Do you think B of A has given away all the homes they have mortgages on?

Irvine Home Address … 4121 OLD MILL St Irvine, CA 92604

Resale Home Price …… $599,999

I turn on the tube what do i see,

a whole lot a people cryin' "don't blame me"

they point their crooked little fingers at everybody else

spend all their time feelin' sorry for them selves

victim of this, victim of that

your momma's too thin; and your daddy's too fat

get over it,

get over it

all this whinin' and cryin' and pitchin' a fit

get over it, get over it

you say ya haven't been the same since ya had your little crash

but you might feel better if they gave you some cash

The Eagles — Get Over It

As I contemplated the impact of the B of A foreclosure moratorium, the lyrics to the song above kept coming into my mind. Perhaps we should just give these people the houses they are squatting in. That might make them happy.

The squatters and HELOC abusers have already lost their homes, but they are being allowed to squat in the empty shell of their financial lives. They need to move on and get over it.

Shevy got really worked up about it…

Why Would B of A ANNOUNCE that they are halting foreclosures?

"Attention, Attention, everyone considering strategic default, we will not foreclose, you can live in your home for free for the foreseeable future and then rent the same home up the street for 1/2 as much, if and when we get around to foreclosing. By the way, please vote for the politicians that we gave a bunch of money to!" (who cares that your responsible neighbors and grandparents retirements will/are paying for it, the heck with them, our execs need to keep getting bonuses, they are used to it)

They might as well have announced that everyone that is underwater can stop paying their mortgage because they are increasing the time they will allow them to squat and its already pretty long. I understand that B of A is halting foreclosures because of actions of some attorneys, forcing them look at their foreclosure process and make sure they are executing it correctly. However, B of A has a huge staff of lawyers on staff the last I heard, the foreclosure process is not rocket science, and shouldn't they have already been on top of this?

This is highly suspect.?Isn't it likely that by announcing to people that they will not foreclose, at least not in the short term, they will encourage those teetering on the brink of foreclosure to strategically default? Won't many take the leap now that they know that B of A has halted foreclosures? Doesn't it make the most sense for those are underwater, will likely be able to live in the home for free for 6+ months and can likely rent the home up the street for about ½ of the cost of paying for their current home.

Moreover, won't this make title companies apprehensive to give title insurance on foreclosures? How many loans and how many millions if not billions of dollars in losses will this create? Is the system so corrupt that the tax payer will pick up this bill? Can anyone think of any good reason why they would ANNOUNCE this? There is only one reason I can come to.

1) Political- Politicians can jump on board and make out like they are coming down on the banks and forcing them to halt foreclosures.?

I believe that bankers and politicians believe they are smarter than everyone else, I hope they are wrong. Unfortunately, even if they are I don't see any good alternatives to our currently corrupt political parties. From what I can tell, this will only help the banks because supply was going up and demand was going down bringing prices closer to reasonable levels and since B of A is now likely the largest property owner in the country and they no longer are forced to use mark to market accounting their assets were losing value fast.

I do not know the details behind their Countrywide deal but I believe that it's likely that the taxpayers are picking up a huge tab for this debacle. If they do not slow play this inventory, they don't have to show losses, thus bank execs can keep getting their bonuses, and politicians can take credit for halting foreclosures all the while they will continue to trick Americans into believing delaying foreclosures and creating artificial value in housing is a good thing. In reality it's only good for the banks.

My recommendation; let house prices fall back in line with incomes, of course with artificially low rates they are in most of the country, but what if rates were at 8%? By keeping rates artificially low they are basically guaranteeing low to no appreciation for a long time to come in most of the country and delaying the inevitable in others. If underwater loan owners don't listen to the spin and guilt trip that having to move to a rental. And have not been tricked into believing or allowing a foreclosure to ruin their family, cause divorce, or cause their children massive amounts of stress and force them into a life of juvenile delinquency. If underwater home owners have a purchase money loan, they should let it go, rent, let prices come down and buy a new home for much less after this mess is cleared. If it's not a purchase-money loan speak with an attorney but don't be tricked into being an indentured servant for the bank for the next 20+ years. They already tricked you once; it does not have to happen again. Enough with the games, if people have not been paying for the last 3 months and are underwater by 10's of thousands of dollars it does not matter how or when you foreclose.

Housing Bubble News from Patrick.net

Fri Oct 8 2010

Housing faces powerful downside risks (lansner.ocregister.com)

Which cities face biggest housing risks (finance.yahoo.com)

Ex-Ginnie Mae's President on US Housing – Going to get worse (bloomberg.com)

The Freddie and Fannie Scam (greatdepression2006.blogspot.com)

Paradise Valley, AZ targets owners of abandoned luxury houses (azcentral.com)

Foreclosure freeze slows South Florida's residential real estate sales (miamiherald.com)

Foreclosure sales freeze leaves buyers in the cold (poten.com)

In foreclosure controversy, problems run deeper than flawed paperwork (washingtonpost.com)

Robosigned? That'll Be $25,000 – Each (market-ticker.org)

Putting the Foreclosure Paperwork Scandal in Perspective (propublica.org)

IMF and World Bank call for cooler heads on currencies (msnbc.msn.com)

Inflation Expectation Noise (Mish)

Refrigerator Price History at NexTag Seems To Show Deflation (nextag.com)

Obama sends bad forclosure documentation bill back to Congress (news.ino.com)

English Housing market crash feared after average house prices take record plunge (guardian.co.uk)

English Property prices drop 6,000 in a month (telegraph.co.uk)

Tech CEOs tell US gov't how to cut $1 trillion from deficit (networkworld.com)

Our Future In Chains: The For-Profit Debtors' Prison System (activistpost.com)

Suburbs take hit as US poverty climbs (dailybreeze.com)

Equality: Thomas Jefferson to James Madison in 1785 (press-pubs.uchicago.edu)

Compare the returns of renting vs buying

Thu Oct 7 2010

Prediction that California metro area price peaks won't return until 2025 (firsttuesdayjournal.com)

Wisconsin foreclosure filings reach record high (jsonline.com)

Real estate improvement for buyers could last 8 years: IMF (marketwatch.com)

Housing market stumbles again (for sellers) (finance.yahoo.com)

10 reasons renters live mortgage free (finance.yahoo.com)

Housing slump hammers local government tax revenue (finance.yahoo.com)

The Gathering Storm Over Foreclosures (dealbook.blogs.nytimes.com)

JPMorgan, Bank of America Face Hydra of Foreclosure Probes (bloomberg.com)

U.S. bank industry entering new crisis (marketwatch.com)

Foreclosure Furor Rises; Many Call for a Freeze (nytimes.com)

Banking giants suspend thousands of foreclosures (webofdebt.com)

Foreclosure Fraud Reveals Structural & Legal Crisis (ritholtz.com)

Foreclosure Procedures by State (all-foreclosure.com)

Global policymakers clash on currency policies (news.yahoo.com)

Stiglitz: Fed's Flood Of Liquidity Throwing World Into Currency Chaos (dailybail.com)

Insider access to Federal Reserve is goose that lays golden eggs (reuters.com)

McDonald's health insurance plan that caps annual benefits at $2,000 (nytimes.com)

Where is renting cheaper than owning?

Wed Oct 6 2010

Marin, CA house values sink (marinij.com)

Housing Inventory Climbs Again In September (blogs.wsj.com)

Feldstein Warns House Prices May Get More Affordable Without U.S. Aid (businessweek.com)

House Prices Will Drop Another 20% (businessinsider.com)

New-house prices fall to levels of 10 years ago (lvrj.com)

Strategic Defaults Threaten To Make All Major Housing Markets Affordable (realestatechannel.com)

No-interest loans offered to jobless houseowners (boston.com)

Japan's central bank cuts key rate to around zero (washingtonpost.com)

Japanese Politicians fed up with Deflation, Challenge BOJ Independence (Mish)

Economy, jobs expected to remain weak through 2014 (money.cnn.com)

Banks have misled houseowners, lawmakers say (mortgage.ocregister.com)

Banker's Foreclosure Fraud Threatens a New Financial Meltdown (thepennsylvaniaprogressive.com)

Please tell President Obama NOT to sign Interstate Recognition of Notarizations Act (4closurefraud.org)

Buffett Compares Wall Street to Church With Raffle (bloomberg.com)

Goldman Sachs Sued Over German Bank's $37 Million Loss on CDO (bloomberg.com)

Lawyer fees bloom along foreclosure paper trail (contracostatimes.com)

Google's CEO: 'The Laws Are Written by Lobbyists' (theatlantic.com)

Real Democracy (patrick.net from 2006)

What are the rent/buy ratios near you?

Tue Oct 5 2010

A Mammoth One in Five Borrowers Will Default; Jumbo Mortgages Plummet (housingstory.net)

Jersey shore house prices still falling (philly.com)

Sellers pulling houses off O.C. market (lansner.ocregister.com)

Companies Fleeing California For Utah Over Confiscatory Tax Rate (nevadanewsandviews.com)

California Has to Delay Bills to Avert IOUs (bloomberg.com)

Plainfield, IL Real Estate Market is Worse Than You Can Imagine (plainfield.patch.com)

Foreclosure numbers poised to rise again (nctimes.com)

A Way Out For Houseowners In Trouble Hits A Snag (npr.org)

Are The Legal Foreclosure Problems Working In Banks' Interests? (butthenwhat.com)

Banking's New Bailout (newsweek.com)

Why monetary policy can't revive housing (boston.com)

Benefits of houseownership challenged by Fed employees (who will soon be fired) (latimes.com)

Lessons From Ireland's Real Estate Crisis (fool.co.uk)

Bankrupt originators paid in full can't foreclose (4closurefraud.org)

3 Banks Freeze Faulty Foreclosures (video – abcnews.go.com)

Health insurers throw support behind Republican candidates (latimes.com)

S. Carolina Lawmaker Introduces Legislation To Substitute Gold, Silver Coins For Dollar (dailybail.com)

When does it make sense to be your own landlord?

Mon Oct 4 2010

Congress puts rest of America on the hook for overpriced Calif. houses, again (cnbc.com)

Las Vegas faces deepest slide since 1940s (msnbc.msn.com)

Pensacola, FL housing market hits slide (pnj.com)

Sesame Street's Elmo Explains How Mortgage Debt Becomes National Debt (dailybail.com)

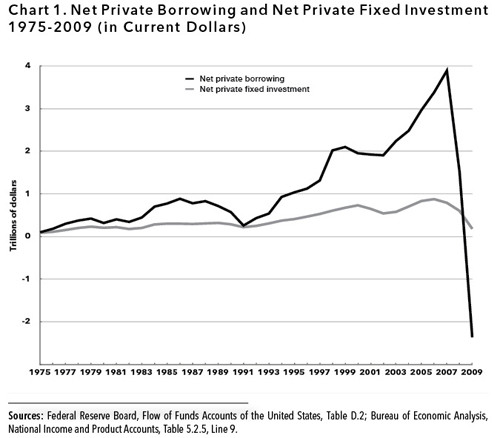

Net Private Borrowing Graph (monthlyreview.org)

{kind=link}

Socialization Of Credit To Prop Up Asset Prices (Mish)

If mortgage rates plunged to 0% (marketwatch.com)

41.7 Million Spend Too Much on Housing (blogs.wsj.com)

The Wisdom of Property and the Politics of the Middle Classes (monthlyreview.org)

Values artificially high because all foreclosures not on market yet (google.com)

Paperwork storm hits nation's biggest bank (washingtonpost.com)

My Turn: Bring the Big Banks to Justice (newsweek.com)

Company Stops Insuring Titles in Chase Foreclosures (nytimes.com)

When real estate riches turn to rags (ocregister.com)

Policeman charged with damaging house after being foreclosed on (pe.com)

In a tough market, house sellers feel discouraged (northjersey.com)

The High-End Real Estate Holdouts (online.wsj.com)

116 Cliff Ave, Capitola, CA 95010 (patrick.net)

Human landscapes in SW Florida (boston.com)

Nothing changes (mattweidnerlaw.com)

{kind=link}

Irvine Home Address … 4121 OLD MILL St Irvine, CA 92604 ![]()

Resale Home Price … $599,999

Home Purchase Price … $460,000

Home Purchase Date …. 12/5/08

Net Gain (Loss) ………. $103,999

Percent Change ………. 22.6%

Annual Appreciation … 13.9%

Cost of Ownership

————————————————-

$599,999 ………. Asking Price

$120,000 ………. 20% Down Conventional

4.52% …………… Mortgage Interest Rate

$479,999 ………. 30-Year Mortgage

$117,536 ………. Income Requirement

$2,438 ………. Monthly Mortgage Payment

$520 ………. Property Tax

$0 ………. Special Taxes and Levies (Mello Roos)

$50 ………. Homeowners Insurance

$65 ………. Homeowners Association Fees

============================================

$3,073 ………. Monthly Cash Outlays

-$407 ………. Tax Savings (% of Interest and Property Tax)

-$630 ………. Equity Hidden in Payment

$201 ………. Lost Income to Down Payment (net of taxes)

$75 ………. Maintenance and Replacement Reserves

============================================

$2,312 ………. Monthly Cost of Ownership

Cash Acquisition Demands

——————————————————————————

$6,000 ………. Furnishing and Move In @1%

$6,000 ………. Closing Costs @1%

$4,800 ………… Interest Points @1% of Loan

$120,000 ………. Down Payment

============================================

$136,800 ………. Total Cash Costs

$35,400 ………… Emergency Cash Reserves

============================================

$172,200 ………. Total Savings Needed

Property Details for 4121 OLD MILL St Irvine, CA 92604

——————————————————————————

Beds: 2

Baths: 2 baths

Home size: 1,192 sq ft

($503 / sq ft)

Lot Size: 5,000 sq ft

Year Built: 1972

Days on Market: 126

Listing Updated: 40447

MLS Number: A10060545

Property Type: Single Family, Residential

Community: El Camino Real

Tract: 0

——————————————————————————

LARGE 2 BEDROOM HOME WITH LIVING ROOM,DINING ROOM KITCHEN FAMJLY ROOM WITH COUNTER,WALKOUT TO SIDE .BEAUTIFUL BACKYARD WITH LOTS OF FRUIT TREES.'TILE FLOOR IN LIVING ROOM,DINING ROOM,KITCHEN, FAMILY ROOM,2 BATHROOM. CARPET IN BEDROOMS. VERY BRIGHT HOME. HOUSE FACES WEST.DOUBLE FRONT ATTACHED GARAGE WITH ENTRANCE INTO THE HOUSE.SHOWS VERY GOOD.READY TO MOVE IN.ON A CUL DE SAC.TWO FULL BATHS . COULD BE ADDED ON UPSTAIRS AND BACK AND FRONT.MUST SEE.IT LOOKS LARGER THAN IT IS .MUST SEE TO BELIEVE.BEAUTIFUL BACK YARD. NOTE: OWNER MAY carry a new first mortgage FOR $460,000 at 6% INTEREST FOR 5 YEARS TERM,INTEREST ONLY.PAYMENT,$140,000 DOWN. NO SECONDS. TO BE $2300 PLUS 1/12 TAXES A MONTH.PURCHASE PRICE MUST BE $600,000.bUYERS TO PAY 1% CLOSING COSTS PLUS TRASFER FEES AND RECORDING FESS AND OTHER FEES NECCESARY TO CLOSE,INCLUDING ALL ESCROW FEES AND TITLE. BUYERS MUST HAVE GOOD CREDIT AND PROOF OF DOWNPAYENT MUST BE SUBMITED WITH THE OFFER.FAMILY ROOM CAN BE CONVERTED TO THIRD BEDROOM.

Financial ripoff

Do you follow the financing terms in the description above? This owner — who is underwater — wants to sell this home by carrying a pass-through note for what he paid for the house and he wants a $140,000 profit as a cash down payment. Please tell me nobody is stupid enough to take this deal.

And he wants to have a carry profit since his note from 2008 is likely less than 6%. And he wants his current taxes refunded to him as part of the transaction. And he wants the buyer to pay nothing toward principal so when the 5 year term is up he can simply take back the property unless the “buyer” can pay $460000 in cash. And he wants 1% to compensate himself for recording the note etc.

All this for a house that “looks larger than it is” I assume the illiterate author of the description is the owner?

Assuming the owner has a mortgage, my guess is he pockets the $140,000, tries to cover HIS mortgage with your payments, then you get evicted in 18 months when the existing 1st lien holder forecloses.

And, $500/sqft for a tiny 1972 home?

Even if my first assumption is wrong, you’re correct that 5 years from now if you can’t finance the $460,000 to pay the balloon, you’re screwed.

And, that description!!! Wow… Unreadable!

This is a perfect house for PR. We’re being priced out…..oh damn, need to get that down payment quickly for this one………..

Of course what Chevy is saying is correct regarding the borrowers, but just as important is only allowing the lender to foreclose. There seems to be concern that some, many, or a heck of a lot of the foreclosures have been filed by entities which do not own the mortgage they are filing on.

Hopefully we will find out if there are one or two circumstances of grievous error and some minor technical flaws, or gross error and large numbers of illegal foreclosures. Neither signifies that the defaulting owners should be allowed to squat, but a mortgage default does not open foreclosure to anybody who claims they own the paper.

We are a nation of law, not convenience.

This is a bogus argument. Read the mortgage. Servicers are authorized to conduct the foreclosure on behalf of the owner of the note. Virtually every mortgage has been securitized and sold off. The only way this system makes any sense is if you have one central point of contact to accept payment and conduct a foreclosure in the event of default.

The argument that only the holder of the note can foreclose flies in the face of the debt obligation that was signed.

Let me be a little more clear.

When these mortgages were securitized they were put into a trust so a large number of mortgages could be pooled and then sold as investment instrumnets to others who own a right to receive payments as they are received. As part of the originall pooling, servicers retain servicing right and are the point of contact for the borrower. As payments are collected by the servicer they are paid into the pool and investors are paid. The trust “holds” the note or is the owner of the note. The servicer acts on behalf of the trust to collect payments or foreclose when necessary.

Mortgages make it clear that an entity other than the original lender or owner (acting on behalf of the owner of the note) is authorized to foreclose if necessary.

There isn’t a question of who owns or holds the note in this. There is a fringe group out there claiming that individual investors are fractionalized owners of the note. Wrong. The investors are merely entitled to payments received and are not owners. If anything, they own a right to receive payments, but are not owners or holders of the indivuals notes.

The slowdown right now is based on a problem with the paperwork that has been filed. It appears as though some lenders/servicers were filing foreclosures without following proper legal procedures regarding the review of loans before filing and recording certain notarized documents. This is where the problem is. It is a paperwork problem, not problem based on the fact that the wrong entity is foreclosing.

You are 100% wrong. The ownership is in question.

http://us1.institutionalriskanalytics.com/pub/IRAMain.asp

the reason banks give to limit foreclosures are all lies. during the last several years i’ve developed the utmost contempt for banks.

they’re just making more excuses to limit housing supply to prevent prices from collapsing further.

the banks can go f themselves.

interesting timing.

the banks start restricting foreclosures during the slow winter months when prices should be crashing. coincidence? let’s see…

1. government mandated foreclosure moratorium (restrict supply).

date: nov 11 2008 – jan 2009

http://www.bizjournals.com/sanfrancisco/stories/2008/11/17/daily83.html

2. government home buyers credit (stimulate buying)

date: jan 1, 2009 to nov 6, 2009

3. extension of the credit (stimulate buying).

date: November 7, 2009 and April 30, 2010.

4. california home buyers tax credit (stimulate buying).

date: may 2010 – august 2010

5. now some sad bullsh*t documentation excuse. another foreclosure moratorium (restrict housing supply)

date: nov 2010 – ?

notice the -consecutive- market props from nov 2008 to today. as soon one ends, another is immediately started. there’s no overlap, there’s no gap. did they coincidentally come up with these dates where as soon as one program ends another is started for the past two years? only a fool would think so.

no doubt, once this latest foreclosure moratorium ends, the banks and government will find some new devious way to keep prices higher. scheme after scheme after scheme, one right after the other, to keep prices higher.

the housing market is so rigged it’s unbelievable, most people don’t even realize it. it’s sad how easy it is to fleece the public.

mike wrote:

> the banks start restricting foreclosures during the slow winter months when prices should be crashing. coincidence? let’s see…

mike, you’re devious. I like that! 🙂

Also, is that timeline construction original work?

If so, you’re devious enough to be a bankster or policy wonk. 🙂

uh wow.

I bet there is some monkey poo that will agree to this. When the poo hits the fan, this monkey poo will sue anybody and everybody claiming he did not know what he was getting into so he should not be fulfill his side of the deal.

No doubt, the American people need someone standing up for them against the banks. Moreover, anyone being unfairly foreclosed upon by the banks needs protection and recourse. In addition, halting foreclosures in areas that this is happening and if it’s that widespread all over the country may have been necessary. But what’s the point of announcing it? What good does that do? Those that are being unfairly foreclosed upon know it. Those that are being fairly foreclosed upon know it. Those that aren’t paying and are squatting know it. They will also figure out pretty quickly when the foreclosure stops or starts again.

I have a client that found a lease on craigslist. The property was being leased by an escrow lady that bought the property at trustee sale when the 2nd lien foreclosed. The property was still subject to a 1.2 million dollar first which she has not paid a penny on. Yet, she collects rent every month from my client. It has now been over 2.5 years that Bank of America has not collected a Penny on the first and the lady that purchased the second made up a bogus law suit to slow down the foreclosure further, which finally got thrown out. They sent a broker out to complete a BPO and he came back with a value of $750,000. The first is now foreclosing and was scheduled for trustee sale a month ago, yet it was postponed and they also refuse to short sell it to my client.

There are 10’s of thousands if not hundreds of thousands of properties out there in similar situations. Landlords collecting rent, not making a payment, and banks not wanting to take the loss letting them do it, this is a bigger travesty than an occasional random paperwork error or even a consistant innocent paperwork error, on a property that has not been paid on for 6 months that is sitting vacant, a landlord that is essentially rent skimming and getting foreclosed on now, or someone that went on a HELOC binge and does not want to pay for it. Bottom line is, right now, Banks don’t have to take losses and are keeping properties off of the market and artificially keeping prices high, making new buyers in many areas the next victims. In many areas the injustice for those have been prudent, save, pay their taxes and just want a home for their family but can’t find one or end up over paying is worse than it is for the HELOC abuser, landlord, or vacant property. This seems to be a convenient excuse to hold thousands of properties off the market, likely at the expense of the responsible American tax payer. I just don’t believe that B of A’s attorney’s can’t figure out the foreclosure process in all 50 states, nor that announcing it serves any good purpose beyond what they think may be a political one.

Ding ding ding! That’s exactly the reason for government regulation of business, a reason that seems to be seldom mentioned these days. Who else will defend a citizen/customer like me against a multi-billion dollar bank let alone a financial industry whose valuation is measured in trillions? It’s why the idea that “Government is the problem, not the solution” is a huge, bald-faced LIE and those screaming it are either bald-faced liars or hopelessly confused. It’s a major reason things are so screwed up today.

Please note, however that I’m speaking in the abstract and not in the concrete as it’s an easily confirmed fact that the regulating bodies in the US government today are controlled and staffed by the industries they are supposed to regulate. For example it’s the financial industry that writes the laws & regulations & it’s the financial industry that decides what laws will be enforced & against whom. And yes, from that viewpoint an industry-controlled government is no solution at all.

One recent article “The Aftermath of the Housing Bubble” (July 2010) at http://housingstory.net/2010/07/28/the-aftermath-of-the-global-housing-bubble-chokes-the-world-banking-system/ published some very interesting charts, that showed that the repo’d properties visible on the market was 5% to 10% of the actual inventory.

In Cook County, IL (Chicago), there are over 28,000 repossessed homes, while only 1,200 repossessed homes are on the market. That is less than 5%.

In Orange County, CA, over 6200 repo’d homes, with only 228 repo’d homes on the market. That’s about 3.5% roughly.

In St. Louis, MO, slightly over 10% of the repo’d inventory is on the market.

Miami-Dade. rather less than 10% of all repos are on the market.

So, for every foreclosed home you see available, about 20 more lurk in the “shadow” inventory. It seems to me that there is quite enough “market overhang” to cause another 50% drop in prices.

How much longer can banks hold on to all this?

You can thank FASB for that one.

For all the bitching about Bernokio, Geithner, Obama and Congress, I’m surprised nobody has been pissed off at the FASB board members for approving new FASB 157 rule governing mark-to-market guidance.

FASB

Frankly, with this change, “pretend and extend” can go on forever.

The FASB link is from April 2, 2009.

Also, not clear if that’s about mortgages or other financial instruments.

Not having to mark to market is ridiculous. I believe that a lot of people feel this way, however, it’s not clear what can be done to change it. When I heard a guy on CNN trying to rationalize not having to mark to market I thought he was joking. No such luck. If banks had to mark to market and a 3rd party company was determining real market value, there would be less incentive for banks to keep shadow inventory. This definately seems to be part of the problem.

I saw the interview this weekend on Bloomberg with Tom Barreck of Colony Capital, and he said the same thing. There is no mark to market with the banks and if they had to they would be insolvent.

At least in the early 1990’s the Resolution Trust Corp. sold off the bad assets of 800 failed S&L institutions and by 1995 most of the problems were cleaned up. This time we have a whole new world of banking.

It is what it is, you can complain about it now or you could have seen it 2 years ago and profited from it.

There is no denying that Irvine price per sq ft was $320 when the world was ending in early 2009. Now it’s trending to $360 per sq ft and those that bought when the world was ending refinanced down over 100 basis points in mortgage rate.

Mark to fantasy will be with us indefinitely. It is our form of socialism to allow people to take on debt of any kind and let 90% of society pay for the defaults. Inflation will eventually take hold further punishing those that don’t join the party.

As usual, I was listening to NPR today. First I heard a bunch of Keynesian rubbish from our nobel laureat economist Mr Paul Krugman going on about the need for a massive goverment stimulus. Then they had a rational sounding economist from Australia say that is the exact wrong thing to do. He went on about how the US now resembles Japan of the 90’s and how US economists are blinded by the “Great Depression”. In Japan, real estate in Tokyo dropped 86% from peak to trough. Other than goverment props which can’t last forever, what’s to really stop that from happening here?

I fear that there might be worse in store for us than a Japan-type economy, which is really probably the BEST outcome we could expect.

I’m afraid we’re on the verge of becoming another Weimar Germany, and I’m sure you’ll agree that we’d be much better off being like Japan of recent years. If our economists and politicians want to recreate the hyperinflation and extreme desperation and misery of the population during the worst years of the Weimar Republic, they’re on the right track by creating ever more government debt and driving the creation of more private debt. We might already have reached the Tipping Point at which we can no longer support existing levels of government debt.

So I doubt we will be so well off as Japan. We will not be so fortunate. We are already in much worse condition than Japan. Japan has a fully functional manufacturing sector, with manufacturing behemoths dedicated to remaining cutting-edge, while we have almost completely dismantled our manufacturing. Most of all, Japan has an extremely resilient population, made so by a high savings rate, while most of us here in the U.S. are literally one paycheck away from living on the streets, and lastly, Japan has a very high degree of social cohesion and cooperation, while we are rather “atomized” and at each other’s throats.

That’s a little extreme, and, I think, wrong. Overall debt levels are gradually declining in the US, as private debt is being reduced, even while government debt is increased, as you note. So the situation isn’t as desperate as all that. The long term issues – entitlements and medicare – are going to be major problems in the future but there is no indication we are headed toward Weimar Germany or even a Japanese outcome. Our demographics are much better, for one thing. Provided we don’t listen to Mr. Krugman and his ilk, things aren’t going to be all that bad, even if we don’t ever recapture the economic euphoria of the ’90s.

“Overall debt levels are gradually declining in the US, as private debt is being reduced,…”

Private debt is being reduced because people are DEFAULTING on the debt, NOT because they’re being paid off.

Yup, defaulting on the debts they have, and unable to get HELOC and small business loans overall.

Sad to watch the USA heading back to a barter economy. Make sure you have a plot of land to farm so you can participate too.

While individuals are defaulting on their debt, I don’t think that is the debt most economists are looking at. Major corporations took on a lot of debt too and now are hording cash to pay down this debt instead of expanding (GM & Chrysler are exceptions… they went thru BK) which is why unemployment is not coming down. That OK when a few of the corps does this but when all the corps pay debt instead of expand at the same time then the economy frezes up.

Alan’s correct, and in any case, while certainly some of the debt reduction is due to defaults – who cares? Also, I didn’t bother to point out two other hopeful factors: #1 an increased household savings rate (up to around 6%) and #2 an increase household net worth (driven by a combination of of debt reduction and increased asset values). Overall these are moderately good signs for the long run (if not necessarily in the short run).

I don’t think I can get over how completely brilliant (if laughable) this ‘owner’s’ idea is. Rather than defaulting on his underwater mortgage, he offers it to someone else – IF they hand him $140,000+ in cash for his trouble. It’s HELOC abuse in reverse! It’s like he built a time machine to 2006.

Truly, a moronically brilliant idea.

It is obvious from the postings on this property that the authors do not know what they are talking about. Based on my understanding, this is an equity sale. A bank does not have a loan on the property. The owner bought the property in 2009 for under 500K and is trying to make a profit. The price is higher than the market but that is normal when the Seller wants to carry financing. I do not understand why the author thinks the Seller is underwater. If I had the option to get a house and pay a little more (if I did not qualify for financing), I would definetly look at seller financing. I know it costs more…plus everything is negotiatable. The listing price is just an ask price. I am constantly looking for Seller financed properties. This property is too small for me…if anybody else out there has a Seller Financed property, please let me know. As long as the property is an equity sale, I might be interested.

Thanks