible to build new housing that most people can afford. That’s great if you already own a home in that area…not so good if you want to buy!

Land-use regulation is the root of the RE bubble, it helps only rich person, such as Donaldson Bent, as well as politicians get re-elected. But the high flying RE prices only help to increase our national debt ($14 trillion).

My relatives own innumerous land in one of most desired city in Asia, so I have certain knowledge in how this is done in other countries to prevent unfair profits from people invent on the land and sucking our blood and our children’s blood.

In most civilized counties, if a land is approved to be residential zone after the land owner request, the land property tax instance goes up to 10-30%% of the land value, this will force the land own to develop it ASAP. However, if land own does not apply it, then the own may face new regulations and other factors, so the owner need to take risk.

Back to Irvine, after IAC change land zone to residential zone, it stays there for as long as it wishes with super low property tax, this is the problem, the law should enforce the land to be developed ASAP, this will instantly lower the RE prices.

The “Root” of the real estate bubble is the banking system.

The “root” of The Great Housing Bubble really goes back to The Fed’s reckless monetary policies when we had negative (real) interest rates, creating subsidies for credit which WS and housing exploited.

Do we still have negative interest rates? I would think so – this “Charlie Sheen” economy (as ‘Feral’ put it so nicely yesterday) is STILL fueled by cheap credit with no end in sight.

The problem is the solution is the problem.

BTW, I just bought a new car with 100% financing and 0.9% interest!

What were you thinking!!!!

I just bought a car with 100% financing and 0% interest!!

It was a poular Japanese model. When was the last time a Japanese manufacturer offered near-zero interest rates?

Toyota is offering it on their smaller cars. I happened to pick up a large gas-guzzling Honda people hauler.

I’m not worried about fuel prices either. Sure they’re on the way up now, but our economy is too frail to handle that, and the powers that be will make sure they go back down to support growth. This current spike in oil prices is a creatively engineered bubble to scare people and to enable the vultures to suck out another round of profits from amateur investors.

In Lee’s world wall street is about to lose any day now, but in reality the music keeps playing with the fractional reserve money floating off the printing press.

“how this is done in other countries to prevent unfair profits from people invent on the land and sucking our blood and our children’s blood.”

In this country we do not have “unfair profits”. We have private property rights.

In New Mexico, all you have to do is keep a couple cows on your land to qualify it as ‘argicultural’ and then your property taxes go down to zip.

Cows work in Florida too…

http://www2.tbo.com/content/2008/jun/28/280018/me-cattle-call-cuts-johnsons-taxes/

Hey, that’s handy. Fresh milk, fertilizer,lawn maintenance AND lower taxes. I like this idea!

Here we go!

————————————–

The Foreclosure Dump

Published: Thursday, 13 Jan 2011 | 1:24 PM ET

By: Diana Olick

CNBC Real Estate Reporter

It’s coming, no question.

Today’s report from RealtyTrac serves as a warning to big banks, Fannie, Freddie and local communities; The foreclosure glut is coming, and they’d better be ready to get rid of that glut in a big way.

MORE

http://www.cnbc.com/id/41059824

I hope your right, but I’m not so sure. A Fannie Mae duplex a few doors down from a two other duplexes we own came up for sale; we offered 10% below asking, cash. Their response so far…the sound of crickets chirping.

The incentives are wrong as long as we incentivize and allow bankers to lie, cheat, and steal they will.

http://blogs.forbes.com/robertlenzner/2011/01/12/us-banks-reporting-phantom-income-on-1-4-trillion-delinquent-mortgages/?boxes=Homepagechannels

The problem is that banks have been regulated and legislated into perpetual existance by the Federal Reserve Act. Get rid of the Federal Reserve, fractional reserve banking, and fiat currency, and banks will not be able to create money, nor become tbtf, and will be prosecuted when they cheat. Presently cheating and stealing is legislated. More regulation is more of the same problem.

we wont accept anything less then $462,000

Grammar FAIL.

‘wont’?

Apostrophe FAIL.

Regarding the property example, it looks more like the toolbag is just maximizing his cashflow, far beyond anything rent would’ve provided over cost of ownership. I’m not saying it’s right, just highly profitable!